Advertisement

- Japan

- /

- Industrials

- /

- TSE:6501

Hitachi (TSE:6501) Valuation: Is There Still Value After Recent Strong Share Price Gains?

Simply Wall St

Reviewed by Simply Wall St

Hitachi (TSE:6501) shares continue to draw attention from investors, given the company’s diversified business and position in Japan’s technology and infrastructure sectors. Recent price moves highlight ongoing curiosity about future growth and market direction.

See our latest analysis for Hitachi.

Hitachi’s share price has gathered impressive momentum lately, up over 5% in the past week and delivering a strong 22.7% share price return for the last 90 days. That strength caps off an exceptional 34% total shareholder return in the past year, and an eye-catching 262% over three years, which suggests that investor confidence in Hitachi’s growth story is firmly established and still building.

If you’re interested in where technology and innovation are creating new opportunities, now is an ideal moment to discover See the full list for free.

With momentum accelerating and returns outpacing the broader market, the question now is whether Hitachi shares still offer value or if the current price already reflects all future growth prospects. Is there a buying opportunity, or is the market a step ahead?

Most Popular Narrative: 8.3% Undervalued

Hitachi's most widely followed narrative puts fair value at ¥5,415, above the last close of ¥4,968. This perspective argues that market momentum has room to run, but hinges on several aggressive growth drivers and profit margin improvements coming to fruition in the years ahead.

Expansion of the Lumada digital platform and related digital services, including synergies from recent acquisitions like GlobalLogic and the increasing adoption of generative AI solutions, are accelerating high-margin recurring revenues in IT and modernization projects. This is enhancing overall profit margins and long-term earnings growth.

What’s the secret behind this narrative’s bullish fair value? The pricing builds on a future scenario involving sustained profit growth and sector-leading margins. Want the details behind the standout earnings leap, revenue upgrades, and the bold profit projections that fuel this conviction? Discover the numbers and rationale that are driving analyst consensus higher. See the full story now.

Result: Fair Value of ¥5,415 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing global competition and rising project costs could put pressure on Hitachi’s profit margins, which may challenge the optimistic outlook for future returns.

Find out about the key risks to this Hitachi narrative.

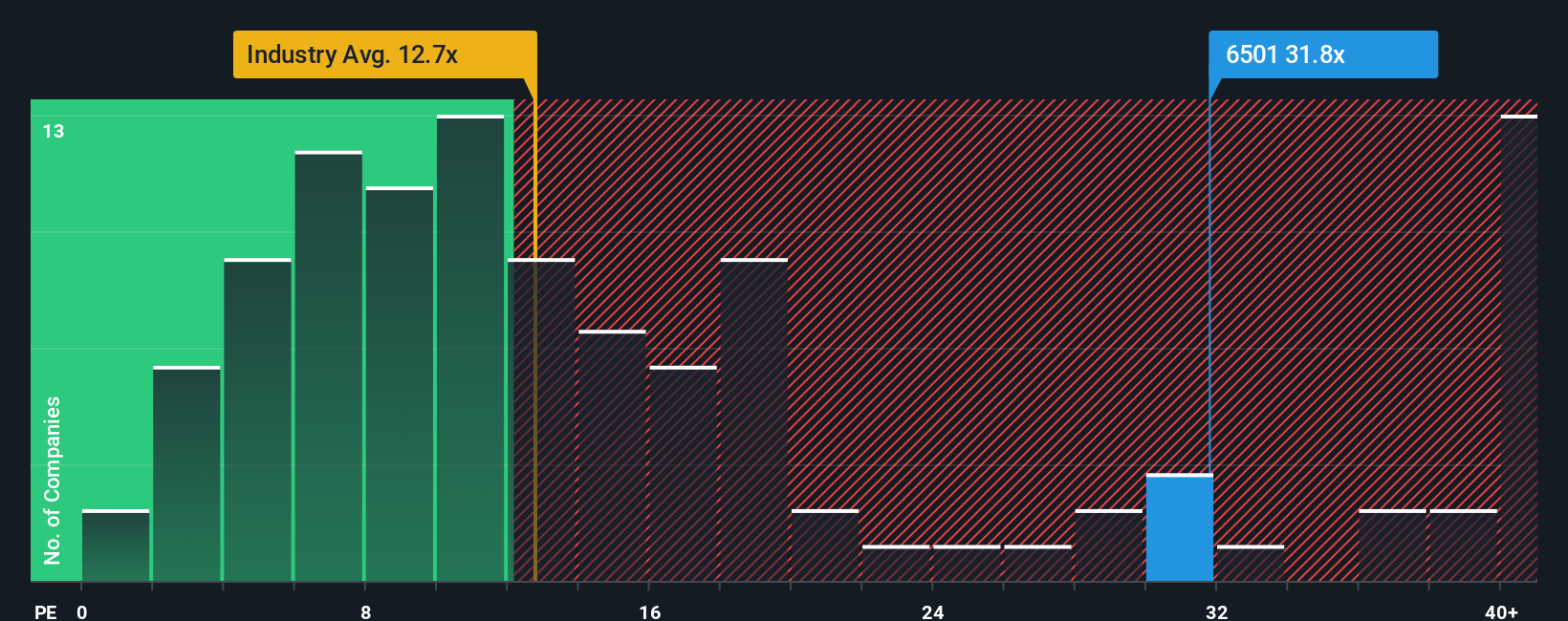

Another View: High Price Compared to Peers

Looking at Hitachi's valuation from a different angle, its current price-to-earnings ratio of 28.3x is well above the industry average of 11.1x and also higher than its peer group average of 12.6x. While this premium suggests confidence in future growth, it also raises the risk that expectations may already be reflected in the price. Can Hitachi deliver enough upside to justify this?

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hitachi for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hitachi Narrative

If you have a different perspective or want to dive into the numbers yourself, shaping your own narrative does not take more than a few minutes. Do it your way.

A great starting point for your Hitachi research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never stop searching for their next great opportunity. Take action now and get ahead of the crowd with unique stocks that match your interests and strategy.

- Tap into tomorrow's leaders in artificial intelligence by checking out these 25 AI penny stocks. These stocks are driving advancements in automation and data innovation.

- Lock in reliable cash flow potential by browsing these 15 dividend stocks with yields > 3%, which consistently offer yields above 3%.

- Position yourself at the frontier of computing with these 28 quantum computing stocks, transforming industries through cutting-edge quantum breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hitachi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6501

Hitachi

Provides digital system and services, green energy and mobility, and connective industry solutions in Japan and internationally.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative