Advertisement

While shareholders of Class Editori (BIT:CLE) are in the black over 3 years, those who bought a week ago aren't so fortunate

It certainly might concern Class Editori Spa (BIT:CLE) shareholders to see the share price down 31% in just 30 days. In contrast the stock is up over the last three years. However, it's unlikely many shareholders are elated with the share price gain of 74% over that time, given the rising market.

Since the long term performance has been good but there's been a recent pullback of 11%, let's check if the fundamentals match the share price.

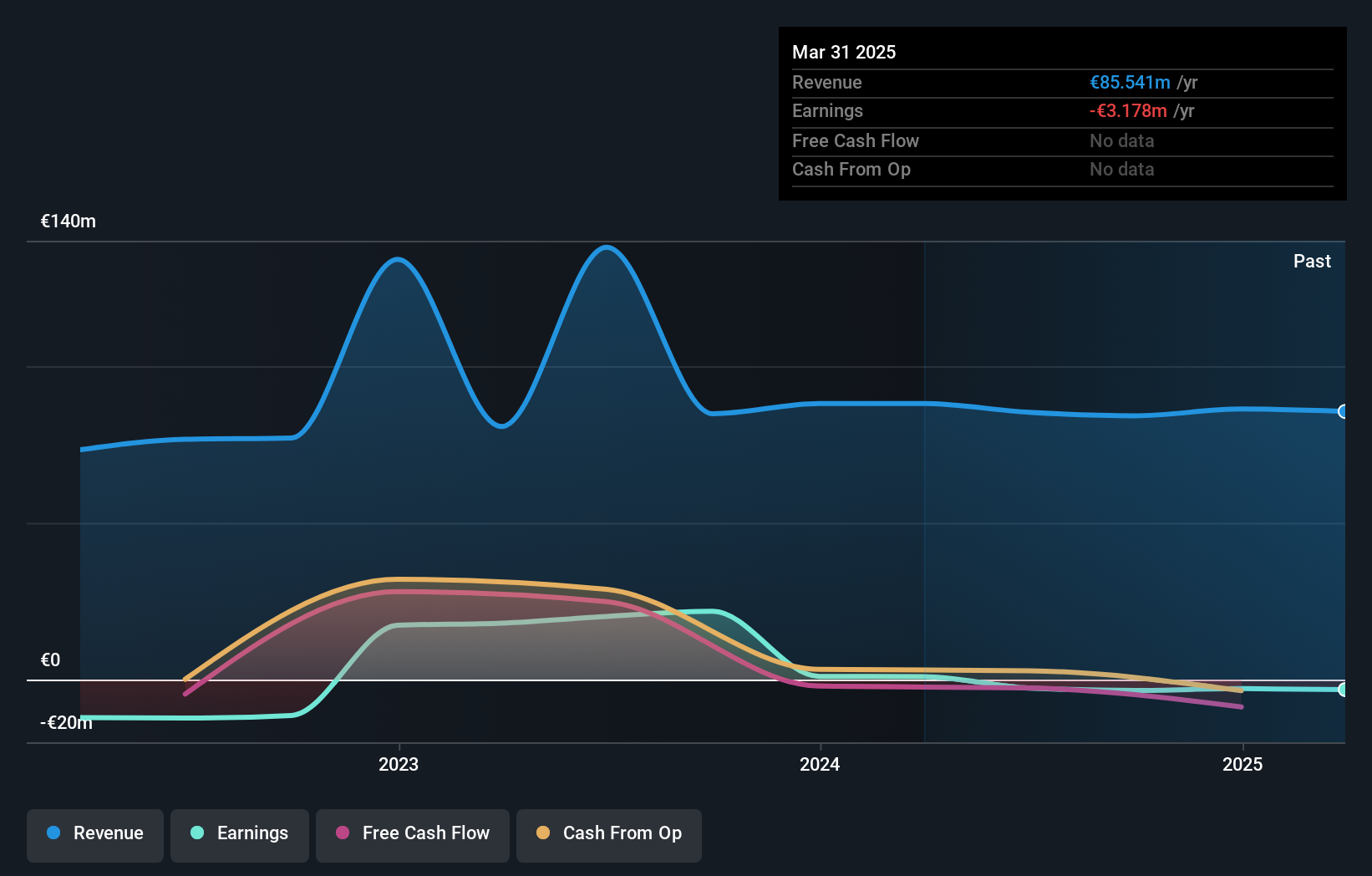

Given that Class Editori didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

Class Editori actually saw its revenue drop by 0.8% per year over three years. Despite the lack of revenue growth, the stock has returned 20%, compound, over three years. Unless the company is going to make profits soon, we would be pretty cautious about it.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

Take a more thorough look at Class Editori's financial health with this free report on its balance sheet.

A Different Perspective

It's nice to see that Class Editori shareholders have received a total shareholder return of 47% over the last year. Since the one-year TSR is better than the five-year TSR (the latter coming in at 1.7% per year), it would seem that the stock's performance has improved in recent times. In the best case scenario, this may hint at some real business momentum, implying that now could be a great time to delve deeper. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 3 warning signs for Class Editori (1 is a bit concerning!) that you should be aware of before investing here.

But note: Class Editori may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Italian exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:CLE

Low and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor