KandenkoLtd (TSE:1942) has caught the attention of investors lately, with its recent price movements sparking some interesting questions. While there has not been a single headline-grabbing event, the gradual rise in KandenkoLtd’s share price over the past month is enough to make anyone pause and reconsider if something deeper is at play. For long-term shareholders and curious newcomers alike, shifts like this often raise the all-important question: does this reflect improving fundamentals, market optimism, or something else entirely?

Taking a step back, KandenkoLtd’s stock is up roughly 96% over the past year. The company has nearly quadrupled its value over three years. Momentum has picked up noticeably, with a 3% climb in the past month and an impressive 32% gain over the last three months. This improving performance comes alongside steady annual growth in both revenue and net income, contributing to a sense that investor sentiment may be leaning more bullish as the company delivers.

So is KandenkoLtd overlooked by the market, or is the current price already factoring in every bit of future growth? Let’s dig into what the numbers are telling us.

Advertisement

Price-to-Earnings of 17.5x: Is it justified?

KandenkoLtd is currently trading at a price-to-earnings (P/E) ratio of 17.5x, which makes it more expensive than the Japanese construction industry average of 12.7x and also higher than the fair estimated P/E ratio of 16.3x.

The P/E ratio compares a company's current share price to its per-share earnings. It is commonly used to gauge whether a stock is fairly valued, undervalued, or overvalued compared to peers or the wider industry. For capital goods companies such as KandenkoLtd, this metric offers insight into how the market is pricing in earnings growth and underlying profitability.

Given KandenkoLtd's higher P/E versus industry and fair benchmarks, the market appears to be expecting stronger growth or a higher quality of earnings than most peers. Investors should consider whether such optimism is warranted by the company's forward earnings prospects and recent financial performance, or if expectations have run ahead of fundamentals.

However, potential shortfalls in expected earnings growth or broader market volatility could challenge the optimism reflected in KandenkoLtd’s current valuation.

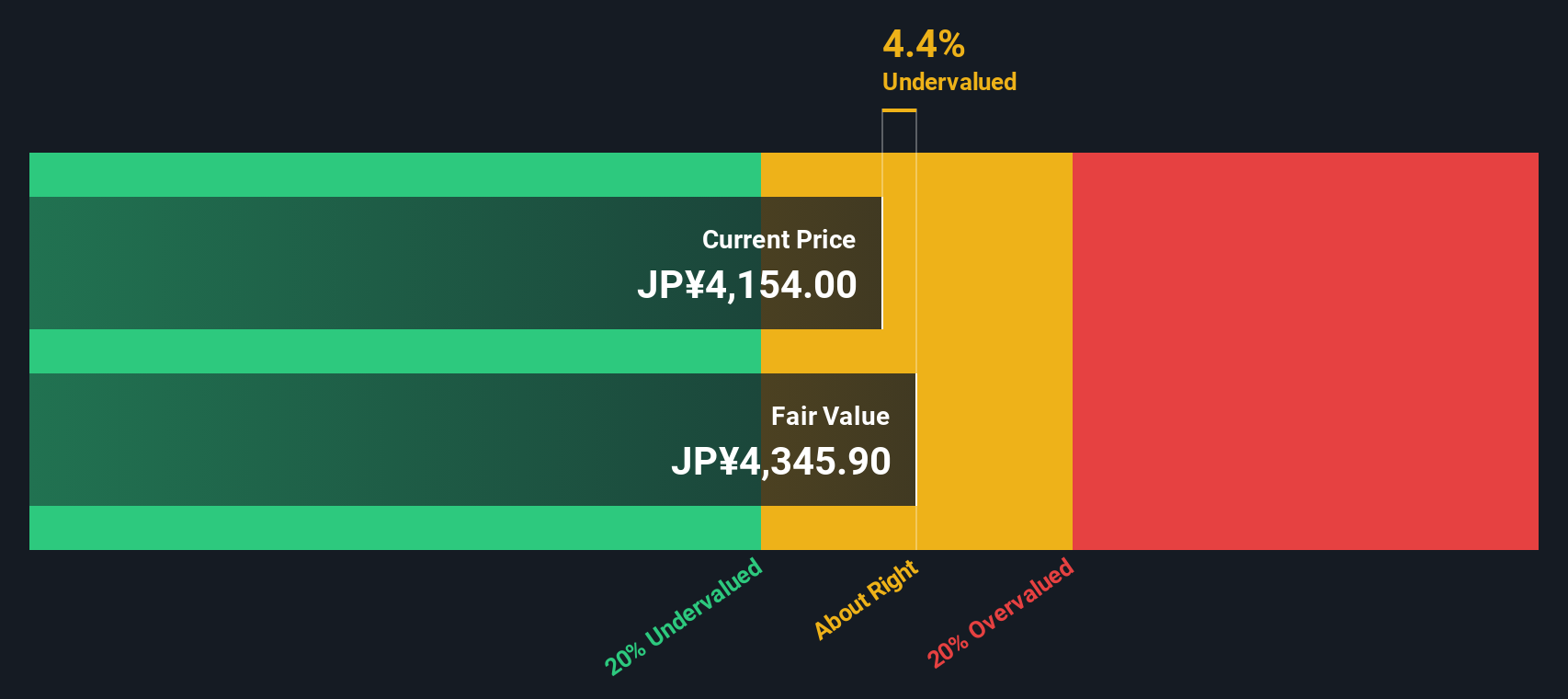

Looking at KandenkoLtd through the lens of our SWS DCF model presents a different perspective. This method currently suggests the shares are undervalued, which challenges the higher valuation implied by earnings multiples. Which approach has it right, and what could shift the balance?

If you see the story differently or prefer to conduct your own research, you can easily form a personal view in just a few minutes, starting today. Do it your way

A great starting point for your KandenkoLtd research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More High-Potential Opportunities?

Don't let your next smart investment slip by. Power up your watchlist with fresh ideas from across the market, handpicked to help you move ahead.

Zero in on under-the-radar opportunities by scanning for penny stocks with strong financials with solid financials and growth potential that many investors overlook.

Tap into the AI revolution by finding AI penny stocks leading innovations in automation, analytics, and intelligent software.

Maximize your returns by focusing on dividend stocks with yields > 3% that offer attractive yields and reliable income for your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KandenkoLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.