Advertisement

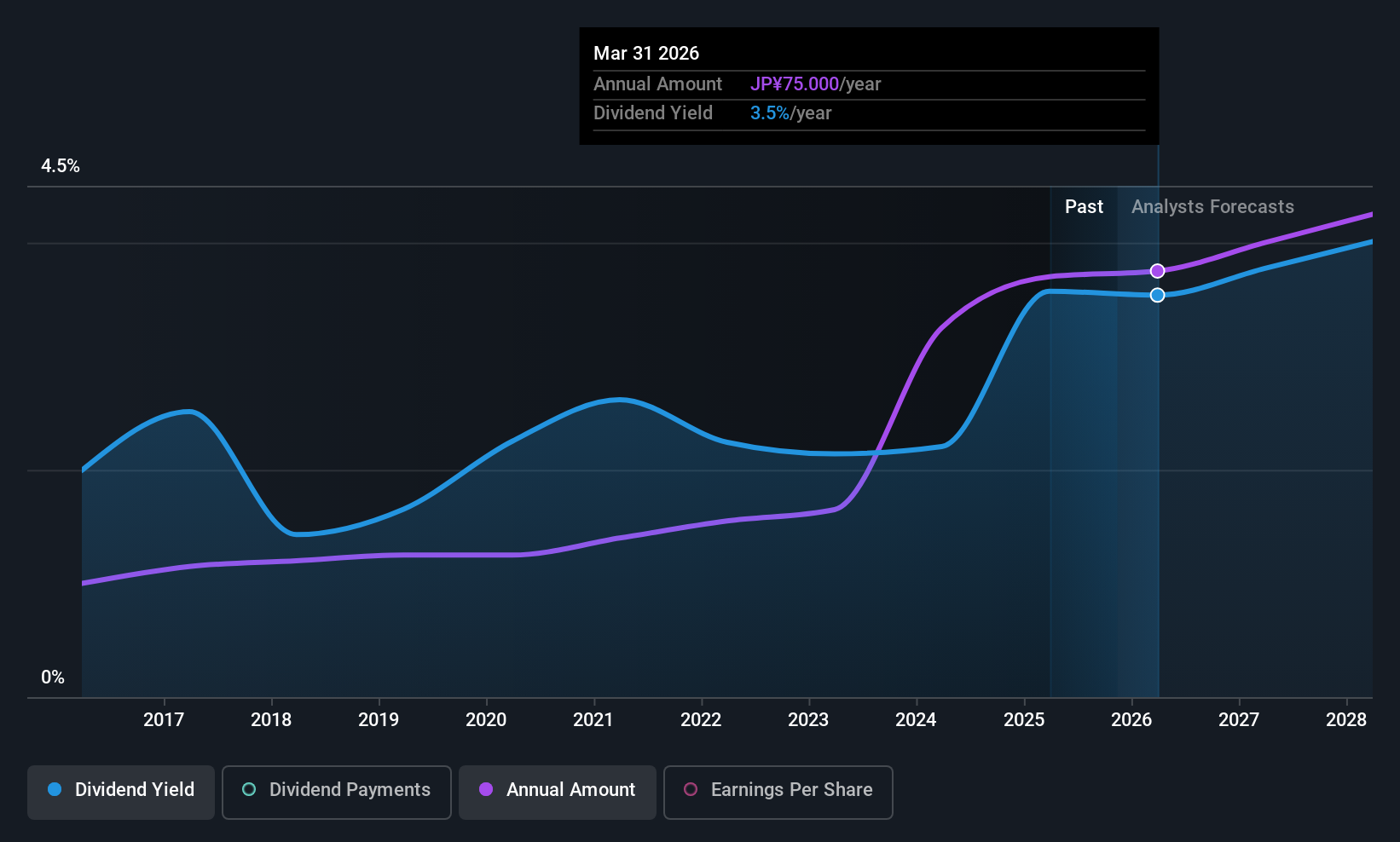

Okada Aiyon Corporation (TSE:6294) will increase its dividend from last year's comparable payment on the 23rd of June to ¥75.00. This will take the dividend yield to an attractive 3.5%, providing a nice boost to shareholder returns.

Okada Aiyon's Future Dividend Projections Appear Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, Okada Aiyon was earning enough to cover the dividend, but it wasn't generating any free cash flows. No cash flows could definitely make returning cash to shareholders difficult, or at least mean the balance sheet will come under pressure.

Over the next year, EPS is forecast to expand by 15.2%. If the dividend continues on this path, the payout ratio could be 43% by next year, which we think can be pretty sustainable going forward.

View our latest analysis for Okada Aiyon

Okada Aiyon Has A Solid Track Record

The company has an extended history of paying stable dividends. The dividend has gone from an annual total of ¥18.00 in 2015 to the most recent total annual payment of ¥75.00. This means that it has been growing its distributions at 15% per annum over that time. It is good to see that there has been strong dividend growth, and that there haven't been any cuts for a long time.

The Dividend Has Growth Potential

The company's investors will be pleased to have been receiving dividend income for some time. It's encouraging to see that Okada Aiyon has been growing its earnings per share at 9.2% a year over the past five years. The company is paying out a lot of its cash as a dividend, but it looks okay based on the payout ratio.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Okada Aiyon will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Just as an example, we've come across 2 warning signs for Okada Aiyon you should be aware of, and 1 of them is potentially serious. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6294

Okada Aiyon

Engages in the manufacture, sale, and repair of construction machines primarily in Japan.

Average dividend payer with moderate growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor