Advertisement

- Japan

- /

- Construction

- /

- TSE:1882

Top Dividend Stocks To Consider In February 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by fluctuating corporate earnings, AI competition fears, and geopolitical tensions over tariffs, investors are keenly observing the Federal Reserve's steady interest rate policy and the European Central Bank's recent rate cut. Amid this backdrop of economic adjustments and market volatility, dividend stocks offer a potential avenue for stability and income generation. In this environment, selecting dividend stocks with strong fundamentals and consistent payout histories can be an attractive strategy for those looking to mitigate risk while seeking reliable returns.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Peoples Bancorp (NasdaqGS:PEBO) | 4.81% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 3.99% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 5.28% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.48% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.42% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.08% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.45% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.96% | ★★★★★★ |

| FALCO HOLDINGS (TSE:4671) | 6.66% | ★★★★★★ |

| Yamato Kogyo (TSE:5444) | 3.88% | ★★★★★★ |

Click here to see the full list of 1959 stocks from our Top Dividend Stocks screener.

We'll examine a selection from our screener results.

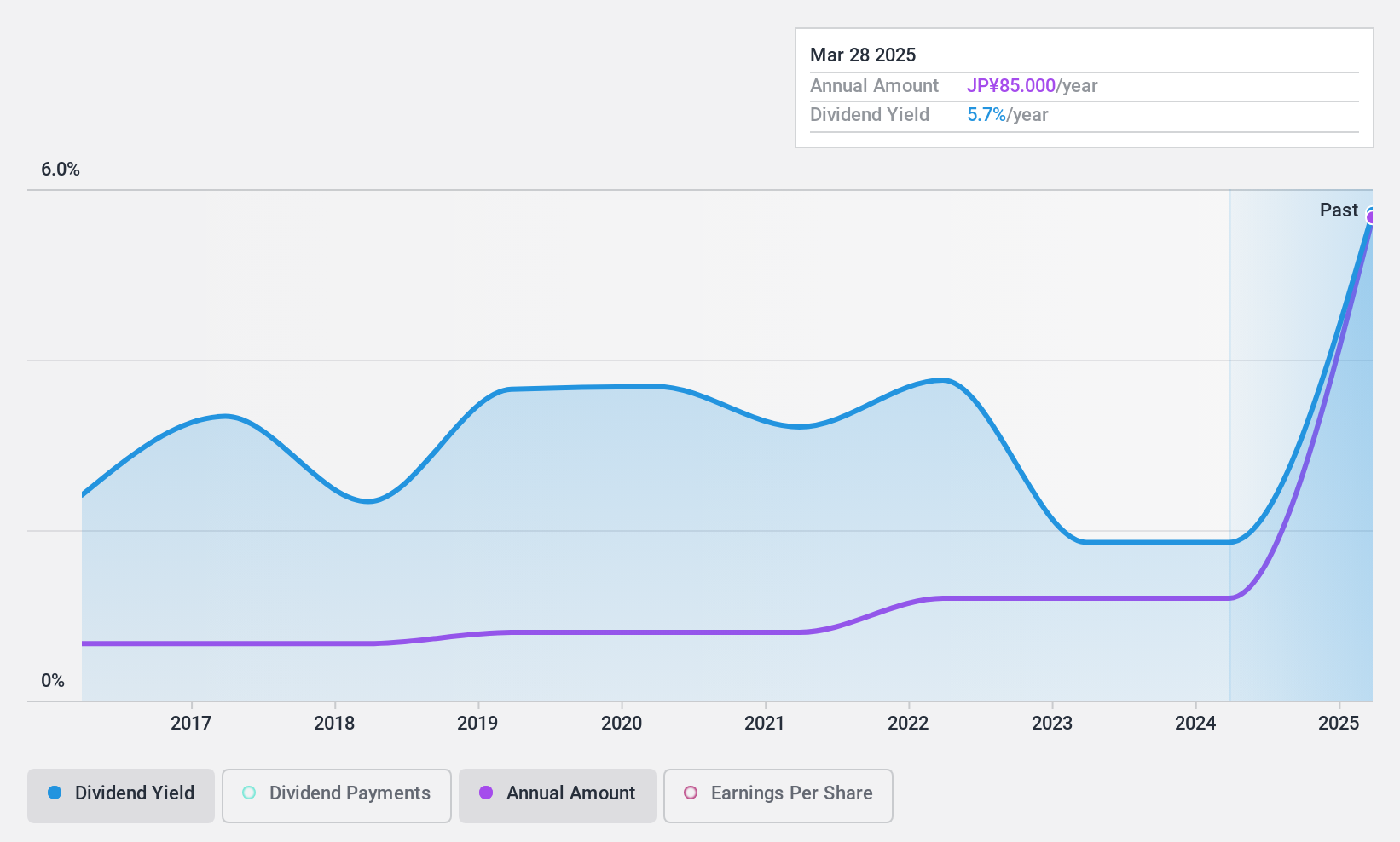

Toa Road (TSE:1882)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Toa Road Corporation operates in the civil engineering sector in Japan and has a market capitalization of ¥70.07 billion.

Operations: Toa Road Corporation's revenue is primarily derived from its Construction Business, generating ¥72.66 billion, and its Manufacturing and Sales, Environmental Business, Etc., contributing ¥49.52 billion.

Dividend Yield: 3.4%

Toa Road has maintained reliable and growing dividend payments over the past decade, with dividends increasing steadily. Although its payout ratio of 50.3% suggests dividends are covered by earnings, the lack of free cash flow raises concerns about sustainability. The company's dividend yield is competitive within Japan's top quartile at 4.01%. However, reliance on non-cash earnings could affect future payouts' stability despite consistent historical performance.

- Get an in-depth perspective on Toa Road's performance by reading our dividend report here.

- Our valuation report here indicates Toa Road may be overvalued.

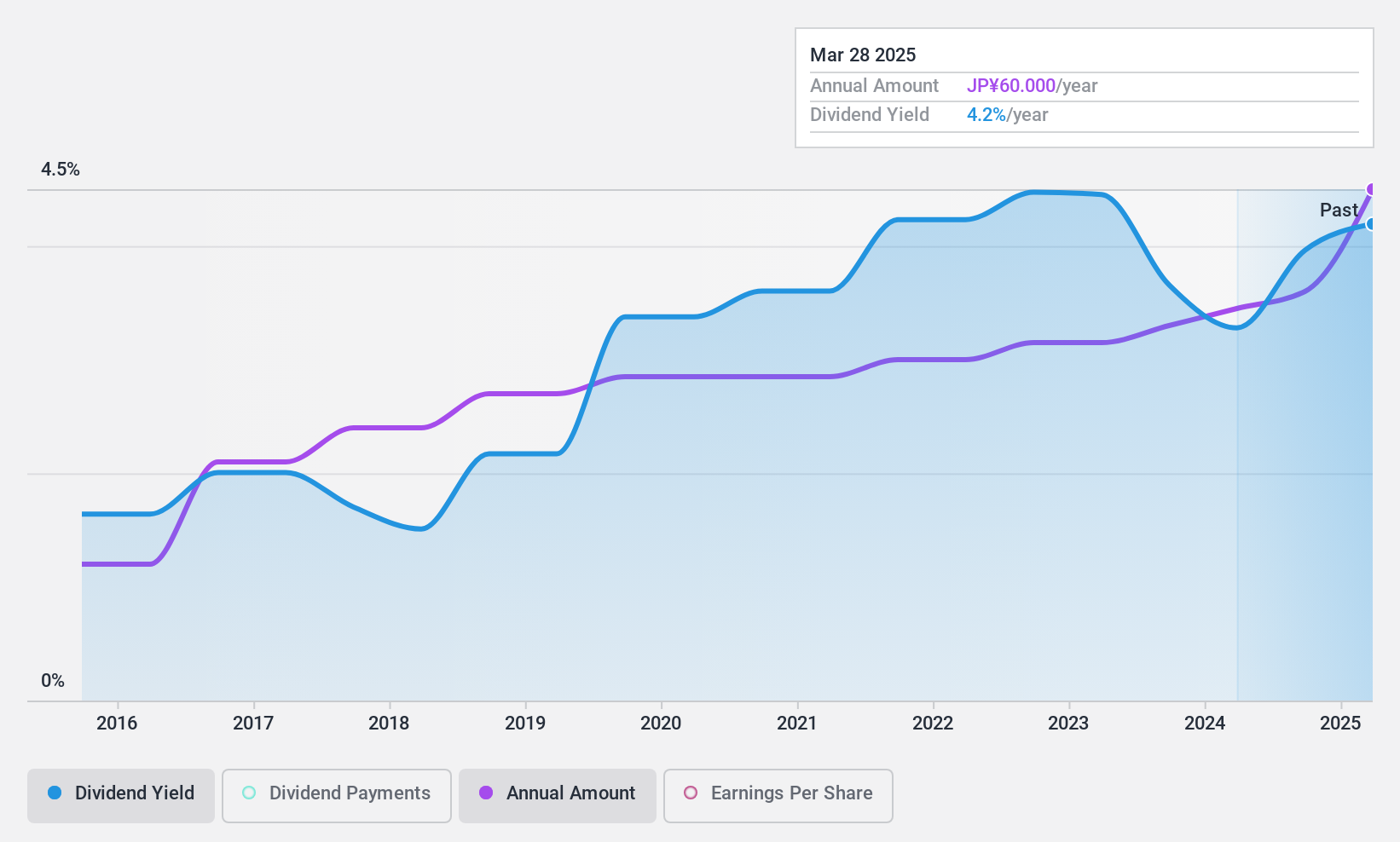

Nihon Tokushu Toryo (TSE:4619)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Nihon Tokushu Toryo Co., Ltd. manufactures and sells automobile products, paints, and coatings in Japan, with a market cap of ¥29.87 billion.

Operations: Nihon Tokushu Toryo Co., Ltd.'s revenue segments include ¥22.61 billion from paint-related products and ¥43.29 billion from automotive products-related sales.

Dividend Yield: 3.4%

Nihon Tokushu Toryo has shown consistent dividend growth over the past decade, recently increasing its semi-annual dividend to JPY 22.00 per share. With a low payout ratio of 24% and a cash payout ratio of 33.4%, dividends are well covered by earnings and cash flows, indicating sustainability. Although trading below estimated fair value, its dividend yield of 3.42% is slightly lower than Japan's top quartile payers, yet remains reliable with stable historical payouts.

- Click to explore a detailed breakdown of our findings in Nihon Tokushu Toryo's dividend report.

- Upon reviewing our latest valuation report, Nihon Tokushu Toryo's share price might be too pessimistic.

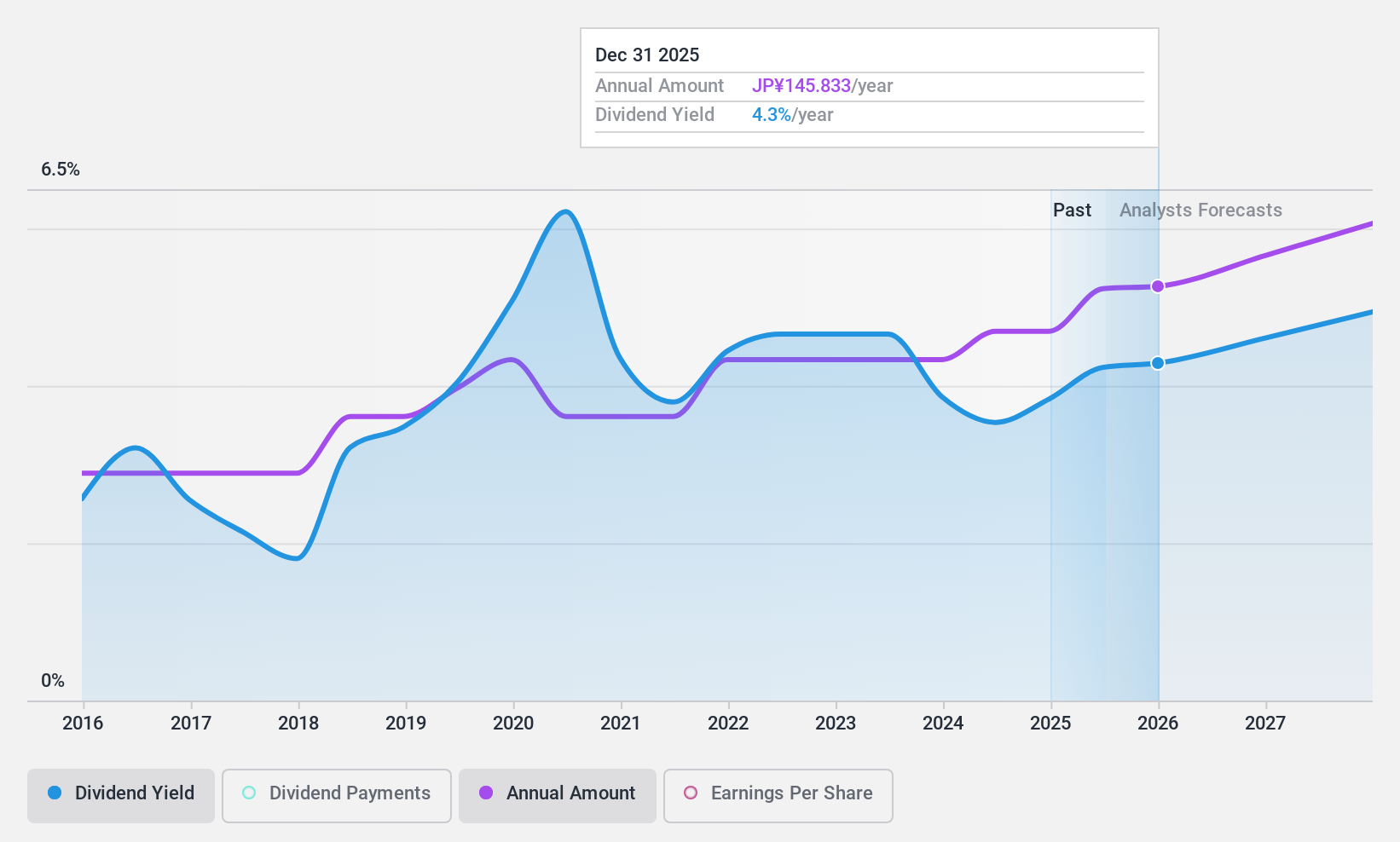

Nippon Electric Glass (TSE:5214)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Nippon Electric Glass Co., Ltd. and its subsidiaries manufacture and sell specialty glass products and glass making machinery both in Japan and internationally, with a market cap of ¥298.81 billion.

Operations: Nippon Electric Glass Co., Ltd. generates revenue through its specialty glass products and glass making machinery, serving both domestic and international markets.

Dividend Yield: 3.5%

Nippon Electric Glass has a dividend yield of 3.84%, placing it in the top 25% of Japanese payers, though its dividend history is volatile and unreliable. The company's dividends are covered by earnings with a payout ratio of 52.5% and cash flows at a cash payout ratio of 78.9%. A recent share buyback program aims to enhance shareholder returns, repurchasing up to ¥20 billion worth of shares, reflecting efforts to improve capital efficiency.

- Navigate through the intricacies of Nippon Electric Glass with our comprehensive dividend report here.

- Our expertly prepared valuation report Nippon Electric Glass implies its share price may be lower than expected.

Where To Now?

- Dive into all 1959 of the Top Dividend Stocks we have identified here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toa Road might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1882

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor