Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Enel SpA (BIT:ENEL) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Enel

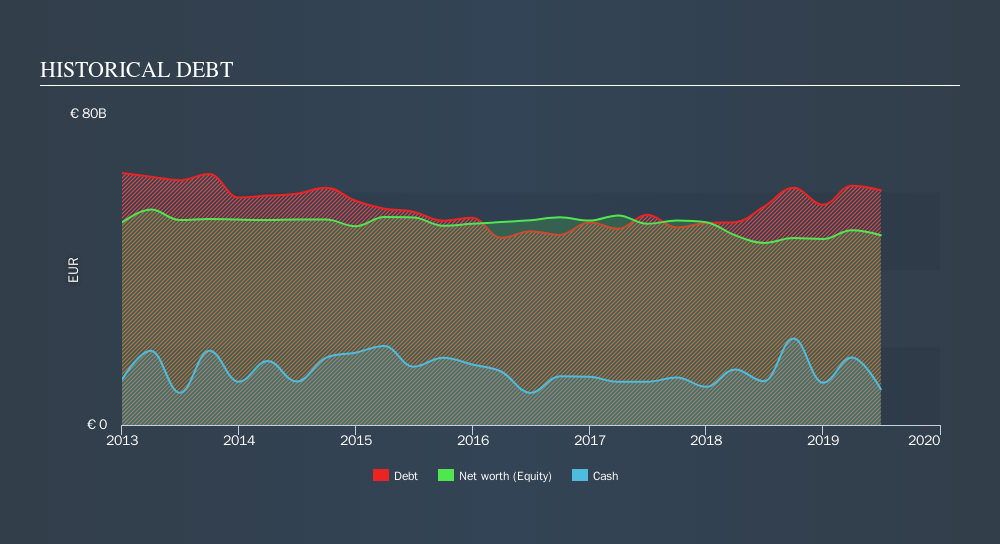

What Is Enel's Net Debt?

As you can see below, at the end of June 2019, Enel had €60.4b of debt, up from €56.2b a year ago. Click the image for more detail. However, because it has a cash reserve of €9.18b, its net debt is less, at about €51.2b.

How Strong Is Enel's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Enel had liabilities of €40.0b due within 12 months and liabilities of €81.6b due beyond that. Offsetting these obligations, it had cash of €9.18b as well as receivables valued at €19.1b due within 12 months. So it has liabilities totalling €93.4b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's massive market capitalization of €70.5b, we think shareholders really should watch Enel's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Enel has a debt to EBITDA ratio of 3.4 and its EBIT covered its interest expense 4.3 times. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Given the debt load, it's hardly ideal that Enel's EBIT was pretty flat over the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Enel can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Enel created free cash flow amounting to 18% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Mulling over Enel's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. Having said that, its ability to grow its EBIT isn't such a worry. It's also worth noting that Enel is in the Electric Utilities industry, which is often considered to be quite defensive. Looking at the bigger picture, it seems clear to us that Enel's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. Given Enel has a strong balance sheet is profitable and pays a dividend, it would be good to know how fast its dividends are growing, if at all. You can find out instantly by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About BIT:ENEL

Enel

Operates as an integrated operator in electricity and gas industries worldwide.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor