Advertisement

Analysts Have Been Trimming Their Persistent Systems Limited (NSE:PERSISTENT) Price Target After Its Latest Report

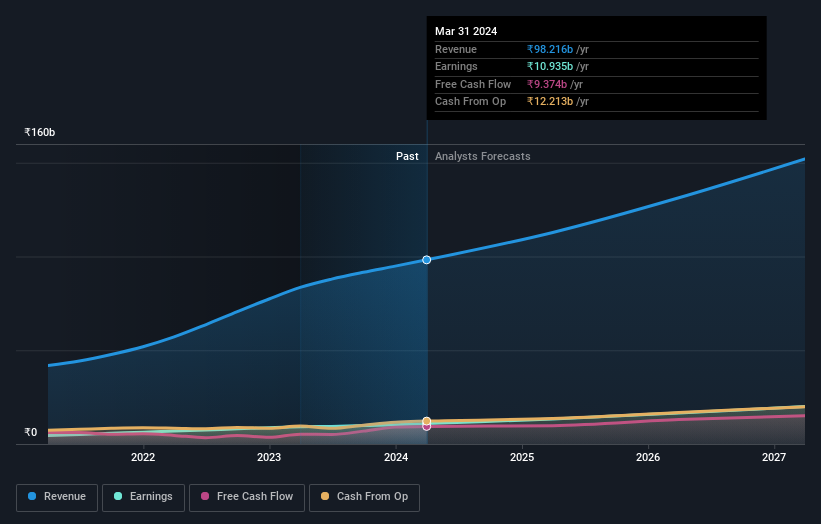

It's been a sad week for Persistent Systems Limited (NSE:PERSISTENT), who've watched their investment drop 11% to ₹3,430 in the week since the company reported its yearly result. It was a credible result overall, with revenues of ₹98b and statutory earnings per share of ₹71.07 both in line with analyst estimates, showing that Persistent Systems is executing in line with expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Persistent Systems

Taking into account the latest results, the consensus forecast from Persistent Systems' 30 analysts is for revenues of ₹112.8b in 2025. This reflects a decent 15% improvement in revenue compared to the last 12 months. Per-share earnings are expected to step up 17% to ₹86.77. Before this earnings report, the analysts had been forecasting revenues of ₹113.7b and earnings per share (EPS) of ₹91.81 in 2025. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

It might be a surprise to learn that the consensus price target fell 5.5% to ₹3,691, with the analysts clearly linking lower forecast earnings to the performance of the stock price. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Persistent Systems analyst has a price target of ₹4,938 per share, while the most pessimistic values it at ₹1,675. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Persistent Systems' past performance and to peers in the same industry. We would highlight that Persistent Systems' revenue growth is expected to slow, with the forecast 15% annualised growth rate until the end of 2025 being well below the historical 25% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 7.7% annually. So it's pretty clear that, while Persistent Systems' revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Persistent Systems' future valuation.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple Persistent Systems analysts - going out to 2027, and you can see them free on our platform here.

We also provide an overview of the Persistent Systems Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PERSISTENT

Persistent Systems

Provides software products, services, and technology solutions in India, North America, and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

23 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Microsoft ·

Microsoft no es una apuesta. Es una franquicia global de la que se puede ser socio durante décadas.

Fair Value:US$497.815.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Significant headwinds will temper expectations for FY2027

Fair Value:JP¥1.91k8.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on International Business Machines ·

IBM has transitioned from a traditional IT services provider into a hybrid cloud and AI platform leader

Fair Value:US$256.0812.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1191 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative