- India

- /

- Communications

- /

- NSEI:ASTRAMICRO

Astra Microwave Products (NSE:ASTRAMICRO) Has A Somewhat Strained Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Astra Microwave Products Limited (NSE:ASTRAMICRO) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Astra Microwave Products

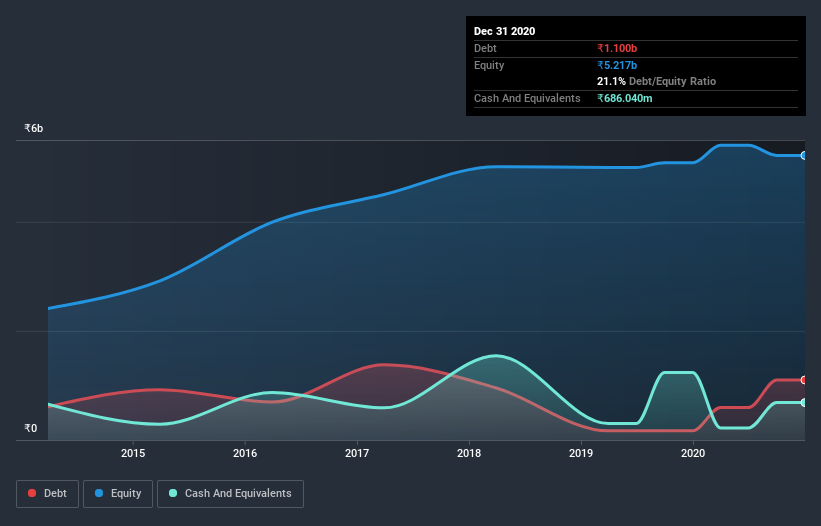

How Much Debt Does Astra Microwave Products Carry?

As you can see below, at the end of September 2020, Astra Microwave Products had ₹1.10b of debt, up from ₹171.1m a year ago. Click the image for more detail. However, because it has a cash reserve of ₹686.0m, its net debt is less, at about ₹414.4m.

A Look At Astra Microwave Products' Liabilities

The latest balance sheet data shows that Astra Microwave Products had liabilities of ₹3.77b due within a year, and liabilities of ₹22.9m falling due after that. On the other hand, it had cash of ₹686.0m and ₹2.01b worth of receivables due within a year. So it has liabilities totalling ₹1.10b more than its cash and near-term receivables, combined.

Given Astra Microwave Products has a market capitalization of ₹11.4b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Given net debt is only 0.95 times EBITDA, it is initially surprising to see that Astra Microwave Products's EBIT has low interest coverage of 1.9 times. So while we're not necessarily alarmed we think that its debt is far from trivial. Shareholders should be aware that Astra Microwave Products's EBIT was down 72% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Astra Microwave Products will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Astra Microwave Products saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Astra Microwave Products's conversion of EBIT to free cash flow and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But on the bright side, its net debt to EBITDA is a good sign, and makes us more optimistic. Overall, we think it's fair to say that Astra Microwave Products has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 5 warning signs we've spotted with Astra Microwave Products (including 1 which is a bit concerning) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Astra Microwave Products, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:ASTRAMICRO

Astra Microwave Products

Designs, develops, manufactures, and sells sub-systems for radio frequency and microwave systems used in defense, space, meteorology, civil, and telecommunication applications in India.

Reasonable growth potential with proven track record.