Investors Can Find Comfort In Tsukishima Holdings' (TSE:6332) Earnings Quality

Tsukishima Holdings Co., Ltd.'s (TSE:6332) recent soft profit numbers didn't appear to worry shareholders, as the stock price showed strength. We think that investors might be looking at some positive factors beyond the earnings numbers.

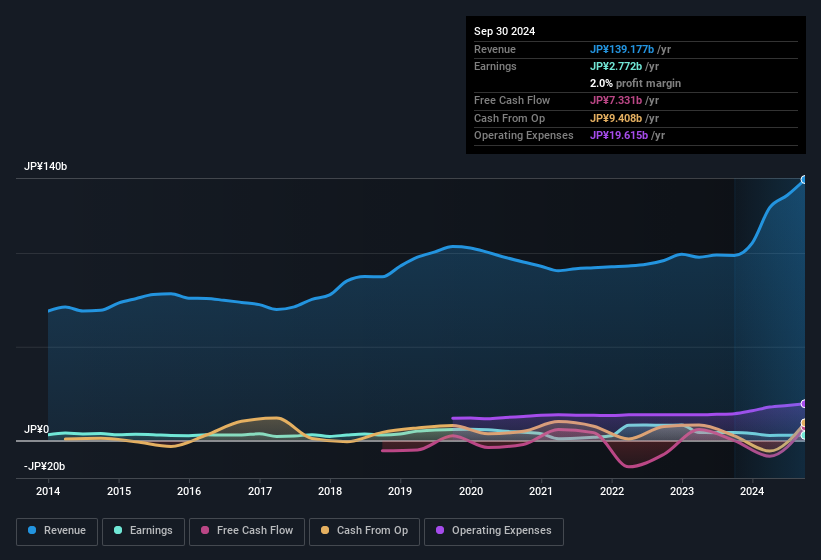

Check out our latest analysis for Tsukishima Holdings

How Do Unusual Items Influence Profit?

Importantly, our data indicates that Tsukishima Holdings' profit was reduced by JP¥915m, due to unusual items, over the last year. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect Tsukishima Holdings to produce a higher profit next year, all else being equal.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Tsukishima Holdings.

Our Take On Tsukishima Holdings' Profit Performance

Unusual items (expenses) detracted from Tsukishima Holdings' earnings over the last year, but we might see an improvement next year. Based on this observation, we consider it likely that Tsukishima Holdings' statutory profit actually understates its earnings potential! And on top of that, its earnings per share have grown at 64% per year over the last three years. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. If you'd like to know more about Tsukishima Holdings as a business, it's important to be aware of any risks it's facing. When we did our research, we found 2 warning signs for Tsukishima Holdings (1 doesn't sit too well with us!) that we believe deserve your full attention.

This note has only looked at a single factor that sheds light on the nature of Tsukishima Holdings' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

Discover if Tsukishima Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6332

Tsukishima Holdings

Provides products and services for water and sewer facilities in Japan and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Community Narratives