Advertisement

Aida Engineering (TSE:6118) Is Due To Pay A Dividend Of ¥30.00

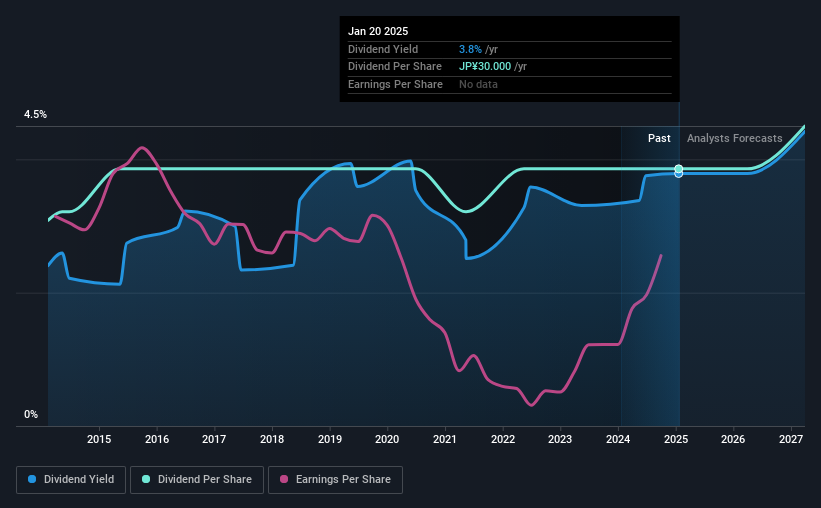

Aida Engineering, Ltd. (TSE:6118) will pay a dividend of ¥30.00 on the 26th of June. Based on this payment, the dividend yield on the company's stock will be 3.8%, which is an attractive boost to shareholder returns.

View our latest analysis for Aida Engineering

Aida Engineering's Payment Could Potentially Have Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, Aida Engineering was quite comfortably covering its dividend with earnings and it was paying more than 75% of its free cash flow to shareholders. The company is clearly earning enough to pay this type of dividend, but it is definitely focused on returning cash to shareholders, rather than growing the business.

Looking forward, earnings per share is forecast to rise by 6.2% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 40%, which is in the range that makes us comfortable with the sustainability of the dividend.

Aida Engineering Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2015, the dividend has gone from ¥24.00 total annually to ¥30.00. This implies that the company grew its distributions at a yearly rate of about 2.3% over that duration. Slow and steady dividend growth might not sound that exciting, but dividends have been stable for ten years, which we think makes this a fairly attractive offer.

Dividend Growth May Be Hard To Achieve

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. However, things aren't all that rosy. Aida Engineering has seen earnings per share falling at 3.7% per year over the last five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

In Summary

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. The low payout ratio is a redeeming feature, but generally we are not too happy with the payments Aida Engineering has been making. This company is not in the top tier of income providing stocks.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 1 warning sign for Aida Engineering that investors should know about before committing capital to this stock. Is Aida Engineering not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6118

Aida Engineering

Manufactures and sells press machines, auto-processing lines, industrial robots, auto-conveyers, and dies in Japan, China, rest of Asia, the Americas, and Europe.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor