- India

- /

- Marine and Shipping

- /

- NSEI:ARVINDPORT

Arvind and Company Shipping Agencies Limited (NSE:ACSAL) Stock Rockets 26% But Many Are Still Ignoring The Company

Despite an already strong run, Arvind and Company Shipping Agencies Limited (NSE:ACSAL) shares have been powering on, with a gain of 26% in the last thirty days. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

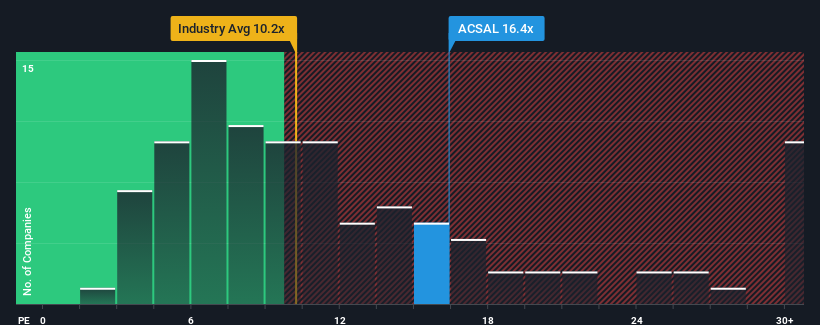

Even after such a large jump in price, Arvind and Company Shipping Agencies' price-to-earnings (or "P/E") ratio of 16.4x might still make it look like a strong buy right now compared to the market in India, where around half of the companies have P/E ratios above 35x and even P/E's above 64x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Earnings have risen firmly for Arvind and Company Shipping Agencies recently, which is pleasing to see. It might be that many expect the respectable earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Arvind and Company Shipping Agencies

Does Growth Match The Low P/E?

Arvind and Company Shipping Agencies' P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

If we review the last year of earnings growth, the company posted a worthy increase of 10%. This was backed up an excellent period prior to see EPS up by 1,272% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Comparing that to the market, which is only predicted to deliver 25% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we find it odd that Arvind and Company Shipping Agencies is trading at a P/E lower than the market. It looks like most investors are not convinced the company can maintain its recent growth rates.

The Key Takeaway

Even after such a strong price move, Arvind and Company Shipping Agencies' P/E still trails the rest of the market significantly. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Arvind and Company Shipping Agencies currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

You need to take note of risks, for example - Arvind and Company Shipping Agencies has 4 warning signs (and 1 which is a bit concerning) we think you should know about.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ARVINDPORT

Arvind Port and Infra

Arvind Port and Infra Limited charters barges and hotel and hospitality businesses in India.

Proven track record with adequate balance sheet.

Market Insights

Community Narratives