Advertisement

Datalogic (BIT:DAL) May Have Issues Allocating Its Capital

When researching a stock for investment, what can tell us that the company is in decline? When we see a declining return on capital employed (ROCE) in conjunction with a declining base of capital employed, that's often how a mature business shows signs of aging. Trends like this ultimately mean the business is reducing its investments and also earning less on what it has invested. In light of that, from a first glance at Datalogic (BIT:DAL), we've spotted some signs that it could be struggling, so let's investigate.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Datalogic is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

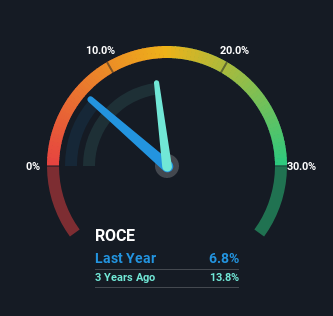

0.068 = €38m ÷ (€871m - €311m) (Based on the trailing twelve months to June 2022).

So, Datalogic has an ROCE of 6.8%. On its own, that's a low figure but it's around the 8.4% average generated by the Electronic industry.

Check out our latest analysis for Datalogic

Above you can see how the current ROCE for Datalogic compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

So How Is Datalogic's ROCE Trending?

There is reason to be cautious about Datalogic, given the returns are trending downwards. Unfortunately the returns on capital have diminished from the 13% that they were earning five years ago. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on Datalogic becoming one if things continue as they have.

What We Can Learn From Datalogic's ROCE

In summary, it's unfortunate that Datalogic is generating lower returns from the same amount of capital. It should come as no surprise then that the stock has fallen 65% over the last five years, so it looks like investors are recognizing these changes. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

One more thing, we've spotted 2 warning signs facing Datalogic that you might find interesting.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:DAL

Datalogic

Designs and produces barcode readers, mobile computers, detection, measurement and safety sensors, vision and laser marking systems, and RFID products in Italy, the Americas, the Asia Pacific, rest of Europe, the Middle East, and Africa.

Flawless balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.1% undervalued

210 followersusers have followed this narrative

1 commentusers have commented on this narrative

30 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.6% undervalued

53 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0719.6% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3814.1% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36039.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Fibromat (M) Berhad ·

Fibromat: More than just a niche player, with clearer earnings visibility from order book and project wins

Fair Value:RM 1.0519.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Ceres ·

Proven business incubator in transition

Fair Value:JP¥2.37k36.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.6% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.5% undervalued

1348 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0