Advertisement

- India

- /

- Specialty Stores

- /

- NSEI:PNGJL

We Think N Gadgil Jewellers (NSE:PNGJL) Can Stay On Top Of Its Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that P N Gadgil Jewellers Limited (NSE:PNGJL) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is N Gadgil Jewellers's Debt?

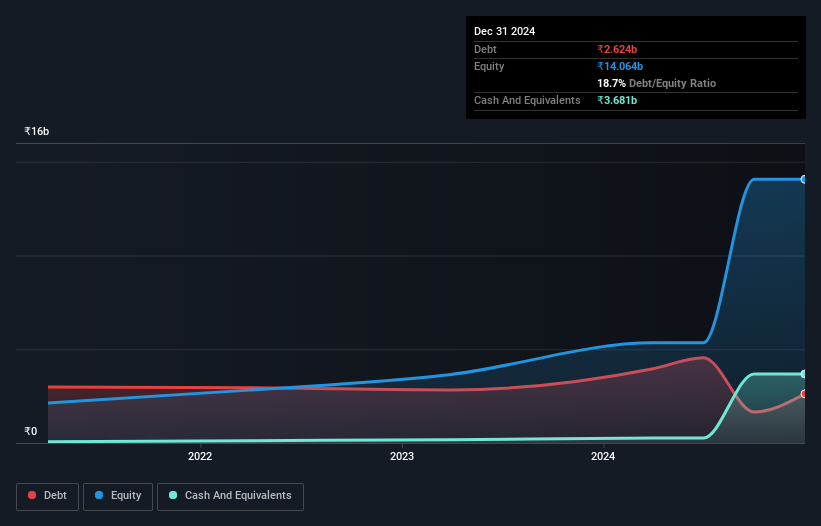

As you can see below, N Gadgil Jewellers had ₹2.62b of debt at September 2024, down from ₹3.96b a year prior. But on the other hand it also has ₹3.68b in cash, leading to a ₹1.06b net cash position.

How Healthy Is N Gadgil Jewellers' Balance Sheet?

According to the last reported balance sheet, N Gadgil Jewellers had liabilities of ₹9.90b due within 12 months, and liabilities of ₹983.5m due beyond 12 months. On the other hand, it had cash of ₹3.68b and ₹357.2m worth of receivables due within a year. So its liabilities total ₹6.85b more than the combination of its cash and short-term receivables.

Of course, N Gadgil Jewellers has a market capitalization of ₹74.6b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, N Gadgil Jewellers also has more cash than debt, so we're pretty confident it can manage its debt safely.

View our latest analysis for N Gadgil Jewellers

In addition to that, we're happy to report that N Gadgil Jewellers has boosted its EBIT by 35%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if N Gadgil Jewellers can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While N Gadgil Jewellers has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, N Gadgil Jewellers burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing Up

While it is always sensible to look at a company's total liabilities, it is very reassuring that N Gadgil Jewellers has ₹1.06b in net cash. And we liked the look of last year's 35% year-on-year EBIT growth. So we are not troubled with N Gadgil Jewellers's debt use. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of N Gadgil Jewellers's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if N Gadgil Jewellers might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PNGJL

High growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|90.8% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|15.9% undervalued

MA

Community Contributor