Kiyo Bank (TSE:8370) might not be the first name on everyone’s watchlist, but its recent performance has started to spark conversations among investors looking for undervalued opportunities in the financial sector. There hasn’t been a headline-grabbing event to trigger this latest move. This makes the stock’s steady gains curious for anyone watching Japanese regional banks. Sometimes, the biggest signals are the quiet ones. Kiyo Bank’s price action is starting to look too significant to ignore.

Over the past year, the stock has delivered a remarkable total return, outpacing the broader market with an 87% gain and showing strong momentum with nearly 21% appreciation in the past 3 months alone. Even as larger players dominate the news cycle, Kiyo Bank’s progress stands out for its consistency. With multi-year returns well into triple digits, the stock’s current trend looks backed by real staying power.

So after this kind of run, are investors looking at a rare buying window, or is the market already factoring in Kiyo Bank’s best days ahead?

Advertisement

Price-to-Earnings of 9.6x: Is it justified?

Kiyo Bank shares are currently trading at a price-to-earnings (P/E) ratio of 9.6, which is lower than both the Japanese banking industry average of 11.2 and the peer group average of 12.1. This suggests the stock could be undervalued by these measures.

The price-to-earnings ratio helps investors compare how much they are paying for each unit of earnings, making it a widely used tool for valuation in the banking sector. A lower P/E can indicate that a stock is priced conservatively relative to its peers and may signal opportunity if earnings quality is high.

For Kiyo Bank, this valuation appears supported by strong recent profit growth, higher-than-peer returns over the last year, and above-industry momentum. This suggests the market may not have fully priced in the bank’s recent operational improvements and earnings strength, which could allow for potential catch-up if positive trends continue.

However, limited visibility into future profit growth and the lack of clear analyst targets could leave investors exposed if market sentiment shifts unexpectedly.

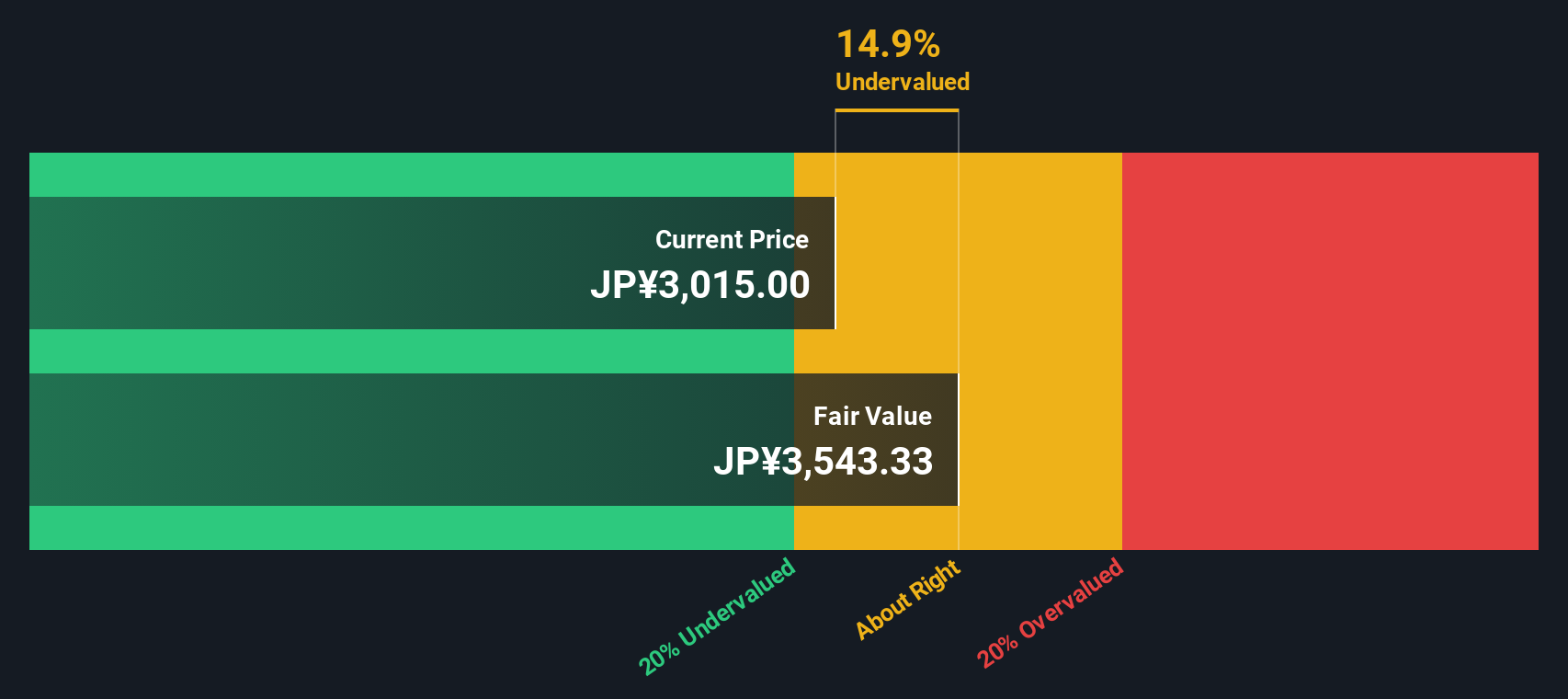

Switching gears from earnings multiples, the SWS DCF model also weighs in on Kiyo Bank’s value and finds the shares undervalued compared to the current market price. But can two valuation methods both be right, or is something being overlooked?

Smart investors always keep fresh opportunities within reach. If you want to broaden your watchlist, these unique market themes deserve your immediate attention. Don’t let opportunity pass you by:

Spot companies harnessing artificial intelligence to transform industries, tapping into the next big wave with AI penny stocks.

Capture growth by targeting fast movers in the penny stock universe with robust financials. Start your search with penny stocks with strong financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kiyo Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.