Advertisement

Nihon Dengi's (TSE:1723) Upcoming Dividend Will Be Larger Than Last Year's

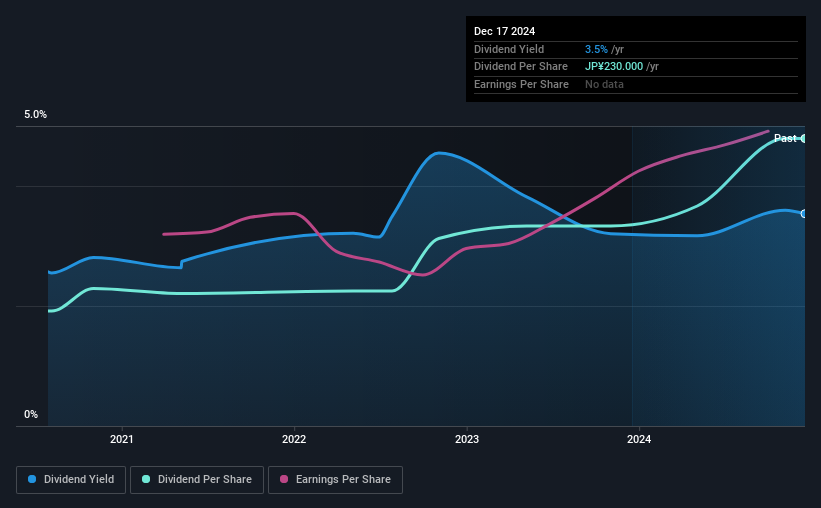

The board of Nihon Dengi Co., Ltd. (TSE:1723) has announced that it will be paying its dividend of ¥148.00 on the 27th of June, an increased payment from last year's comparable dividend. This will take the dividend yield to an attractive 3.5%, providing a nice boost to shareholder returns.

See our latest analysis for Nihon Dengi

Nihon Dengi's Projected Earnings Seem Likely To Cover Future Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. However, prior to this announcement, Nihon Dengi's dividend was comfortably covered by both cash flow and earnings. This means that most of what the business earns is being used to help it grow.

Over the next year, EPS could expand by 9.0% if recent trends continue. If the dividend continues along recent trends, we estimate the payout ratio will be 36%, which is in the range that makes us comfortable with the sustainability of the dividend.

Nihon Dengi Is Still Building Its Track Record

The dividend hasn't seen any major cuts in the past, but the company has only been paying a dividend for 4 years, which isn't that long in the grand scheme of things. Since 2020, the annual payment back then was ¥92.00, compared to the most recent full-year payment of ¥230.00. This works out to be a compound annual growth rate (CAGR) of approximately 26% a year over that time. The dividend has been growing rapidly, however with such a short payment history we can't know for sure if payment can continue to grow over the long term, so caution may be warranted.

We Could See Nihon Dengi's Dividend Growing

Investors could be attracted to the stock based on the quality of its payment history. It's encouraging to see that Nihon Dengi has been growing its earnings per share at 9.0% a year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for Nihon Dengi's prospects of growing its dividend payments in the future.

We Really Like Nihon Dengi's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. See if management have their own wealth at stake, by checking insider shareholdings in Nihon Dengi stock. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Nihon Dengi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:1723

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.9% undervalued

TO

Community Contributor