Advertisement

- India

- /

- Gas Utilities

- /

- NSEI:GUJGASLTD

These 4 Measures Indicate That Gujarat Gas (NSE:GUJGAS) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Gujarat Gas Limited (NSE:GUJGAS) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Gujarat Gas

What Is Gujarat Gas's Net Debt?

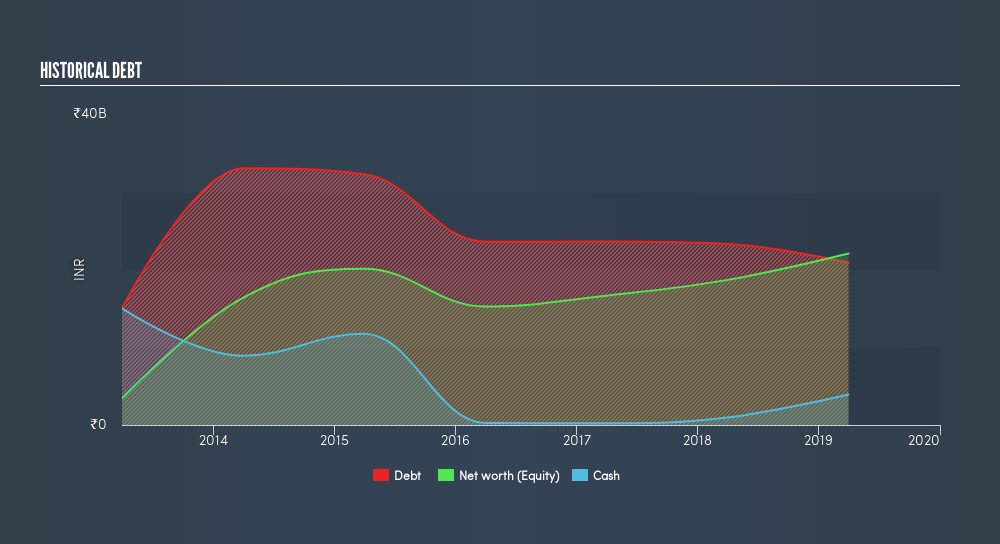

You can click the graphic below for the historical numbers, but it shows that Gujarat Gas had ₹20.9b of debt in March 2019, down from ₹23.3b, one year before On the flip side, it has ₹3.92b in cash leading to net debt of about ₹17.0b.

How Strong Is Gujarat Gas's Balance Sheet?

According to the last reported balance sheet, Gujarat Gas had liabilities of ₹16.8b due within 12 months, and liabilities of ₹32.8b due beyond 12 months. Offsetting these obligations, it had cash of ₹3.92b as well as receivables valued at ₹5.12b due within 12 months. So it has liabilities totalling ₹40.5b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Gujarat Gas is worth ₹114.0b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Since Gujarat Gas does have net debt, we think it is worthwhile for shareholders to keep an eye on the balance sheet, over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Gujarat Gas's net debt is sitting at a very reasonable 1.77 times its EBITDA, while its EBIT covered its interest expense just 3.55 times last year. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. One way Gujarat Gas could vanquish its debt would be if it stops borrowing more but conitinues to grow EBIT at around 10%, as it did over the last year. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Gujarat Gas's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Gujarat Gas's free cash flow amounted to 48% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Gujarat Gas's interest cover was a real negative on this analysis, although the other factors we considered were considerably better In particular, we thought its EBIT growth rate was a positive. We would also note that Gas Utilities industry companies like Gujarat Gas commonly do use debt without problems. Looking at all this data makes us feel a little cautious about Gujarat Gas's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Gujarat Gas's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:GUJGASLTD

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor