Advertisement

Quicktouch Technologies (NSE:QUICKTOUCH) First Quarter 2025 Results

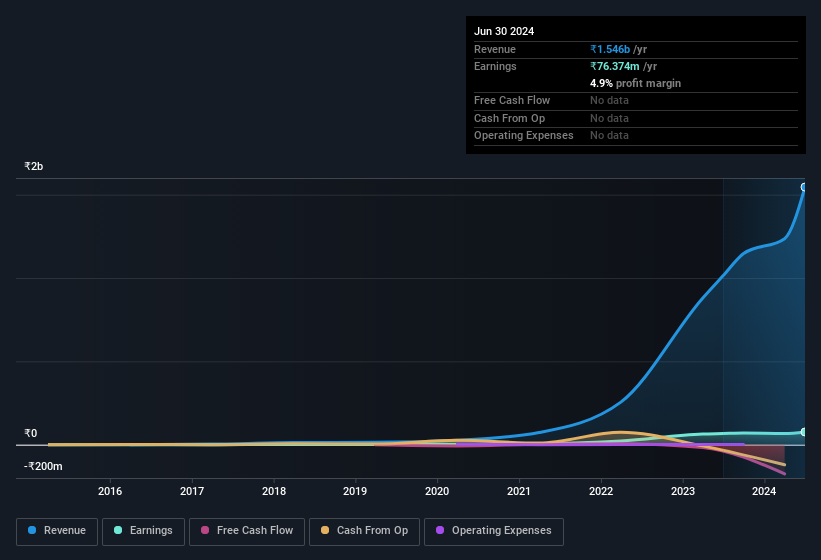

Key Financial Results

- Revenue: ₹424.1m (up 81% from 1Q 2024).

- Net income: ₹15.3m (down 10% from 1Q 2024).

- Profit margin: 3.6% (down from 7.3% in 1Q 2024). The decrease in margin was driven by higher expenses.

- EPS: ₹2.61.

All figures shown in the chart above are for the trailing 12 month (TTM) period

Quicktouch Technologies shares are up 5.0% from a week ago.

Risk Analysis

It's necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Quicktouch Technologies (at least 1 which shouldn't be ignored), and understanding these should be part of your investment process.

Valuation is complex, but we're here to simplify it.

Discover if Quicktouch Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:QUICKTOUCH

Quicktouch Technologies

Engages in the development and trading of computer software and related activities primarily in India.

Excellent balance sheet with moderate risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

AN

andre_santos on Ferrari ·

Ferrari's Intrinsic and Historical Valuation

Fair Value:€243.5623.2% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TI

TibiT on Costco Wholesale ·

Investment Thesis: Costco Wholesale (COST)

Fair Value:US$726.2932.7% overvalued

18 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3323.3% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on Broadcom ·

Broadcom - A Fundamental and Historical Valuation

Fair Value:US$258.7135.9% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DE

Deep_Insights on Hims & Hers Health ·

Hims & Hers Health aims for three dimensional revenue expansion

Fair Value:US$173.0281.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DM

DMXS on Coca-Cola HBC ·

A Tale of Two Engines: Coca-Cola HBC (EEE.AT)

Fair Value:€54.617.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8230.6% undervalued

78 followersusers have followed this narrative

6 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.4% undervalued

1029 followersusers have followed this narrative

6 commentsusers have commented on this narrative

30 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6444.1% undervalued

45 followersusers have followed this narrative

5 commentsusers have commented on this narrative

9 likesusers have liked this narrative