Patel Integrated Logistics Limited (NSE:PATINTLOG) Investors Should Think About This Before Buying It For Its Dividend

Today we'll take a closer look at Patel Integrated Logistics Limited (NSE:PATINTLOG) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. If you are hoping to live on the income from dividends, it's important to be a lot more stringent with your investments than the average punter.

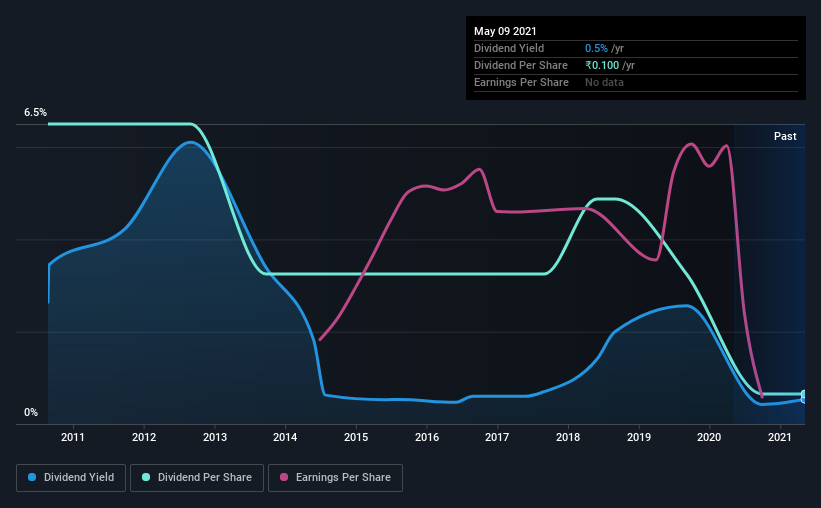

A 0.5% yield is nothing to get excited about, but investors probably think the long payment history suggests Patel Integrated Logistics has some staying power. Remember that the recent share price drop will make Patel Integrated Logistics's yield look higher, even though recent events might have impacted the company's prospects. There are a few simple ways to reduce the risks of buying Patel Integrated Logistics for its dividend, and we'll go through these below.

Explore this interactive chart for our latest analysis on Patel Integrated Logistics!

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Patel Integrated Logistics paid out 16% of its profit as dividends, over the trailing twelve month period. Given the low payout ratio, it is hard to envision the dividend coming under threat, barring a catastrophe.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. Patel Integrated Logistics paid out 93% of its free cash flow last year, which we think is concerning if cash flows do not improve. While Patel Integrated Logistics' dividends were covered by the company's reported profits, free cash flow is somewhat more important, so it's not great to see that the company didn't generate enough cash to pay its dividend. Were it to repeatedly pay dividends that were not well covered by cash flow, this could be a risk to Patel Integrated Logistics' ability to maintain its dividend.

Consider getting our latest analysis on Patel Integrated Logistics' financial position here.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. For the purpose of this article, we only scrutinise the last decade of Patel Integrated Logistics' dividend payments. Its dividend payments have declined on at least one occasion over the past 10 years. During the past 10-year period, the first annual payment was ₹1.0 in 2011, compared to ₹0.1 last year. This works out to a decline of approximately 90% over that time.

We struggle to make a case for buying Patel Integrated Logistics for its dividend, given that payments have shrunk over the past 10 years.

Dividend Growth Potential

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Over the past five years, it looks as though Patel Integrated Logistics' EPS have declined at around 35% a year. A sharp decline in earnings per share is not great from from a dividend perspective, as even conservative payout ratios can come under pressure if earnings fall far enough.

Conclusion

To summarise, shareholders should always check that Patel Integrated Logistics' dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. First, we like Patel Integrated Logistics' low dividend payout ratio, although we're a bit concerned that it paid out a substantially higher percentage of its free cash flow. Earnings per share have been falling, and the company has cut its dividend at least once in the past. From a dividend perspective, this is a cause for concern. In summary, Patel Integrated Logistics has a number of shortcomings that we'd find it hard to get past. Things could change, but we think there are a number of better ideas out there.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Just as an example, we've come accross 8 warning signs for Patel Integrated Logistics you should be aware of, and 4 of them can't be ignored.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

When trading Patel Integrated Logistics or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:PATINTLOG

Flawless balance sheet moderate.