Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Premier Energies Limited (NSE:PREMIERENE) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

What Is Premier Energies's Debt?

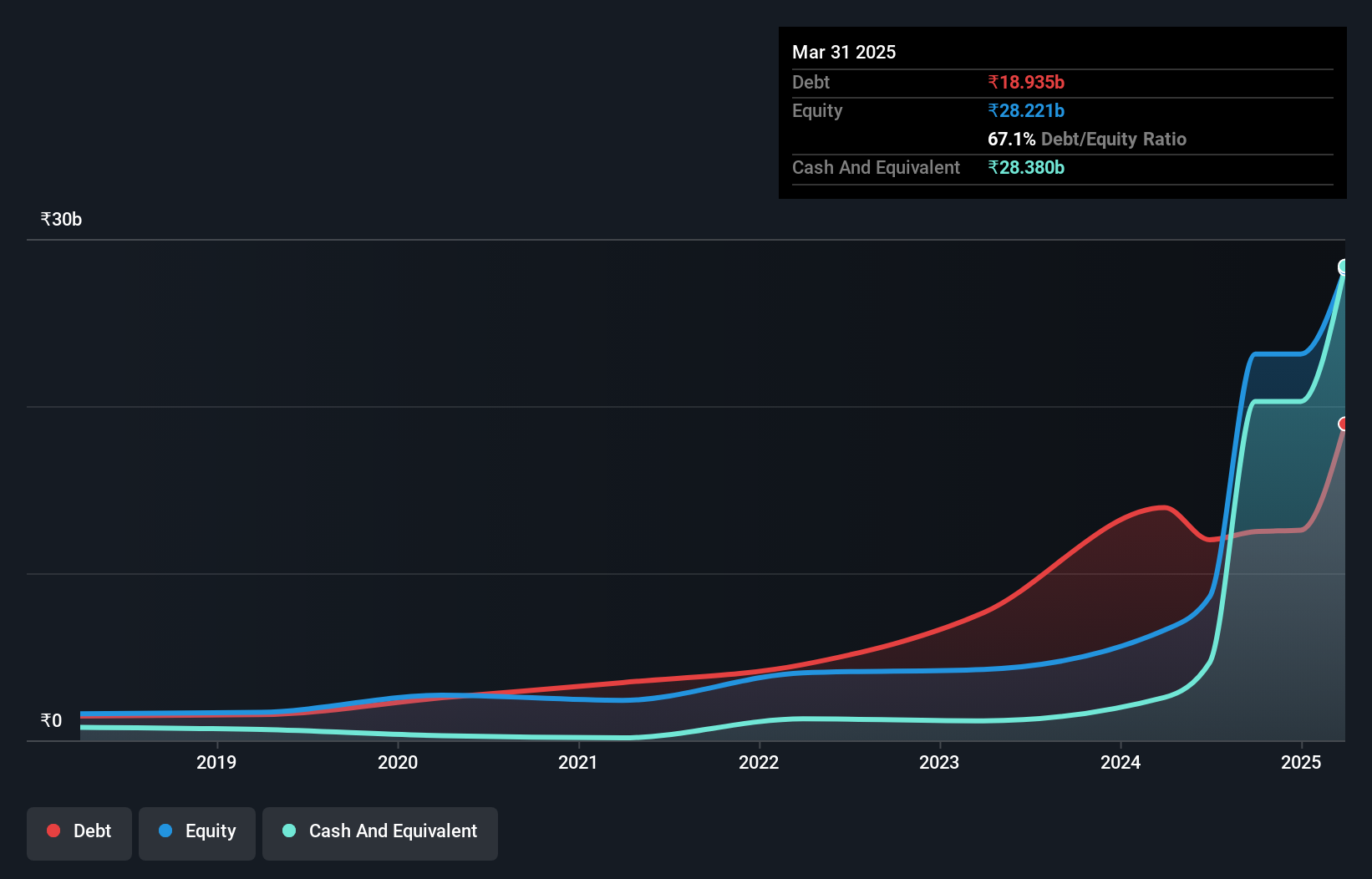

As you can see below, at the end of March 2025, Premier Energies had ₹18.9b of debt, up from ₹13.9b a year ago. Click the image for more detail. However, it does have ₹28.4b in cash offsetting this, leading to net cash of ₹9.45b.

A Look At Premier Energies' Liabilities

Zooming in on the latest balance sheet data, we can see that Premier Energies had liabilities of ₹27.8b due within 12 months and liabilities of ₹12.4b due beyond that. Offsetting these obligations, it had cash of ₹28.4b as well as receivables valued at ₹8.03b due within 12 months. So its liabilities total ₹3.78b more than the combination of its cash and short-term receivables.

Having regard to Premier Energies' size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the ₹461.7b company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, Premier Energies also has more cash than debt, so we're pretty confident it can manage its debt safely.

View our latest analysis for Premier Energies

Better yet, Premier Energies grew its EBIT by 225% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Premier Energies can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Premier Energies may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Premier Energies created free cash flow amounting to 7.4% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing Up

We could understand if investors are concerned about Premier Energies's liabilities, but we can be reassured by the fact it has has net cash of ₹9.45b. And it impressed us with its EBIT growth of 225% over the last year. So we don't have any problem with Premier Energies's use of debt. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Premier Energies insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PREMIERENE

Premier Energies

Manufactures and sells integrated solar cells and modules in India.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Airbnb (ABNB): Still one of the most interesting bets in travel

Fair Value US$163.75|23.6% undervalued

TI

Community Contributor

ING leads the pack when it comes to pivoting towards non-lending income

Fair Value €27.92|23.7% undervalued

PI

Community Contributor

Coles (ASX: COL): Safe, Steady, and Surprisingly Cheap

Fair Value AU$22.00|4.3% undervalued

RO

Community Contributor