Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, ispace, inc. (TSE:9348) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for ispace

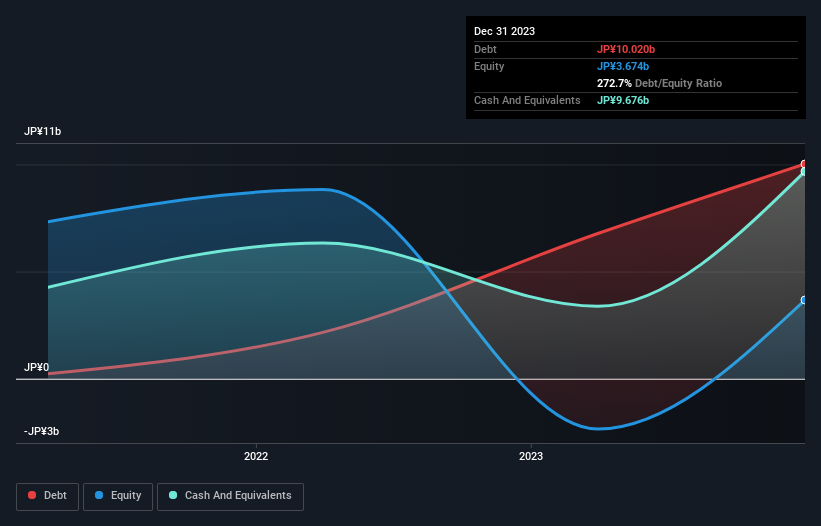

What Is ispace's Net Debt?

As you can see below, at the end of December 2023, ispace had JP¥10.0b of debt, up from JP¥6.78b a year ago. Click the image for more detail. However, it also had JP¥9.68b in cash, and so its net debt is JP¥344.0m.

How Healthy Is ispace's Balance Sheet?

The latest balance sheet data shows that ispace had liabilities of JP¥7.74b due within a year, and liabilities of JP¥6.87b falling due after that. Offsetting these obligations, it had cash of JP¥9.68b as well as receivables valued at JP¥29.0m due within 12 months. So it has liabilities totalling JP¥4.90b more than its cash and near-term receivables, combined.

Of course, ispace has a market capitalization of JP¥91.7b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Carrying virtually no net debt, ispace has a very light debt load indeed. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine ispace's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year ispace wasn't profitable at an EBIT level, but managed to grow its revenue by 119%, to JP¥2.0b. So its pretty obvious shareholders are hoping for more growth!

Caveat Emptor

Despite the top line growth, ispace still had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at JP¥5.4b. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. For example, we would not want to see a repeat of last year's loss of JP¥2.5b. So we do think this stock is quite risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 2 warning signs we've spotted with ispace (including 1 which is a bit unpleasant) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if ispace might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9348

ispace

A lunar resource development company, engages in designing and building lunar landers and rovers to transport customer payloads to the moon.

Adequate balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.2% undervalued

TO

Community Contributor