- Thailand

- /

- Specialty Stores

- /

- SET:HMPRO

Home Product Center And 2 Other Top Dividend Stocks For Your Portfolio

Reviewed by Simply Wall St

In a week marked by fluctuating indices and mixed economic signals, global markets have shown resilience despite challenges such as subdued manufacturing activity and divergent labor market data. As investors navigate this complex landscape, dividend stocks like Home Product Center offer a compelling opportunity for those seeking steady income streams amidst market volatility. Understanding what makes a good dividend stock involves evaluating factors such as consistent earnings growth, strong cash flow, and a commitment to returning value to shareholders—qualities that become particularly attractive in uncertain economic environments.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 6.85% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 5.16% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.23% | ★★★★★★ |

| Financial Institutions (NasdaqGS:FISI) | 4.87% | ★★★★★★ |

| Innotech (TSE:9880) | 4.76% | ★★★★★★ |

| Business Brain Showa-Ota (TSE:9658) | 4.22% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.97% | ★★★★★★ |

| James Latham (AIM:LTHM) | 5.94% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.87% | ★★★★★★ |

| Banque Cantonale Vaudoise (SWX:BCVN) | 5.00% | ★★★★★★ |

Click here to see the full list of 2002 stocks from our Top Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

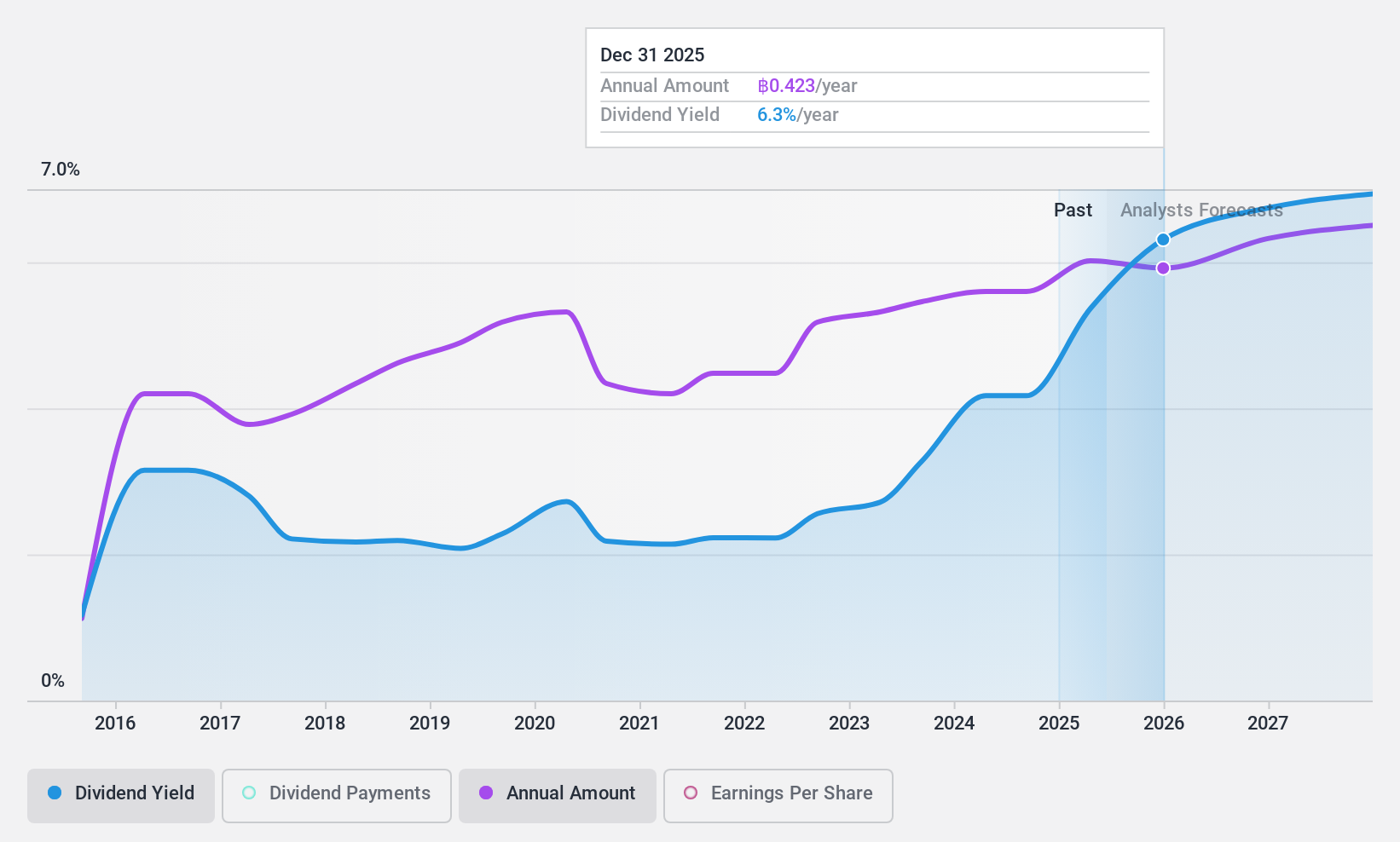

Home Product Center (SET:HMPRO)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Home Product Center Public Company Limited is a home improvement retailer operating in Thailand, Malaysia, and Vietnam with a market cap of THB128.88 billion.

Operations: Home Product Center's revenue from retail building products amounts to THB72.47 billion.

Dividend Yield: 4.1%

Home Product Center's dividend payments have been volatile over the past decade, though they have shown growth in that period. The current payout ratio of 81.7% suggests dividends are covered by earnings, and with a cash payout ratio of 85.9%, they are also supported by free cash flow. Despite a lower yield compared to top market payers, the stock trades at good value relative to peers with a price-to-earnings ratio below industry average.

- Click to explore a detailed breakdown of our findings in Home Product Center's dividend report.

- In light of our recent valuation report, it seems possible that Home Product Center is trading behind its estimated value.

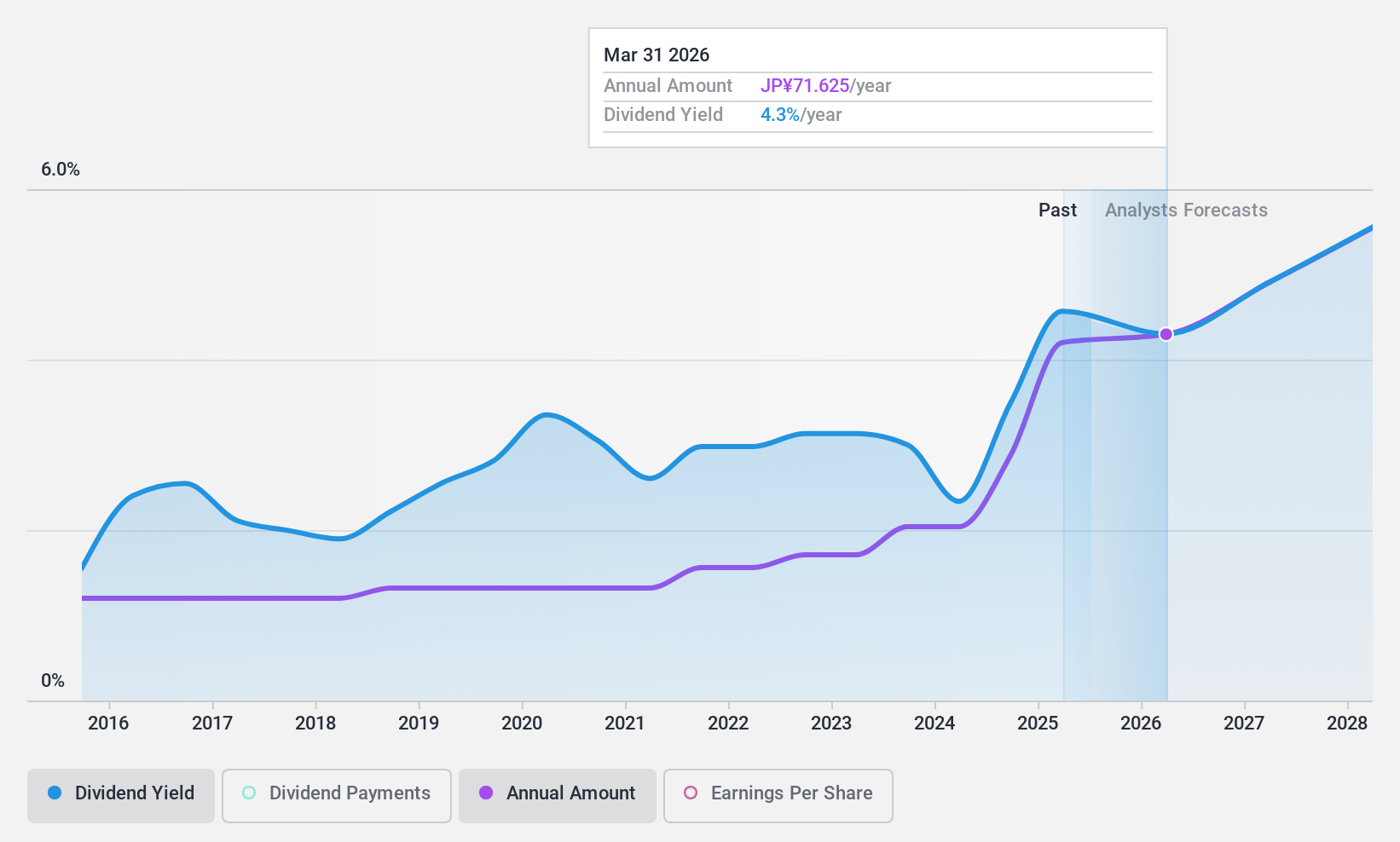

Shizuoka Financial GroupInc (TSE:5831)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Shizuoka Financial Group, Inc., along with its subsidiaries, offers a range of banking products and services and has a market capitalization of approximately ¥680.85 billion.

Operations: Shizuoka Financial Group, Inc. generates its revenue through diverse banking products and services offered by its subsidiaries.

Dividend Yield: 3.7%

Shizuoka Financial Group Inc. offers a reliable dividend yield of 3.69%, slightly below the top quartile in Japan, yet its dividends have been stable and growing over the past decade. The company's payout ratio of 34.6% indicates dividends are well covered by earnings, although there's insufficient data to predict future coverage. Despite large one-off items affecting results, it trades at a discount to its estimated fair value, enhancing its attractiveness for dividend investors.

- Take a closer look at Shizuoka Financial GroupInc's potential here in our dividend report.

- Our valuation report unveils the possibility Shizuoka Financial GroupInc's shares may be trading at a discount.

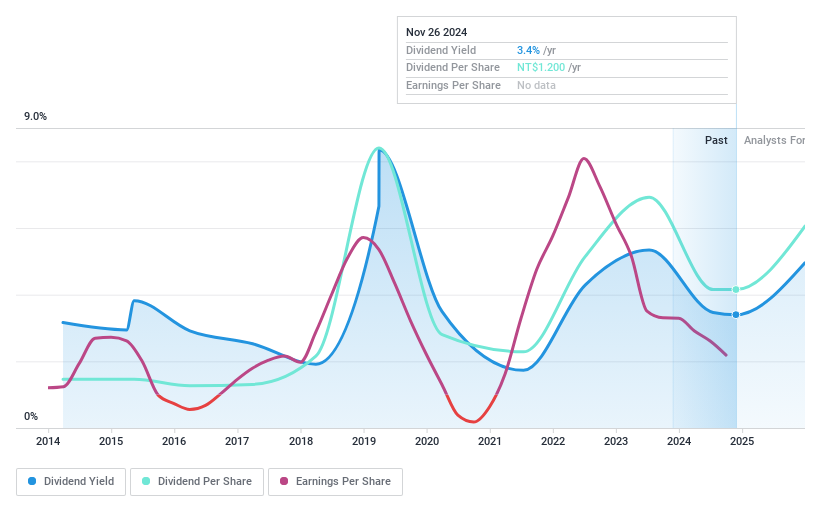

Ta Chen Stainless Pipe (TWSE:2027)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Ta Chen Stainless Pipe Co., Ltd. is engaged in the manufacturing, processing, and sale of stainless steel pipes, plates, fittings, and venetian blinds across Taiwan, the United States, China, and other international markets with a market cap of approximately NT$69.99 billion.

Operations: Ta Chen Stainless Pipe Co., Ltd.'s revenue is primarily derived from its Stainless Steel and Aluminum Products Department, which generated NT$77.70 billion, followed by the Screws and Nuts Segment at NT$22.04 billion, and Aluminum Products Manufacturing contributing NT$21.79 billion.

Dividend Yield: 3.5%

Ta Chen Stainless Pipe's recent earnings report shows a decline in sales and net income, raising concerns about its financial performance. Despite this, the company's dividends are well-covered by both earnings and cash flows with payout ratios of 74.6% and 11.1%, respectively. However, its dividend history is marked by volatility and unreliability over the past decade. While offering a lower yield of 3.49% compared to top-tier payers in Taiwan, it trades at an attractive P/E ratio below the market average.

- Click here and access our complete dividend analysis report to understand the dynamics of Ta Chen Stainless Pipe.

- According our valuation report, there's an indication that Ta Chen Stainless Pipe's share price might be on the expensive side.

Taking Advantage

- Get an in-depth perspective on all 2002 Top Dividend Stocks by using our screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Home Product Center might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SET:HMPRO

Home Product Center

Operates as a home improvement retailer in Thailand, Malaysia, and Vietnam.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives