Advertisement

This Analyst Just Wrote A Brand New Outlook For TXT e-solutions S.p.A.'s (BIT:TXT) Business

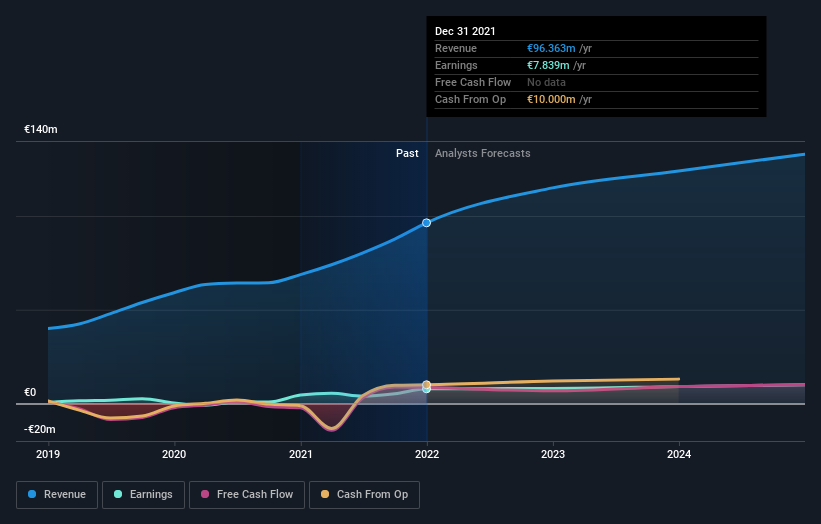

TXT e-solutions S.p.A. (BIT:TXT) shareholders will have a reason to smile today, with the covering analyst making substantial upgrades to this year's statutory forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects. The stock price has risen 6.3% to €9.69 over the past week, suggesting investors are becoming more optimistic. Whether the upgrade is enough to drive the stock price higher is yet to be seen, however.

Following the upgrade, the latest consensus from TXT e-solutions' single analyst is for revenues of €115m in 2022, which would reflect a decent 19% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to be €0.66, roughly flat on the last 12 months. Prior to this update, the analyst had been forecasting revenues of €103m and earnings per share (EPS) of €0.59 in 2022. There has definitely been an improvement in perception recently, with the analyst substantially increasing both their earnings and revenue estimates.

Check out our latest analysis for TXT e-solutions

With these upgrades, we're not surprised to see that the analyst has lifted their price target 6.3% to €13.50 per share.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the TXT e-solutions' past performance and to peers in the same industry. We can infer from the latest estimates that forecasts expect a continuation of TXT e-solutions'historical trends, as the 19% annualised revenue growth to the end of 2022 is roughly in line with the 21% annual revenue growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 20% annually. So although TXT e-solutions is expected to maintain its revenue growth rate, it's only growing at about the rate of the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that the analyst upgraded their earnings per share estimates for this year, expecting improving business conditions. There was also an upgrade to revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, TXT e-solutions could be worth investigating further.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2024, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if TXT e-solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:TXT

TXT e-solutions

Provides software and service solutions in Italy and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor