Advertisement

- Japan

- /

- Construction

- /

- TSE:1939

Yondenko's (TSE:1939) Shareholders Will Receive A Bigger Dividend Than Last Year

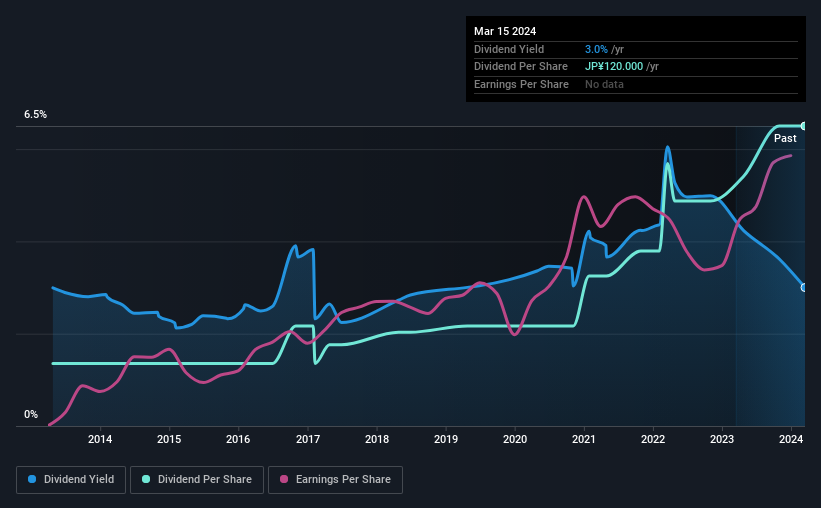

The board of Yondenko Corporation (TSE:1939) has announced that it will be paying its dividend of ¥80.00 on the 1st of July, an increased payment from last year's comparable dividend. This makes the dividend yield about the same as the industry average at 3.0%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Yondenko's stock price has increased by 35% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for Yondenko

Yondenko's Earnings Easily Cover The Distributions

We aren't too impressed by dividend yields unless they can be sustained over time. The last payment was quite easily covered by earnings, but it made up 96% of cash flows. While the company may be more focused on returning cash to shareholders than growing the business at this time, we think that a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

Looking forward, earnings per share could rise by 16.2% over the next year if the trend from the last few years continues. Assuming the dividend continues along recent trends, we think the payout ratio could be 44% by next year, which is in a pretty sustainable range.

Yondenko Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2014, the annual payment back then was ¥25.00, compared to the most recent full-year payment of ¥120.00. This works out to be a compound annual growth rate (CAGR) of approximately 17% a year over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. It's encouraging to see that Yondenko has been growing its earnings per share at 16% a year over the past five years. While on an earnings basis, this company looks appealing as an income stock, the cash payout ratio still makes us cautious.

Our Thoughts On Yondenko's Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For instance, we've picked out 1 warning sign for Yondenko that investors should take into consideration. Is Yondenko not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:1939

Yondenko

Engages in the electrical, and electrical power transmission and distribution facilities construction activities in Japan.

Excellent balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor