Advertisement

FIDEA Holdings Co. Ltd. (TSE:8713) will pay a dividend of ¥37.50 on the 4th of December. This makes the dividend yield 4.8%, which will augment investor returns quite nicely.

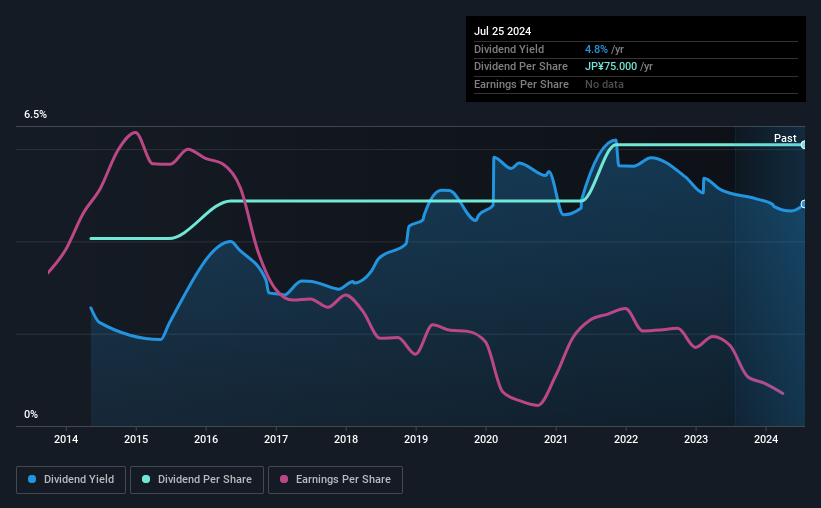

See our latest analysis for FIDEA Holdings

FIDEA Holdings Will Pay Out More Than It Is Earning

If the payments aren't sustainable, a high yield for a few years won't matter that much.

FIDEA Holdings has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Past distributions unfortunately do not guarantee future ones, and FIDEA Holdings' last earnings report actually showed that the company went over its net earnings in its total dividend distribution. This is an alarming sign for the sustainability of its dividends, as it may mean that FIDEA Holdingsis pulling cash from elsewhere to keep its shareholders happy.

Looking forward, EPS could fall by 20.2% if the company can't turn things around from the last few years. Assuming the dividend continues along recent trends, we believe the future payout ratio could reach 149%, which could put the dividend under pressure if earnings don't start to improve.

FIDEA Holdings Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2014, the annual payment back then was ¥50.00, compared to the most recent full-year payment of ¥75.00. This works out to be a compound annual growth rate (CAGR) of approximately 4.1% a year over that time. Although we can't deny that the dividend has been remarkably stable in the past, the growth has been pretty muted.

The Dividend Has Limited Growth Potential

The company's investors will be pleased to have been receiving dividend income for some time. However, things aren't all that rosy. FIDEA Holdings' EPS has fallen by approximately 20% per year during the past five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in.

FIDEA Holdings' Dividend Doesn't Look Sustainable

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. Although they have been consistent in the past, we think the payments are a little high to be sustained. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, FIDEA Holdings has 3 warning signs (and 1 which shouldn't be ignored) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8713

FIDEA Holdings

Through its subsidiaries, provides various banking products and services to corporate and individual customers in Japan.

Established dividend payer and good value.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$268.43|27.9% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|43.8% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|41.0% undervalued

AG

Community Contributor