Advertisement

- Italy

- /

- Aerospace & Defense

- /

- BIT:TPS

Investors Could Be Concerned With Technical Publications Service's (BIT:TPS) Returns On Capital

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Having said that, from a first glance at Technical Publications Service (BIT:TPS) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Technical Publications Service is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.17 = €5.2m ÷ (€41m - €10m) (Based on the trailing twelve months to December 2021).

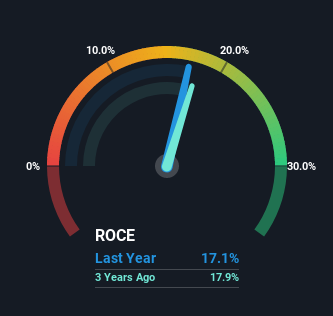

Thus, Technical Publications Service has an ROCE of 17%. On its own, that's a standard return, however it's much better than the 7.6% generated by the Aerospace & Defense industry.

See our latest analysis for Technical Publications Service

Historical performance is a great place to start when researching a stock so above you can see the gauge for Technical Publications Service's ROCE against it's prior returns. If you'd like to look at how Technical Publications Service has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

The Trend Of ROCE

In terms of Technical Publications Service's historical ROCE movements, the trend isn't fantastic. Over the last five years, returns on capital have decreased to 17% from 59% five years ago. Although, given both revenue and the amount of assets employed in the business have increased, it could suggest the company is investing in growth, and the extra capital has led to a short-term reduction in ROCE. If these investments prove successful, this can bode very well for long term stock performance.

On a side note, Technical Publications Service has done well to pay down its current liabilities to 25% of total assets. So we could link some of this to the decrease in ROCE. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

The Bottom Line On Technical Publications Service's ROCE

In summary, despite lower returns in the short term, we're encouraged to see that Technical Publications Service is reinvesting for growth and has higher sales as a result. In light of this, the stock has only gained 11% over the last five years. So this stock may still be an appealing investment opportunity, if other fundamentals prove to be sound.

Like most companies, Technical Publications Service does come with some risks, and we've found 1 warning sign that you should be aware of.

While Technical Publications Service may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Technical Publications Service might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:TPS

Technical Publications Service

Engages in the provision of engineering and digital services in Italy.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.0% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.1% undervalued

ME

Community Contributor