Reply (BIT:REY) is catching some eyes this week as its shares reversed course after a challenging stretch, closing the day up roughly 0.2%. While the move is modest, it stands out against a backdrop of extended weakness for the stock. For investors sizing up whether to buy, the question is less about the day-to-day headlines and more about whether this uptick could be signaling something about changing sentiment or simply a pause within a longer downtrend.

If you zoom out further, it is clear Reply’s story has been about managing shifting expectations. After strong multi-year gains, shares have dropped over the past year, falling about 10%. Over the past 3 months, momentum lagged, and the year-to-date decline sits around 23%. These stumbles come despite revenue and net income both growing at a steady pace. This suggests investors may be grappling with how much of Reply’s growth is already reflected in its price.

So with the stock drifting down this year even as the business keeps growing, is the market offering a bargain right now, or are investors right to question how much more upside is left?

Advertisement

Price-to-Earnings of 19x: Is it justified?

Reply’s current valuation looks attractive when measured against peers. Its price-to-earnings (P/E) ratio is 19x, which is significantly lower than the sector average of 51.6x. This suggests the stock may offer relatively better value than similar companies in the software industry.

The price-to-earnings ratio compares a company’s market price to its earnings per share, offering insight into how much investors are willing to pay for each euro of earnings. For technology and software firms, this metric is especially telling as it often signals the market’s future growth expectations.

This lower P/E multiple could indicate that the market is underestimating Reply’s ability to grow profits in the future or is cautious about its growth durability. It leaves the door open for upside if the company continues to outperform on its fundamentals.

However, slower revenue growth or continued investor skepticism could prevent shares from rebounding quickly, particularly if industry sentiment remains fragile.

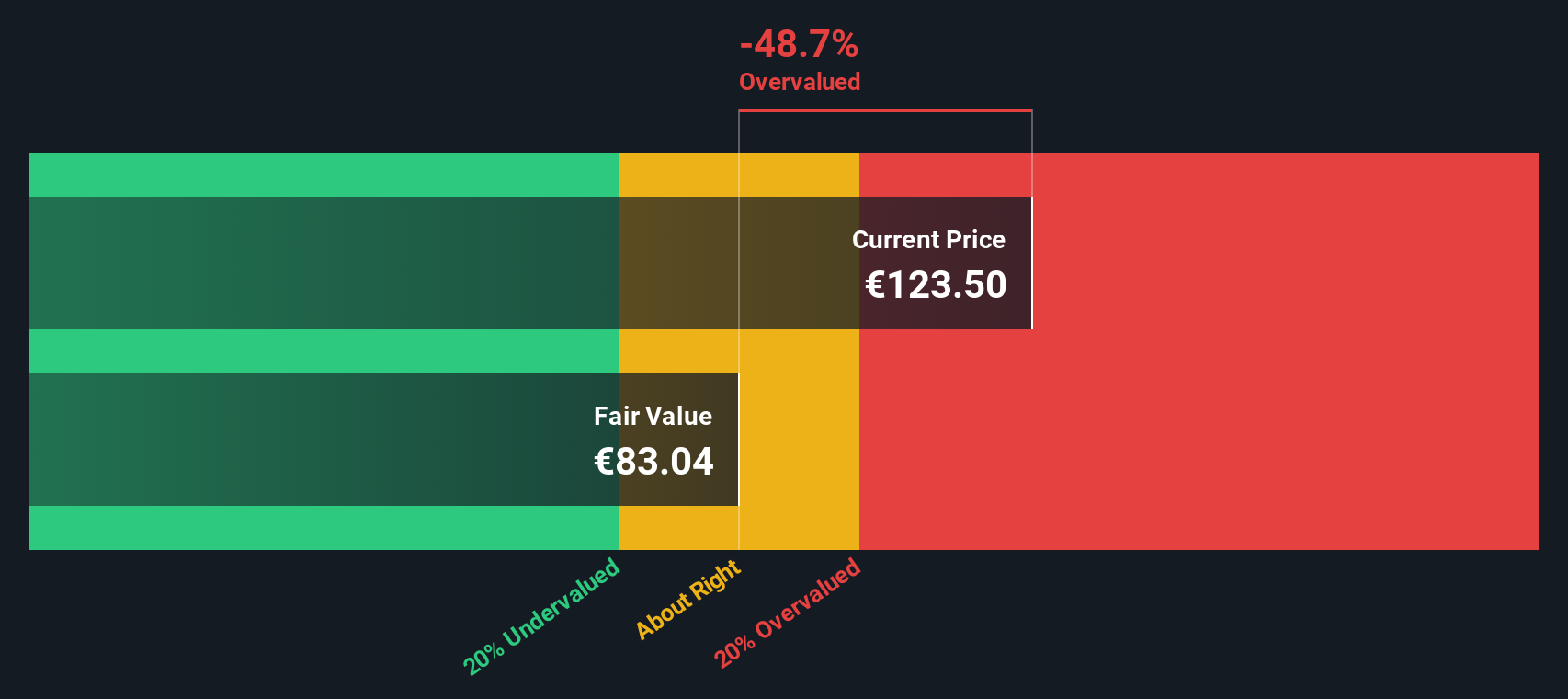

Another View: Discounted Cash Flow Paints a Different Picture

Taking a step back, our DCF model arrives at a very different conclusion. By focusing on cash flows rather than earnings, this approach suggests Reply could actually be overvalued at current prices. Does this signal caution? Or is the market seeing something the models miss?

If you want to dig into the numbers yourself or see things from a different angle, you can shape your own reply in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Reply.

Looking for more investment ideas?

Expand your horizons and catch the next winning trend. Don’t let opportunity pass by while others get ahead. Let Simply Wall Street’s expert screeners help you zero in on new opportunities:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.