Eni (BIT:ENI) has captured fresh interest lately as investors take a closer look at its performance. Shares saw a small dip this past week but remain up 13% over the past year. There are several longer-term trends worth noticing here.

After a year that has seen some ups and downs, Eni’s recent share price movement hints at cooling short-term momentum. Its 1-year total shareholder return of 13.3% shows investors have still been rewarded for staying the course.

With Eni shares up strongly over the longer term but modestly below analyst price targets, the real question is whether the stock still offers value at current levels or if expectations for future growth are already built in.

Advertisement

Most Popular Narrative: 3.1% Undervalued

With Eni's fair value estimated at €15.35, just above the latest closing price of €14.88, the prevailing narrative sees modest upside potential. Analyst consensus frames the current price as slightly undervalued, with a tight margin signaling balanced market expectations.

Eni's strategic expansion in LNG, highlighted by leading floating LNG investments in Africa, the Eastern Mediterranean, and new ventures in Argentina and Southeast Asia, positions the company to capture rising global demand for diverse and secure natural gas supplies. This geographic and product diversification is expected to drive future revenue and stabilize earnings amid energy transition volatility.

Wondering what bold assumptions power this valuation? The big story centers on ambitious growth in future earnings and profit margins, plus a profit multiple that reflects changing energy dynamics. Unpack the full methodology and discover which forecasts could swing the number further in either direction.

However, persistent losses in Eni's chemicals division and delayed renewable cash neutrality could challenge future growth and place current profit expectations at risk.

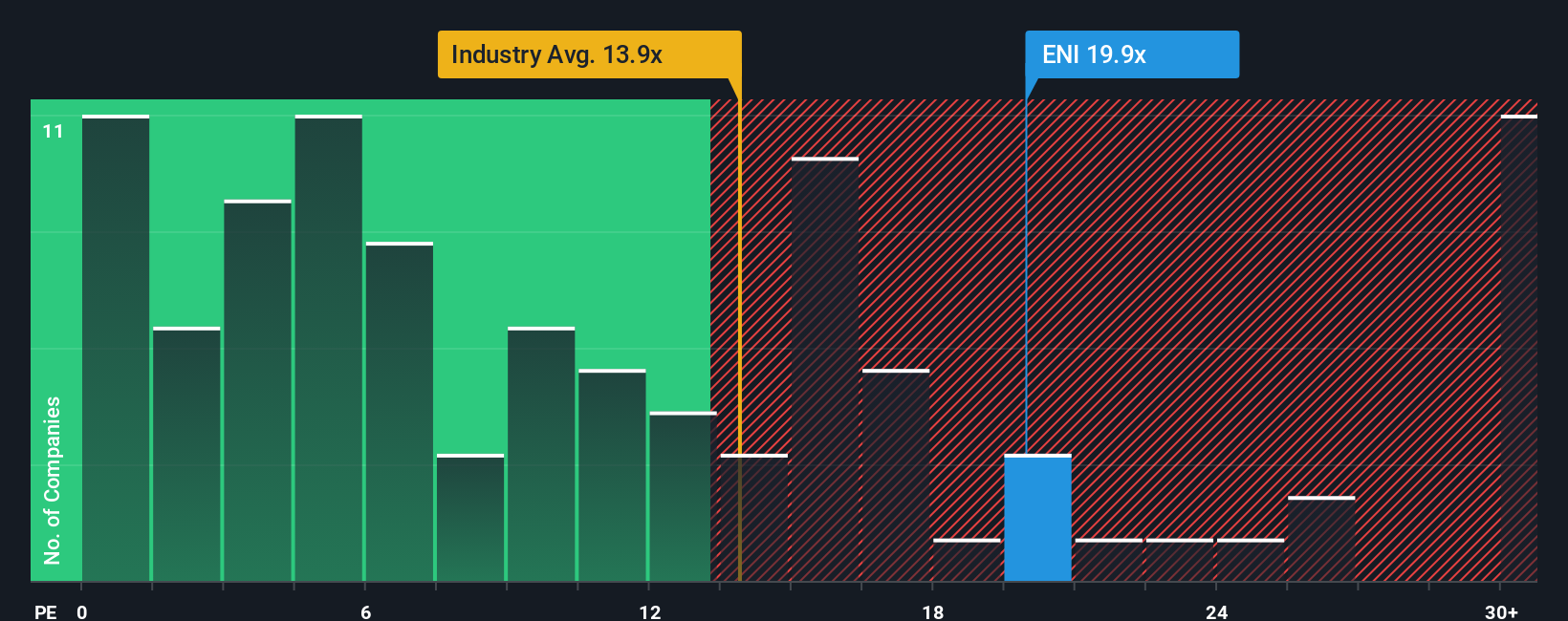

While the fair value estimate points to slight undervaluation, price-to-earnings ratios tell a different story. Eni trades at 19.8x earnings, a premium to both peers (14.6x) and the European sector (13.8x), and even above its fair ratio of 18.2x. Could this premium signal valuation risk on today’s price?

If you see the story differently or want to review the numbers for yourself, you can quickly craft your own perspective in just minutes. Do it your way

Capitalize on the transformative power of next-gen health solutions with these 31 healthcare AI stocks making waves in AI-driven medical advances.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eni might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.