Advertisement

Hachijuni Bank (TSE:8359) Is Paying Out A Larger Dividend Than Last Year

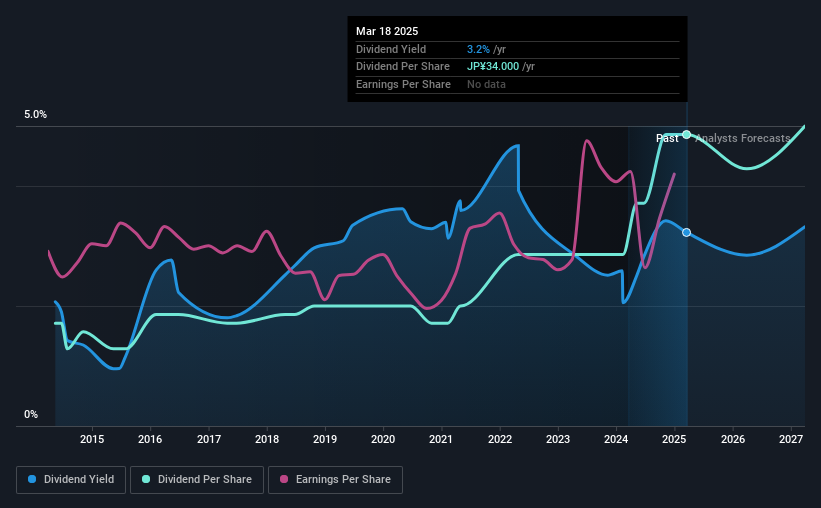

The board of The Hachijuni Bank, Ltd. (TSE:8359) has announced that it will be paying its dividend of ¥21.00 on the 24th of June, an increased payment from last year's comparable dividend. Based on this payment, the dividend yield for the company will be 3.2%, which is fairly typical for the industry.

Check out our latest analysis for Hachijuni Bank

Hachijuni Bank's Earnings Will Easily Cover The Distributions

Unless the payments are sustainable, the dividend yield doesn't mean too much.

Hachijuni Bank has established itself as a dividend paying company with over 10 years history of distributing earnings to shareholders. Past distributions do not necessarily guarantee future ones, but Hachijuni Bank's payout ratio of 36% is a good sign as this means that earnings decently cover dividends.

Over the next year, EPS is forecast to expand by 12.5%. If the dividend continues on this path, the future payout ratio could be 41% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2015, the dividend has gone from ¥12.00 total annually to ¥34.00. This implies that the company grew its distributions at a yearly rate of about 11% over that duration. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Has Growth Potential

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Hachijuni Bank has seen EPS rising for the last five years, at 8.7% per annum. Hachijuni Bank definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

Hachijuni Bank Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Earnings are easily covering distributions, and the company is generating plenty of cash. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 1 warning sign for Hachijuni Bank that investors should know about before committing capital to this stock. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Hachijuni Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8359

Hachijuni Bank

Provides various banking products and services to individuals, corporations, and sole proprietors.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$268.43|26.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.3% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.3% undervalued

AG

Community Contributor