Advertisement

Moriya Transportation Engineering and Manufacturing Co.,Ltd.'s (TSE:6226) Shares Leap 29% Yet They're Still Not Telling The Full Story

Moriya Transportation Engineering and Manufacturing Co.,Ltd. (TSE:6226) shareholders have had their patience rewarded with a 29% share price jump in the last month. Taking a wider view, although not as strong as the last month, the full year gain of 18% is also fairly reasonable.

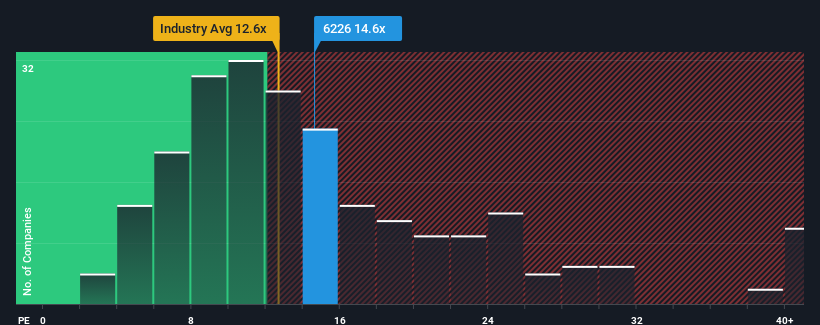

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Moriya Transportation Engineering and ManufacturingLtd's P/E ratio of 14.6x, since the median price-to-earnings (or "P/E") ratio in Japan is also close to 14x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Recent times have been advantageous for Moriya Transportation Engineering and ManufacturingLtd as its earnings have been rising faster than most other companies. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for Moriya Transportation Engineering and ManufacturingLtd

What Are Growth Metrics Telling Us About The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Moriya Transportation Engineering and ManufacturingLtd's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 166% last year. The strong recent performance means it was also able to grow EPS by 31% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 12% during the coming year according to the one analyst following the company. Meanwhile, the rest of the market is forecast to only expand by 9.8%, which is noticeably less attractive.

With this information, we find it interesting that Moriya Transportation Engineering and ManufacturingLtd is trading at a fairly similar P/E to the market. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From Moriya Transportation Engineering and ManufacturingLtd's P/E?

Moriya Transportation Engineering and ManufacturingLtd's stock has a lot of momentum behind it lately, which has brought its P/E level with the market. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Moriya Transportation Engineering and ManufacturingLtd's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

Plus, you should also learn about this 1 warning sign we've spotted with Moriya Transportation Engineering and ManufacturingLtd.

If these risks are making you reconsider your opinion on Moriya Transportation Engineering and ManufacturingLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6226

Moriya Transportation Engineering and ManufacturingLtd

Moriya Transportation Engineering and Manufacturing Co.,Ltd.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.8% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|43.5% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor