Advertisement

- Italy

- /

- Healthcare Services

- /

- BIT:GHC

Are Garofalo Health Care's (BIT:GHC) Statutory Earnings A Good Guide To Its Underlying Profitability?

It might be old fashioned, but we really like to invest in companies that make a profit, each and every year. That said, the current statutory profit is not always a good guide to a company's underlying profitability. This article will consider whether Garofalo Health Care's (BIT:GHC) statutory profits are a good guide to its underlying earnings.

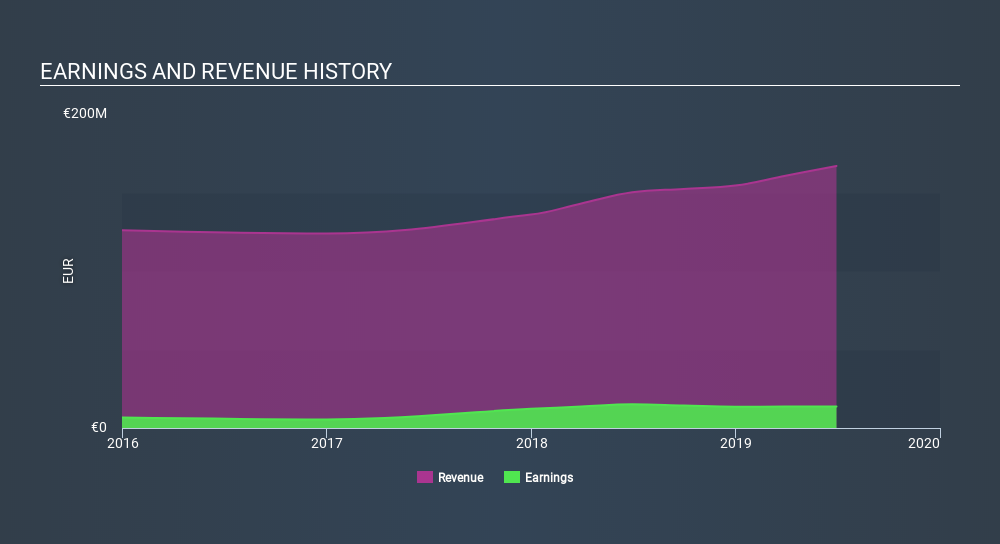

While Garofalo Health Care was able to generate revenue of €166.9m in the last twelve months, we think its profit result of €13.7m was more important. In the chart below, you can see that its profit and revenue have both grown over the last three years, although its profit has slipped in the last twelve months.

View our latest analysis for Garofalo Health Care

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. Therefore, today we will consider the nature of Garofalo Health Care's statutory earnings with reference to its dilution of shareholders and the impact of unusual items. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, Garofalo Health Care increased the number of shares on issue by 55% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of Garofalo Health Care's EPS by clicking here.

A Look At The Impact Of Garofalo Health Care's Dilution on Its Earnings Per Share (EPS).

Garofalo Health Care has improved its profit over the last three years, with an annualized gain of 127% in that time. In comparison, earnings per share only gained 46% over the same period. Net income was down 8.8% over the last twelve months. Unfortunately for shareholders, though, the earnings per share result was even worse, declining 41%. So you can see that the dilution has had a fairly significant impact on shareholders.

If Garofalo Health Care's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

The Impact Of Unusual Items On Profit

Alongside that dilution, it's also important to note that Garofalo Health Care's profit suffered from unusual items, which reduced profit by €2.9m in the last twelve months. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. Assuming those unusual expenses don't come up again, we'd therefore expect Garofalo Health Care to produce a higher profit next year, all else being equal.

Our Take On Garofalo Health Care's Profit Performance

To sum it all up, Garofalo Health Care took a hit from unusual items which pushed its profit down; without that, it would have made more money. But unfortunately the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). That will weigh on earnings per share, even if it is not reflected in net income. Based on these factors, we think it's very unlikely that Garofalo Health Care's statutory profits make it seem much weaker than it is. While it's really important to consider how well a company's statutory earnings represent its true earnings power, it's also worth taking a look at what analysts are forecasting for the future. So feel free to check out our free graph representing analyst forecasts.

Our examination of Garofalo Health Care has focussed on certain factors that can make its earnings look better than they are. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About BIT:GHC

Fair value with limited growth.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor