Should Income Investors Look At Dev Information Technology Limited (NSE:DEVIT) Before Its Ex-Dividend?

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Dev Information Technology Limited (NSE:DEVIT) is about to trade ex-dividend in the next 3 days. This means that investors who purchase shares on or after the 20th of September will not receive the dividend, which will be paid on the 30th of October.

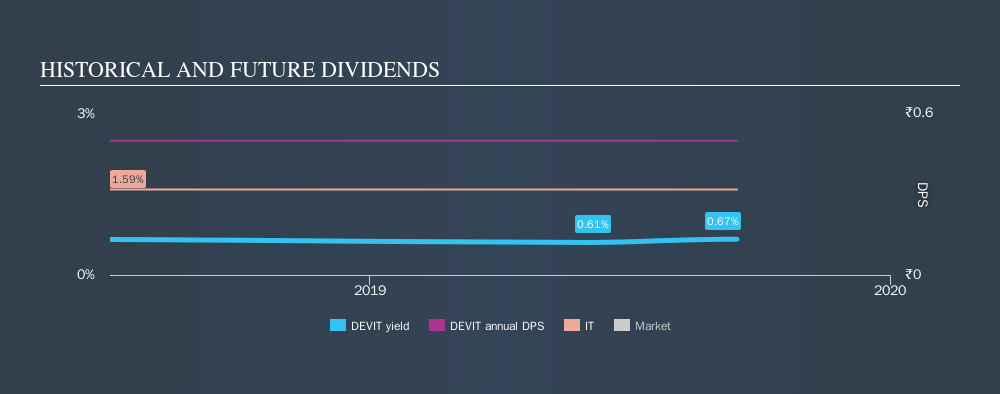

Dev Information Technology's next dividend payment will be ₹0.50 per share. Last year, in total, the company distributed ₹0.50 to shareholders. Last year's total dividend payments show that Dev Information Technology has a trailing yield of 0.7% on the current share price of ₹75. If you buy this business for its dividend, you should have an idea of whether Dev Information Technology's dividend is reliable and sustainable. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

View our latest analysis for Dev Information Technology

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Dev Information Technology is paying out just 6.3% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Dev Information Technology paid a dividend despite reporting negative free cash flow over the last twelve months. This may be due to heavy investment in the business, but this is still suboptimal from a dividend sustainability perspective.

It's positive to see that Dev Information Technology's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit Dev Information Technology paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Fortunately for readers, Dev Information Technology's earnings per share have been growing at 15% a year for the past five years.

We'd also point out that Dev Information Technology issued a meaningful number of new shares in the past year. It's hard to grow dividends per share when a company keeps creating new shares.

Unfortunately Dev Information Technology has only been paying a dividend for a year or so, so there's not much of a history to draw insight from.

The Bottom Line

Is Dev Information Technology an attractive dividend stock, or better left on the shelf? We like that Dev Information Technology has been successfully growing its earnings per share at a nice rate and reinvesting most of its profits in the business. However, we note the high cashflow payout ratio with some concern. It might be worth researching if the company is reinvesting in growth projects that could grow earnings and dividends in the future, but for now we're not all that optimistic on its dividend prospects.

Want to learn more about Dev Information Technology? Here's a visualisation of its historical rate of revenue and earnings growth.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:DEVIT

Dev Information Technology

Provides information technology enabled services in India, Europe, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)