Advertisement

Zensar Technologies Limited Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

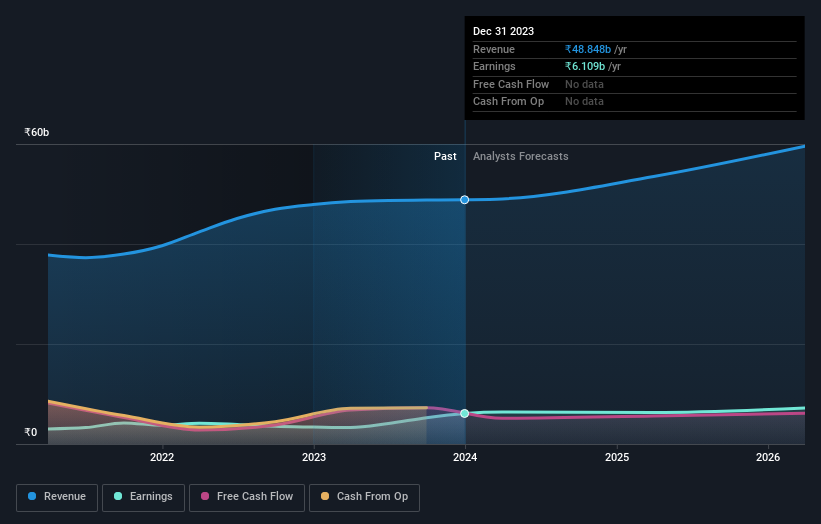

Zensar Technologies Limited (NSE:ZENSARTECH) last week reported its latest third-quarter results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. It looks like a credible result overall - although revenues of ₹12b were what the analysts expected, Zensar Technologies surprised by delivering a (statutory) profit of ₹7.08 per share, an impressive 21% above what was forecast. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Zensar Technologies

Taking into account the latest results, the consensus forecast from Zensar Technologies' eight analysts is for revenues of ₹53.5b in 2025. This reflects a notable 9.5% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to rise 3.3% to ₹27.85. In the lead-up to this report, the analysts had been modelling revenues of ₹53.9b and earnings per share (EPS) of ₹27.74 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

The analysts reconfirmed their price target of ₹623, showing that the business is executing well and in line with expectations. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Zensar Technologies at ₹680 per share, while the most bearish prices it at ₹570. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's clear from the latest estimates that Zensar Technologies' rate of growth is expected to accelerate meaningfully, with the forecast 7.5% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 4.6% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 8.5% annually. Zensar Technologies is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no real changes to revenue forecasts, with the business still expected to grow in line with the overall industry. The consensus price target held steady at ₹623, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple Zensar Technologies analysts - going out to 2026, and you can see them free on our platform here.

You can also see our analysis of Zensar Technologies' Board and CEO remuneration and experience, and whether company insiders have been buying stock.

Valuation is complex, but we're here to simplify it.

Discover if Zensar Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ZENSARTECH

Zensar Technologies

A digital solutions and technology services company, provides technology consulting and system integration services in India, Americas, Europe, Africa, and internationally.

Flawless balance sheet 6 star dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative