Advertisement

- India

- /

- Renewable Energy

- /

- NSEI:GREENPOWER

Does Orient Green Power (NSE:GREENPOWER) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Orient Green Power Company Limited (NSE:GREENPOWER) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Orient Green Power

What Is Orient Green Power's Debt?

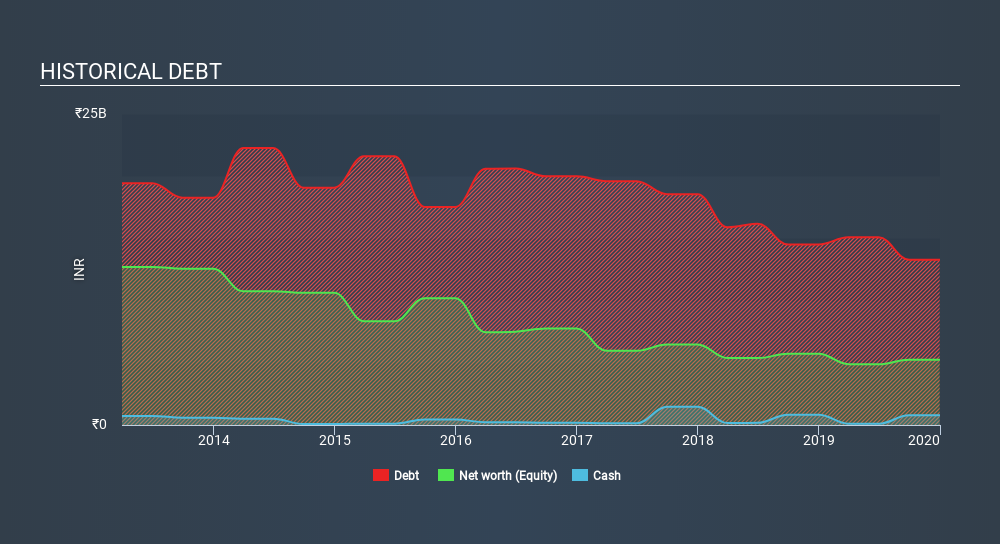

As you can see below, Orient Green Power had ₹13.3b of debt at September 2019, down from ₹14.5b a year prior. On the flip side, it has ₹784.7m in cash leading to net debt of about ₹12.5b.

How Healthy Is Orient Green Power's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Orient Green Power had liabilities of ₹4.07b due within 12 months and liabilities of ₹13.3b due beyond that. On the other hand, it had cash of ₹784.7m and ₹1.07b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹15.5b.

The deficiency here weighs heavily on the ₹938.4m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Orient Green Power would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Orient Green Power shareholders face the double whammy of a high net debt to EBITDA ratio (5.6), and fairly weak interest coverage, since EBIT is just 0.81 times the interest expense. This means we'd consider it to have a heavy debt load. On a slightly more positive note, Orient Green Power grew its EBIT at 11% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Orient Green Power will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Orient Green Power actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

On the face of it, Orient Green Power's interest cover left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Orient Green Power's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 3 warning signs we've spotted with Orient Green Power .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:GREENPOWER

Orient Green Power

An independent renewable energy company, owns, develops, and operates a portfolio of wind energy projects in India and Europe.

Adequate balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|47.8% undervalued

TO

Community Contributor