- South Korea

- /

- Food

- /

- KOSE:A001790

3 Reliable Dividend Stocks Offering Yields Up To 4.3%

Reviewed by Simply Wall St

As global markets continue to navigate through geopolitical tensions and economic uncertainties, major U.S. indexes have shown resilience by approaching record highs, buoyed by strong labor market data and positive sentiment in the housing sector. In this environment of mixed signals and cautious optimism, dividend stocks stand out as a reliable option for investors seeking steady income streams, particularly those offering yields up to 4.3%.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.44% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.51% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.33% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 6.67% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.49% | ★★★★★★ |

| Financial Institutions (NasdaqGS:FISI) | 4.25% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.89% | ★★★★★★ |

| E J Holdings (TSE:2153) | 3.81% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.45% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.35% | ★★★★★★ |

Click here to see the full list of 1954 stocks from our Top Dividend Stocks screener.

Let's review some notable picks from our screened stocks.

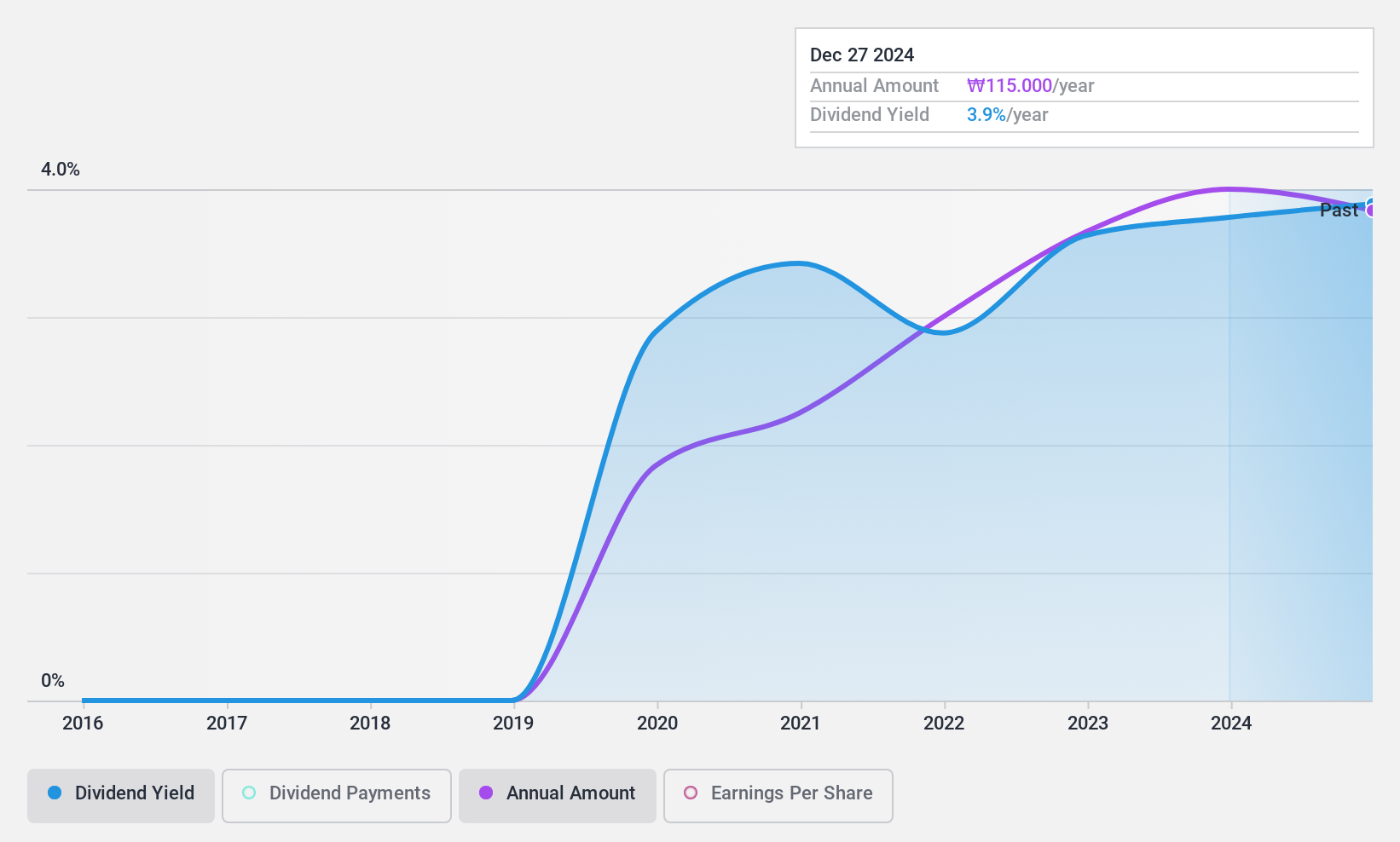

TS (KOSE:A001790)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: TS Corporation operates as a food company in South Korea with a market capitalization of approximately ₩257.43 billion.

Operations: TS Corporation generates revenue through its operations in the food industry in South Korea.

Dividend Yield: 4%

TS Corporation's dividend yield is among the top 25% in the KR market, supported by a stable payout history over six years. Dividends are well-covered by earnings (payout ratio of 44%) and cash flows (cash payout ratio of 50.2%). Despite recent profit margin declines, with net income dropping to KRW 3.27 billion in Q3 from KRW 6.92 billion last year, TS maintains a favorable P/E ratio of 10.9x compared to the market average.

- Unlock comprehensive insights into our analysis of TS stock in this dividend report.

- In light of our recent valuation report, it seems possible that TS is trading beyond its estimated value.

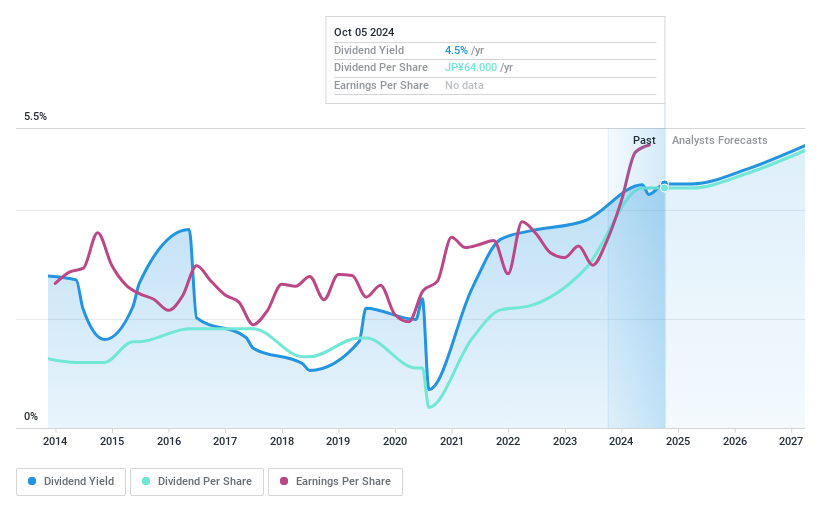

Human Holdings (TSE:2415)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Human Holdings Co., Ltd. operates in human resources, education, and nursing care sectors both in Japan and internationally, with a market cap of ¥15.44 billion.

Operations: Human Holdings Co., Ltd. generates revenue through its diverse operations in human resources, education, and nursing care sectors across Japan and international markets.

Dividend Yield: 4.3%

Human Holdings offers a dividend yield of 4.3%, placing it in the top 25% of Japanese dividend payers, yet its dividends are not supported by free cash flows. Despite a low payout ratio of 30.2%, indicating coverage by earnings, the dividends have been volatile over the past decade. The stock trades at a favorable P/E ratio of 7.2x compared to the market average, but sustainability concerns remain due to unreliable cash flow coverage.

- Navigate through the intricacies of Human Holdings with our comprehensive dividend report here.

- Our valuation report here indicates Human Holdings may be undervalued.

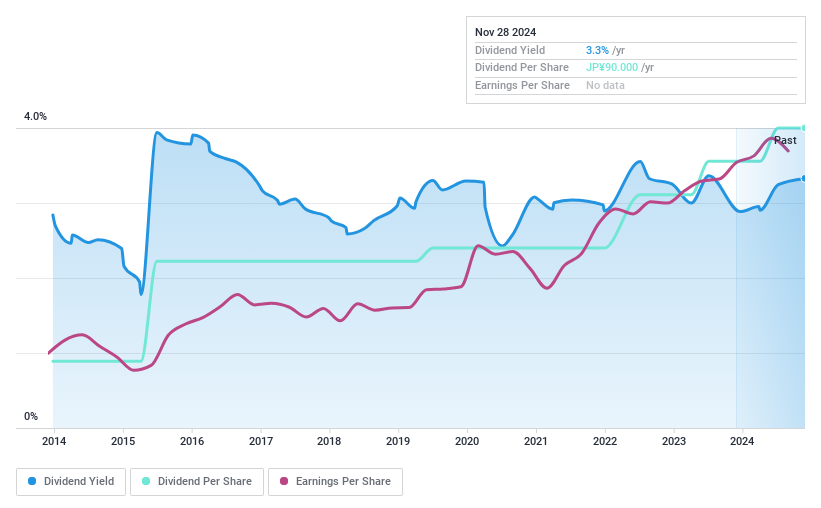

Takara (TSE:7921)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Takara & Company Ltd. operates in the production, consulting, printing, and translation of disclosure and investor relations-related materials both in Japan and internationally, with a market cap of ¥35.32 billion.

Operations: Takara & Company Ltd.'s revenue is primarily derived from its Disclosure Related Business, which generated ¥21.01 billion, and its Interpretation and Translation Business, contributing ¥9.52 billion.

Dividend Yield: 3.3%

Takara's dividends are well-supported by both earnings and cash flows, with a payout ratio of 36.1% and a cash payout ratio of 50.7%. Over the past decade, dividends have been stable and consistently growing. Although its dividend yield of 3.31% is below the top tier in Japan, Takara trades at a significant discount to its estimated fair value, suggesting potential value for investors seeking reliable income amidst steady earnings growth.

- Click here and access our complete dividend analysis report to understand the dynamics of Takara.

- Our comprehensive valuation report raises the possibility that Takara is priced lower than what may be justified by its financials.

Key Takeaways

- Access the full spectrum of 1954 Top Dividend Stocks by clicking on this link.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TS might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A001790

Excellent balance sheet average dividend payer.

Market Insights

Community Narratives