If you have been tracking Brembo (BIT:BRE), you may have noticed its shares have been moving in a way that could leave you wondering whether the market sees something others are missing or if this is just noise. There is no single groundbreaking event behind the recent price action. Sometimes it is these quieter moves that end up signaling a shift in how investors view a company’s prospects.

Over the past year, Brembo’s stock has given up around 7%, lagging the broader market and suggesting sentiment has cooled after stronger gains in recent years. Still, the stock is up 19% over the past three months and about 26% in the past five years, hinting that momentum may be rebuilding. Annual results also show revenue and profit advancing in the right direction, though at a pace that some might call measured rather than explosive.

With shares staging a noticeable short-term rebound after a disappointing year, the critical question is whether Brembo offers real value at current prices or if the market is already anticipating better days ahead.

Advertisement

Price-to-Earnings of 14.4x: Is it justified?

Brembo is currently valued at a price-to-earnings (P/E) ratio of 14.4x. This is higher than both the European Auto Components industry average of 13.1x and the peer average of 12.5x. This suggests the stock may be priced at a premium relative to its sector.

The price-to-earnings multiple measures how much investors are willing to pay for each euro of earnings. In the auto parts space, this ratio often reflects expectations for future growth, profitability, and stability within a cyclical industry.

The market appears to expect more from Brembo compared to its peers, possibly due to its history of high quality earnings or anticipated profit growth. However, paying a premium in this sector usually requires strong evidence of outperformance in the years to come.

However, lingering industry challenges or slower than expected profit growth could quickly unravel the current optimism and pressure the share price once again.

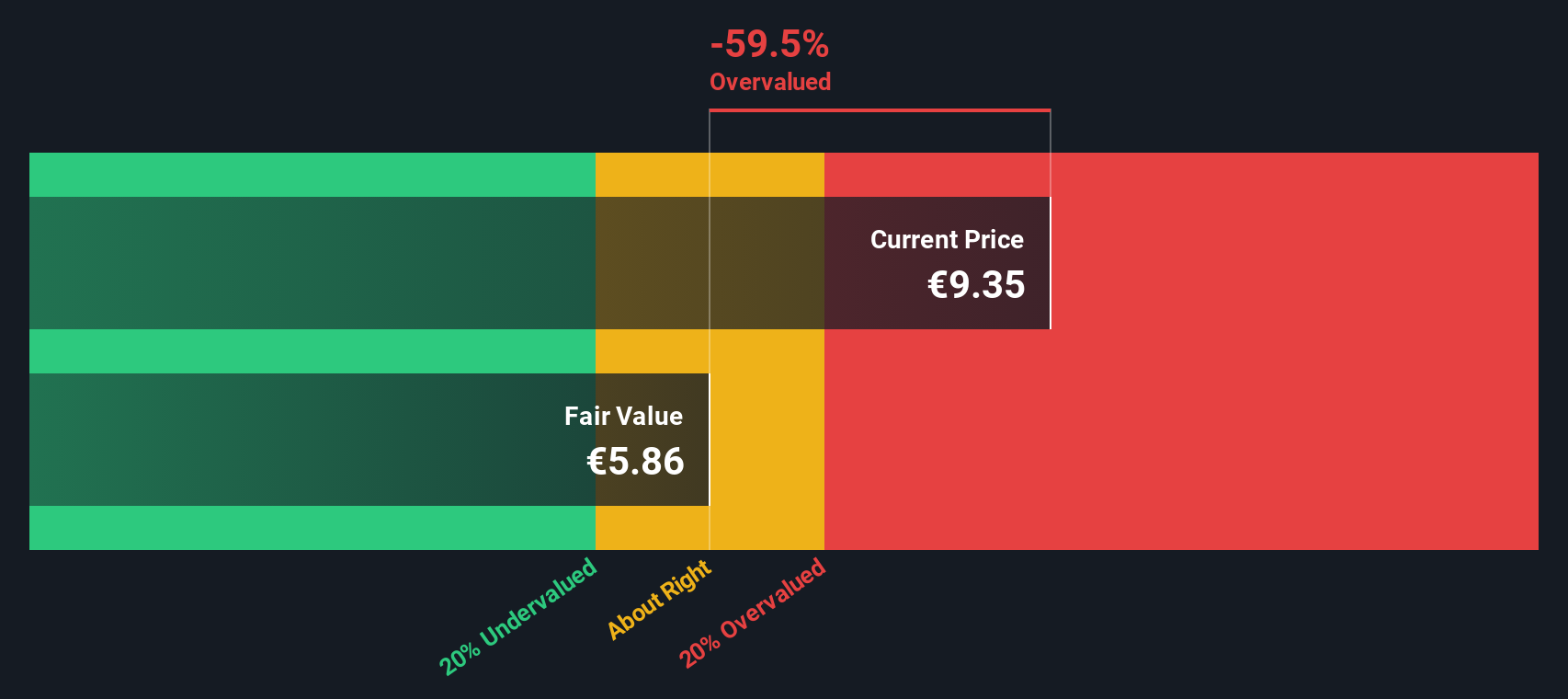

Looking through the lens of our DCF model, a different picture emerges. This approach suggests Brembo is actually trading above what the fundamentals justify, presenting a distinct challenge to the value seen in market multiples. Could this mean market optimism is running ahead of reality, or is something else missed in the forecasts?

Of course, if you see the data differently or want to shape your own perspective, you can easily craft a personal narrative in just a few minutes using our platform. Do it your way.

Give yourself every advantage by using the Simply Wall Street Screener to find high potential stocks that match your goals. If you hesitate, you might just miss tomorrow’s biggest opportunity.

Tap into future innovations with a curated group of quantum computing stocks paving new ground in advanced computing and technology.

Unlock value plays with stocks trading below their intrinsic worth. This gives you access to undervalued stocks based on cash flows others may have overlooked.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Brembo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.