Advertisement

- Thailand

- /

- Consumer Finance

- /

- SET:THANI

3 Undervalued Stocks Estimated To Trade Up To 46% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

In a week marked by cautious Federal Reserve commentary and political uncertainty, global markets experienced notable declines, with U.S. stocks seeing broad-based losses despite a late-week rally. As investors navigate these turbulent conditions, the search for undervalued stocks becomes increasingly pertinent, offering potential opportunities amidst market volatility. Identifying good stocks often involves assessing those trading below their intrinsic value, especially in times of economic fluctuations and shifting interest rate expectations.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Alltop Technology (TPEX:3526) | NT$265.50 | NT$530.93 | 50% |

| Wasion Holdings (SEHK:3393) | HK$7.03 | HK$14.06 | 50% |

| Kuaishou Technology (SEHK:1024) | HK$42.45 | HK$84.87 | 50% |

| Lindab International (OM:LIAB) | SEK226.40 | SEK451.11 | 49.8% |

| GlobalData (AIM:DATA) | £1.87 | £3.74 | 50% |

| Absolent Air Care Group (OM:ABSO) | SEK255.00 | SEK509.90 | 50% |

| T'Way Air (KOSE:A091810) | ₩2520.00 | ₩5038.37 | 50% |

| Medley (TSE:4480) | ¥3835.00 | ¥7639.79 | 49.8% |

| Surgical Science Sweden (OM:SUS) | SEK159.10 | SEK317.61 | 49.9% |

| GRCS (TSE:9250) | ¥1415.00 | ¥2820.34 | 49.8% |

Let's explore several standout options from the results in the screener.

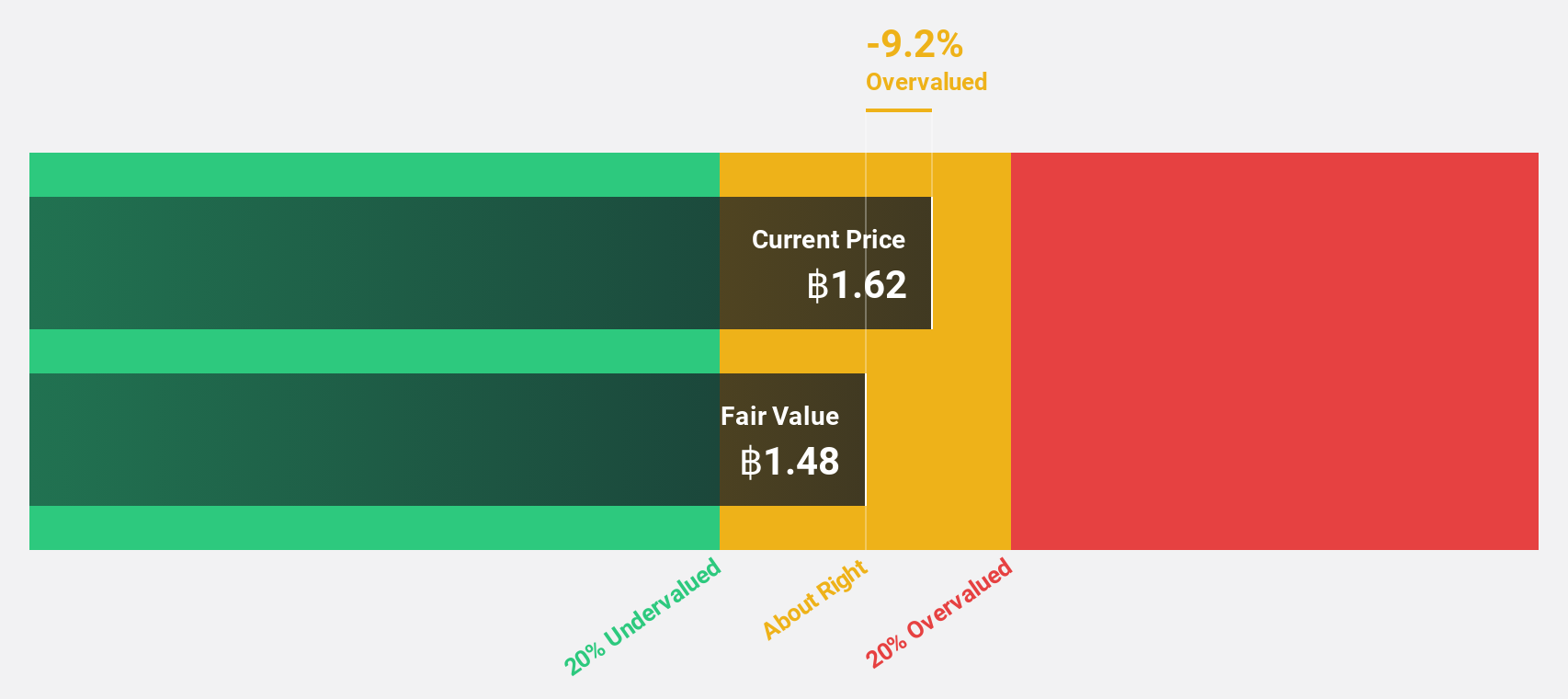

Ratchthani Leasing (SET:THANI)

Overview: Ratchthani Leasing Public Company Limited, along with its subsidiary, offers hire-purchase and leasing services in Thailand and has a market cap of THB9.90 billion.

Operations: The company's revenue segments include THB1.83 billion from its financial service business and THB168.62 million from its insurance brokerage business.

Estimated Discount To Fair Value: 16.2%

Ratchthani Leasing is trading at THB1.59, below the estimated fair value of THB1.9, representing a good relative value compared to peers. Despite high debt levels and recent declines in revenue and net income, earnings are forecast to grow significantly at 20.9% annually over the next three years, outpacing market expectations. Revenue growth is also expected to exceed 20% per year, highlighting potential undervaluation based on cash flows despite current financial challenges.

- Our growth report here indicates Ratchthani Leasing may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of Ratchthani Leasing.

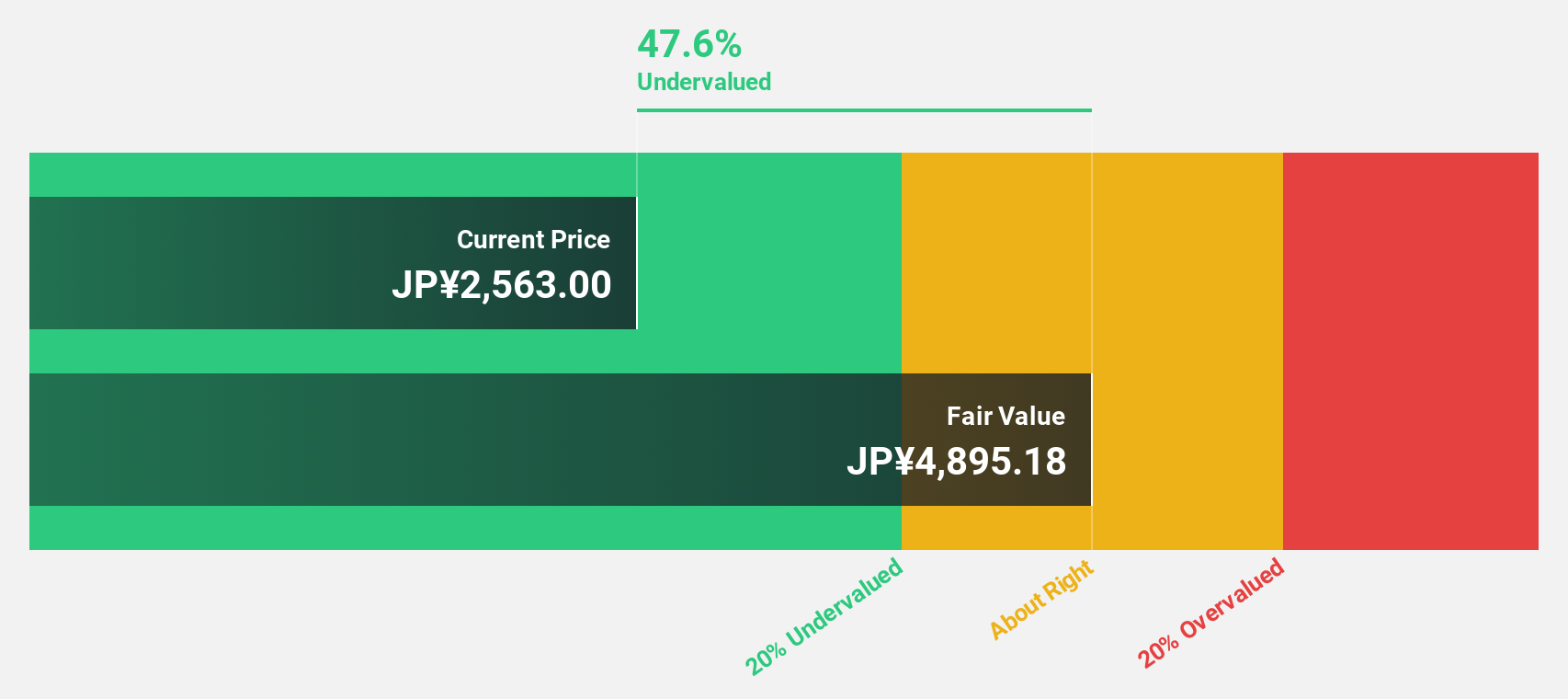

IDEC (TSE:6652)

Overview: IDEC Corporation develops human machine interfaces, industrial switches, control devices, and daily life scenes for markets in Japan and internationally, with a market cap of ¥69.49 billion.

Operations: The company's revenue segments are distributed as follows: ¥34.33 billion from Japan, ¥14.49 billion from the Americas, ¥17.50 billion from Asia-Pacific, and ¥18.77 billion from Europe, Middle East and Africa (EMEA).

Estimated Discount To Fair Value: 46%

IDEC is trading at ¥2357, significantly below its estimated fair value of ¥4362.24, indicating potential undervaluation based on cash flows. Earnings are forecast to grow substantially at 24.9% annually over the next three years, surpassing the JP market's growth rate of 7.9%. However, profit margins have decreased from 9.7% to 3.7%, and the dividend yield of 5.52% is not well covered by earnings, suggesting caution despite growth prospects.

- Our earnings growth report unveils the potential for significant increases in IDEC's future results.

- Dive into the specifics of IDEC here with our thorough financial health report.

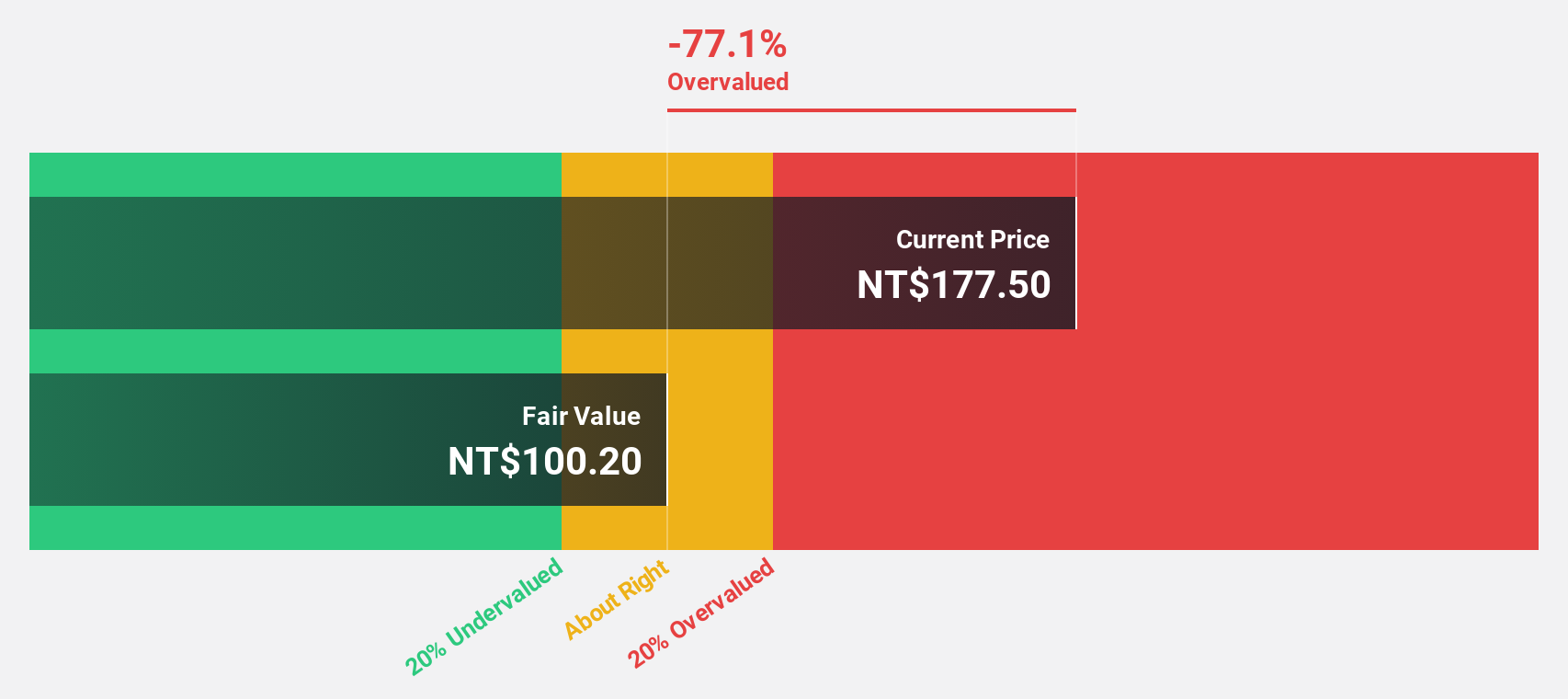

Sunonwealth Electric Machine Industry (TWSE:2421)

Overview: Sunonwealth Electric Machine Industry Co., Ltd. and its subsidiaries manufacture and sell precision motors and thermal solutions globally, with a market cap of NT$26.44 billion.

Operations: The company's revenue segments include NT$22.93 billion from Greater China and NT$790.64 million from Europe and North America.

Estimated Discount To Fair Value: 28.6%

Sunonwealth Electric Machine Industry is trading at NT$96.7, significantly below its fair value estimate of NT$135.34, highlighting potential undervaluation based on cash flows. Earnings are projected to grow substantially at 30.9% annually over the next three years, outpacing the TW market's 19.2% growth rate, despite a volatile share price recently and an unstable dividend track record. Recent earnings showed increased sales but a decline in net income compared to last year.

- Our comprehensive growth report raises the possibility that Sunonwealth Electric Machine Industry is poised for substantial financial growth.

- Get an in-depth perspective on Sunonwealth Electric Machine Industry's balance sheet by reading our health report here.

Taking Advantage

- Get an in-depth perspective on all 872 Undervalued Stocks Based On Cash Flows by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SET:THANI

Ratchthani Leasing

Together with its subsidiary, provides hire-purchase and leasing services in Thailand.

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor