Advertisement

Iveco Group (BIT:IVG) Will Pay A Larger Dividend Than Last Year At €0.33

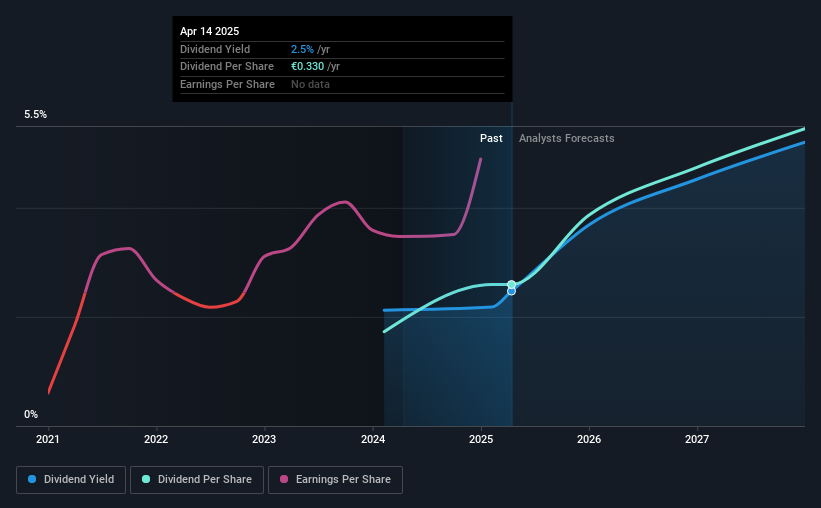

The board of Iveco Group N.V. (BIT:IVG) has announced that it will be paying its dividend of €0.33 on the 24th of April, an increased payment from last year's comparable dividend. This will take the annual payment to 2.5% of the stock price, which is above what most companies in the industry pay.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Iveco Group's stock price has increased by 43% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

We've discovered 2 warning signs about Iveco Group. View them for free.Iveco Group's Future Dividend Projections Appear Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Before making this announcement, Iveco Group was easily earning enough to cover the dividend. This means that most of what the business earns is being used to help it grow.

Over the next year, EPS is forecast to expand by 29.2%. If the dividend continues along recent trends, we estimate the payout ratio will be 13%, which is in the range that makes us comfortable with the sustainability of the dividend.

View our latest analysis for Iveco Group

Iveco Group Doesn't Have A Long Payment History

It is tough to make a judgement on how stable a dividend is when the company hasn't been paying one for very long. This doesn't mean that the company can't pay a good dividend, but just that we want to wait until it can prove itself.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. Iveco Group has seen EPS rising for the last three years, at 119% per annum. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

Iveco Group Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Earnings are easily covering distributions, and the company is generating plenty of cash. All in all, this checks a lot of the boxes we look for when choosing an income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 2 warning signs for Iveco Group you should be aware of, and 1 of them is a bit unpleasant. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:IVG

Iveco Group

Engages in the design, production, marketing, sale, servicing, and financing of trucks, commercial vehicles, buses and specialty vehicles, combustion engines, alternative propulsion systems, transmissions, axles, engines, alternative propulsion systems, construction equipment, marine, and power generation applications in Europe, South America, North America, and internationally.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor