Advertisement

How Aggressive Buybacks at Komatsu (TSE:6301) Have Changed Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- Between July and September 2025, Komatsu repurchased 7,968,200 shares for ¥39.76 billion under its ongoing buyback program, completing a total of 14,962,300 shares repurchased since April 2025.

- This substantial buyback activity not only signals the company’s commitment to returning capital to shareholders but also highlights its broader aim to reinforce shareholder value as part of its capital allocation strategy.

- We'll explore how these shareholder-focused buybacks influence Komatsu's investment narrative amid sector innovation and evolving capital priorities.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Komatsu Investment Narrative Recap

For investors considering Komatsu, the core belief centers on the company’s ability to capture long-term growth through infrastructure demand and next-generation mining equipment, while mitigating regional slowdowns and cost headwinds. The recent share buyback update supports Komatsu’s focus on shareholder returns, but does not materially shift the near-term outlook, where the success of mining innovation remains the main catalyst and persistent weakness in Japan and Indonesia remains the chief risk.

Among recent developments, the MoU with Cummins to co-develop hybrid powertrains stands out, directly aligning with regulatory and market trends for cleaner mining equipment. This reinforces Komatsu’s efforts to target new avenues for margin upside and revenue stability as core regions soften.

Yet, it’s also important to remember that, despite strong capital returns, ongoing demand softness in key Asian markets could pressure future earnings if...

Read the full narrative on Komatsu (it's free!)

Komatsu's projections estimate revenues of ¥4,297.5 billion and earnings of ¥444.3 billion by 2028. This outlook is based on a 2.0% annual revenue growth rate and an earnings increase of ¥23.6 billion from current earnings of ¥420.7 billion.

Uncover how Komatsu's forecasts yield a ¥5075 fair value, a 5% downside to its current price.

Exploring Other Perspectives

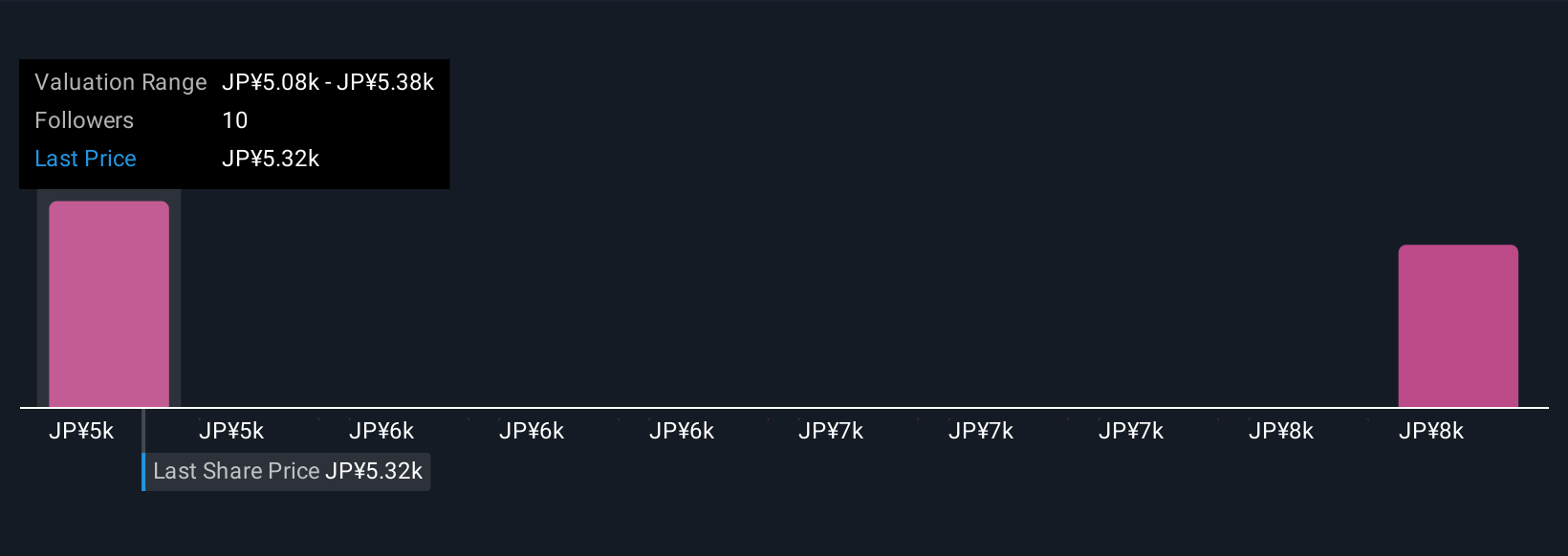

Simply Wall St Community fair value estimates span a wide range from ¥5,075 to ¥8,129, reflecting just 2 different investor perspectives. While buybacks underscore efforts to bolster shareholder value, regional demand weakness remains a pressing concern for Komatsu’s forward momentum.

Explore 2 other fair value estimates on Komatsu - why the stock might be worth as much as 53% more than the current price!

Build Your Own Komatsu Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Komatsu research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Komatsu research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Komatsu's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 34 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Komatsu might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6301

Komatsu

Manufactures and sells construction, mining, and utility equipment in Japan, the Americas, Europe, China, Rest of Asia, Oceania, the Middle East, Africa, and CIS countries.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.5% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor