A2A (BIT:A2A) has been catching attention as investors digest its recent share price performance. Over the past month, the stock has climbed by about 6%, continuing a pattern of moderate returns this year.

The recent momentum in A2A’s share price suggests investors are warming up to its outlook. A steady 1-year total shareholder return of 18% reflects both renewed confidence and the company’s ability to navigate a changing utilities landscape.

With shares advancing and expectations running high, the key question emerges: is A2A’s current price a bargain for savvy investors, or has the market already factored in all future growth potential?

Advertisement

Most Popular Narrative: 10% Undervalued

With the latest close at €2.23 and the narrative's fair value sitting higher at €2.49, bullish expectations are shaping the outlook. The market appears to be weighing a steady transformation story against near-term headwinds.

Early and significant engagement in the circular economy, demonstrated by robust waste treatment and district heating results and a strong pipeline backed by EU landfill directives, ensures A2A is well placed to capture secular growth in recycling, waste-to-energy, and water-cycle services. This supports durable top-line and margin expansion as EU mandates tighten.

Curious how grid investments and green ambitions are shaping this price target? The real story lies in forecasts for declining profits but rising valuation multiples. Only the boldest earnings assumptions could justify this premium. Find out which catalysts analysts believe tip the scales.

However, regulatory delays or unexpected concession costs could easily outpace forecasts. This could shift the narrative and challenge current bullish assumptions.

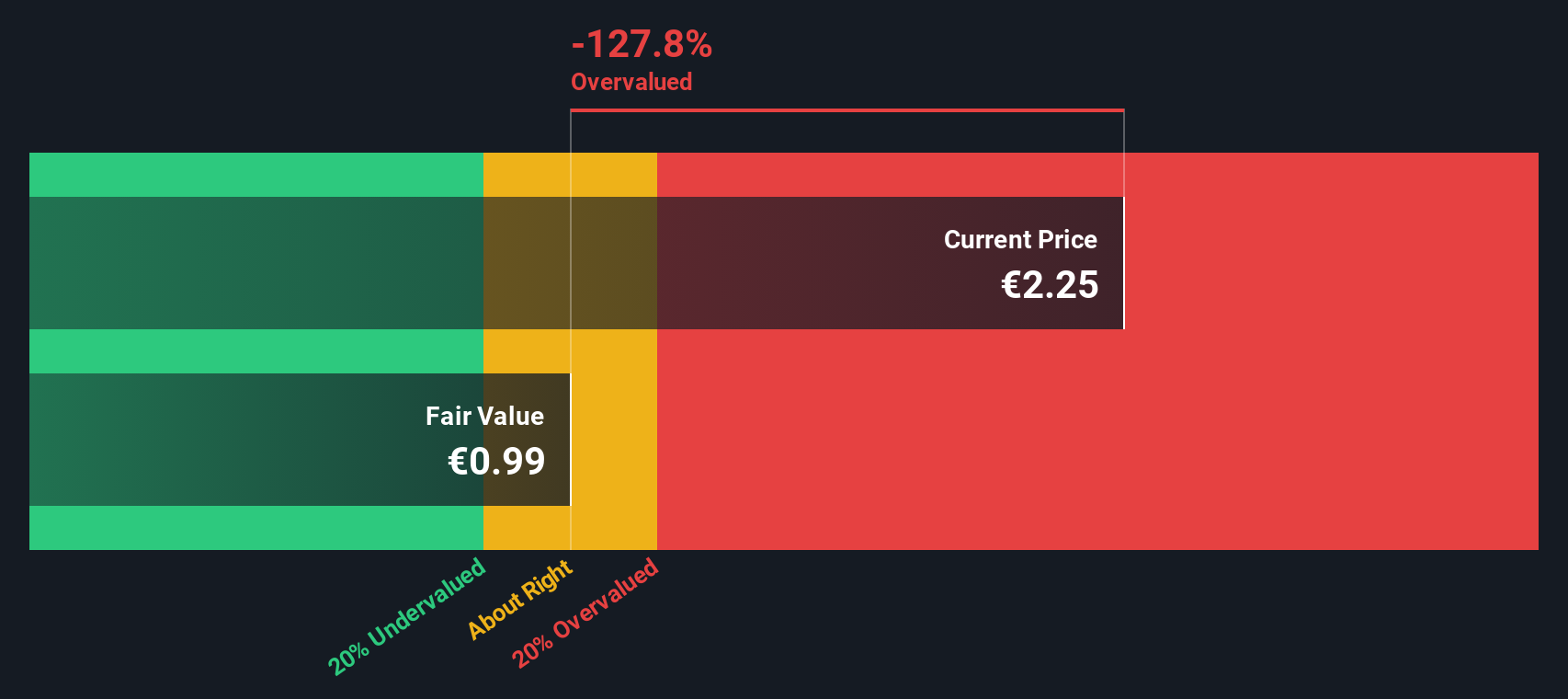

While analysts’ consensus values A2A at €2.49, our SWS DCF model presents a different perspective. It estimates the company’s fair value at just €0.99 per share, which is significantly below today’s price. This sharp difference raises the question: are growth assumptions and investor optimism running too high?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out A2A for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own A2A Narrative

If you have a different perspective or want to dig into the data firsthand, you can shape your own view in just a few minutes. Do it your way.

Set your sights on opportunities you might be missing. Simply Wall Street’s powerful screener spotlights stocks across hot sectors and under-the-radar gems you wish you’d found sooner.

Ride the AI wave and catch early movers by checking out these 24 AI penny stocks pushing boundaries in artificial intelligence.

Make your mark on tomorrow's tech trends by exploring these 26 quantum computing stocks that are pioneering quantum computing breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks