Advertisement

There are a few key trends to look for if we want to identify the next multi-bagger. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So when we looked at the ROCE trend of Intense Technologies (NSE:INTENTECH) we really liked what we saw.

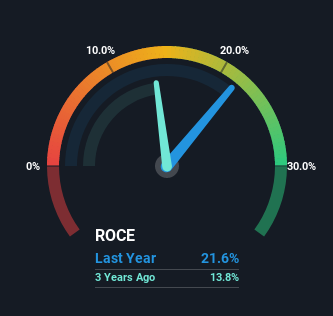

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Intense Technologies is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.22 = ₹232m ÷ (₹1.1b - ₹51m) (Based on the trailing twelve months to December 2022).

So, Intense Technologies has an ROCE of 22%. In absolute terms that's a great return and it's even better than the Software industry average of 13%.

Check out our latest analysis for Intense Technologies

Historical performance is a great place to start when researching a stock so above you can see the gauge for Intense Technologies' ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Intense Technologies, check out these free graphs here.

SWOT Analysis for Intense Technologies

Strength

- Debt is well covered by earnings.

Weakness

- Earnings declined over the past year.

- Dividend is low compared to the top 25% of dividend payers in the Software market.

- Current share price is above our estimate of fair value.

- Shareholders have been diluted in the past year.

Opportunity

- INTENTECH's financial characteristics indicate limited near-term opportunities for shareholders.

- Lack of analyst coverage makes it difficult to determine INTENTECH's earnings prospects.

Threat

- Debt is not well covered by operating cash flow.

- Paying a dividend but company has no free cash flows.

What The Trend Of ROCE Can Tell Us

The trends we've noticed at Intense Technologies are quite reassuring. The data shows that returns on capital have increased substantially over the last five years to 22%. The amount of capital employed has increased too, by 145%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

One more thing to note, Intense Technologies has decreased current liabilities to 4.6% of total assets over this period, which effectively reduces the amount of funding from suppliers or short-term creditors. So shareholders would be pleased that the growth in returns has mostly come from underlying business performance.

The Key Takeaway

To sum it up, Intense Technologies has proven it can reinvest in the business and generate higher returns on that capital employed, which is terrific. Since the total return from the stock has been almost flat over the last five years, there might be an opportunity here if the valuation looks good. So researching this company further and determining whether or not these trends will continue seems justified.

On a final note, we've found 3 warning signs for Intense Technologies that we think you should be aware of.

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INTENTECH

Intense Technologies

Provides enterprise platform and IP-enabled service organization services in India.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.2% undervalued

95 followersusers have followed this narrative

0 commentsusers have commented on this narrative

23 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.5% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.3% overvalued

37 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Revival Gold ·

7,000% US Based Idaho & Utah Gold Miner Play, Beartrack + Mercur: $1.2B+ NAV Leverage with Strong Management

Fair Value:CA$12.7194.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

NO

NordicWolf on Carlsberg ·

Defensive Beverage Compounder With Britvic Upside

Fair Value:DKK 870.329.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

DaneDruss on Cloudflare ·

Q-Day: Quantum Hype vs Quantum-Safe Infrastructure

Fair Value:US$167.4547.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.9% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5453.8% undervalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

MW

mwod31 on Greatland Resources ·

A great comment, WSB have not done the research imo. I intend to buy more shares in 2026.

0

|0