- Japan

- /

- Auto Components

- /

- TSE:7276

Koito Manufacturing Co., Ltd.'s (TSE:7276) Share Price Matching Investor Opinion

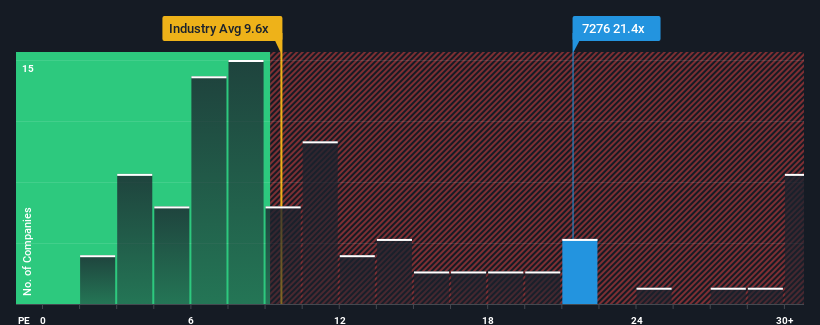

When close to half the companies in Japan have price-to-earnings ratios (or "P/E's") below 13x, you may consider Koito Manufacturing Co., Ltd. (TSE:7276) as a stock to avoid entirely with its 21.4x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

While the market has experienced earnings growth lately, Koito Manufacturing's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Koito Manufacturing

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Koito Manufacturing's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 42%. This means it has also seen a slide in earnings over the longer-term as EPS is down 38% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 32% per annum during the coming three years according to the twelve analysts following the company. That's shaping up to be materially higher than the 10% per annum growth forecast for the broader market.

With this information, we can see why Koito Manufacturing is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Koito Manufacturing maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware Koito Manufacturing is showing 2 warning signs in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Koito Manufacturing, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Koito Manufacturing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7276

Koito Manufacturing

Manufactures and markets automotive lighting equipment, aircraft parts, electrical equipment, and other products in Japan.

Flawless balance sheet average dividend payer.