Advertisement

- Italy

- /

- Oil and Gas

- /

- BIT:ENI

A Fresh Look at Eni (BIT:ENI) Valuation Following Its Recent Share Price Movement

Simply Wall St

Reviewed by Kshitija Bhandaru

Eni (BIT:ENI) shares have seen modest movement over the past week, with a slight dip of almost 2%. Investors are evaluating the stock’s current price in comparison to its recent three month climb of almost 7%.

See our latest analysis for Eni.

Looking beyond this week’s move, Eni’s short-term momentum shows some signs of fading after its strong run over the past quarter. Still, the 1-year total shareholder return sits at a solid 13.3%, suggesting that patient investors who benefited from dividends and buybacks have outperformed simple share price returns in the same period.

If you’re curious where else strong momentum and management alignment are driving results, now could be a great time to discover fast growing stocks with high insider ownership

The question now facing investors is whether Eni’s recent pullback reveals a market underestimating its future growth, or if the stock’s current price already includes all the optimism about its prospects.

Most Popular Narrative: 3.1% Undervalued

Eni’s fair value estimate now stands at €15.35, which is just above the last close of €14.88. The narrative’s close gap to market price makes the underlying forecasts particularly important to understand.

Eni's strategic expansion in LNG, highlighted by leading floating LNG investments in Africa, the Eastern Mediterranean, and new ventures in Argentina and Southeast Asia, positions the company to capture rising global demand for diverse and secure natural gas supplies. This geographic and product diversification is expected to drive future revenue and stabilize earnings amid energy transition volatility.

What is fueling this “undervalued” story? One set of aggressive profit projections, ambitious margin expansion plans, and a rare multiple downgrade not typical for this sector. Want to uncover the numbers powering this view and why so many analysts buy in? Don’t miss the full narrative; it puts a bold spin on Eni’s next chapter.

Result: Fair Value of €15.35 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent losses in legacy chemicals and delayed renewable profitability could threaten Eni's growth outlook if improvements do not occur soon.

Find out about the key risks to this Eni narrative.

Another View: Multiples Tell a Different Story

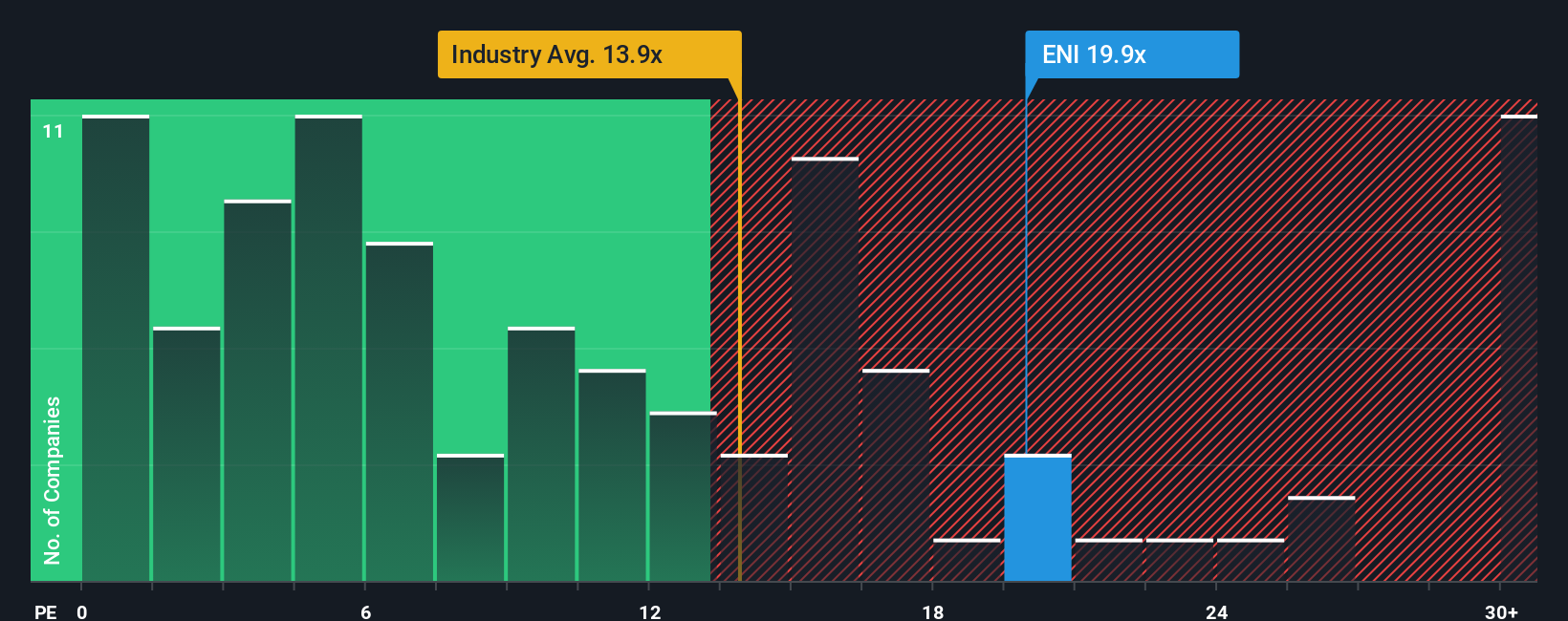

Looking at Eni’s valuation through the lens of its price-to-earnings ratio reveals a different angle. Eni trades at 19.8x earnings, making it pricier than both its industry peers (average 13.8x) and the market’s fair ratio of 18.2x. This suggests investors are paying a premium, potentially increasing valuation risk if growth does not accelerate. Could the market be too optimistic, or does this premium reflect unseen strengths?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Eni Narrative

If you see a different story in the data or want to dig deeper into the details yourself, it takes less than three minutes to build your own view. Do it your way.

A great starting point for your Eni research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t let opportunity pass you by. Expand your horizon and uncover new stocks with growth, innovation, or stable returns that others may be overlooking.

- Capitalize on standout yields and steady income by checking out these 19 dividend stocks with yields > 3% with returns over 3%.

- Spot tomorrow’s tech leaders by scanning these 24 AI penny stocks as they make breakthroughs in artificial intelligence.

- Strengthen your portfolio with value-driven picks using these 907 undervalued stocks based on cash flows based on real company cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eni might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:ENI

Eni

Operates as an integrated energy company in Italy, Other European Union, Rest of Europe, the United States, Asia, Africa, and internationally.

Excellent balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor