Advertisement

Investors Shouldn't Be Too Comfortable With Hosokawa Micron's (TSE:6277) Earnings

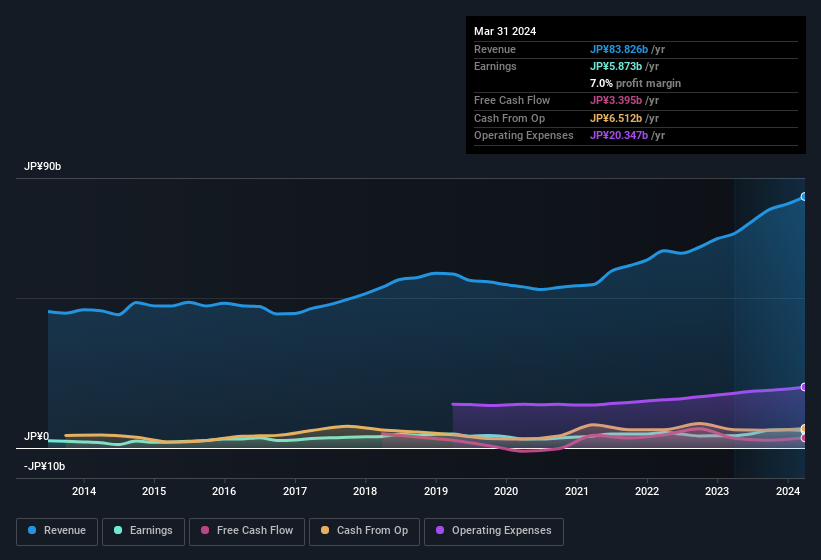

Hosokawa Micron Corporation (TSE:6277) announced strong profits, but the stock was stagnant. Our analysis suggests that shareholders have noticed something concerning in the numbers.

Check out our latest analysis for Hosokawa Micron

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, Hosokawa Micron increased the number of shares on issue by 8.2% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Hosokawa Micron's EPS by clicking here.

A Look At The Impact Of Hosokawa Micron's Dilution On Its Earnings Per Share (EPS)

Hosokawa Micron has improved its profit over the last three years, with an annualized gain of 46% in that time. And the 43% profit boost in the last year certainly seems impressive at first glance. But in comparison, EPS only increased by 54% over the same period. And so, you can see quite clearly that dilution is influencing shareholder earnings.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So it will certainly be a positive for shareholders if Hosokawa Micron can grow EPS persistently. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

The Impact Of Unusual Items On Profit

Alongside that dilution, it's also important to note that Hosokawa Micron's profit suffered from unusual items, which reduced profit by JP¥939m in the last twelve months. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Assuming those unusual expenses don't come up again, we'd therefore expect Hosokawa Micron to produce a higher profit next year, all else being equal.

Our Take On Hosokawa Micron's Profit Performance

To sum it all up, Hosokawa Micron took a hit from unusual items which pushed its profit down; without that, it would have made more money. But on the other hand, the company issued more shares, so without buying more shares each shareholder will end up with a smaller part of the profit. Given the contrasting considerations, we don't have a strong view as to whether Hosokawa Micron's profits are an apt reflection of its underlying potential for profit. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. Case in point: We've spotted 2 warning signs for Hosokawa Micron you should be aware of.

Our examination of Hosokawa Micron has focussed on certain factors that can make its earnings look better than they are. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Hosokawa Micron might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6277

Hosokawa Micron

Provides powder and plastic processing equipment in Japan, the Americas, Europe, Asia, and internationally.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor