Advertisement

IntraSoft Technologies Limited (NSE:ISFT) Not Doing Enough For Some Investors As Its Shares Slump 25%

IntraSoft Technologies Limited (NSE:ISFT) shares have had a horrible month, losing 25% after a relatively good period beforehand. Looking back over the past twelve months the stock has been a solid performer regardless, with a gain of 16%.

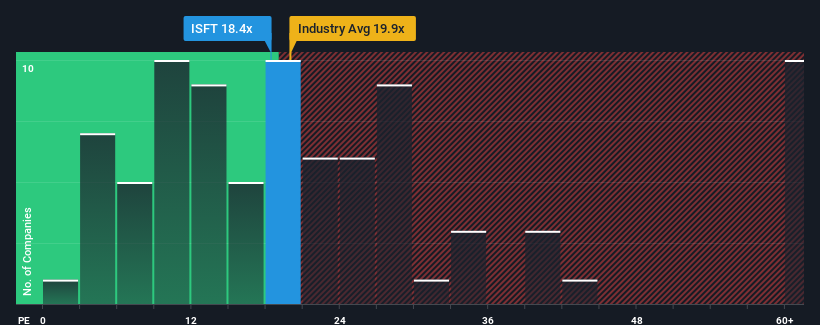

Since its price has dipped substantially, IntraSoft Technologies may be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 18.4x, since almost half of all companies in India have P/E ratios greater than 29x and even P/E's higher than 54x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

IntraSoft Technologies has been doing a good job lately as it's been growing earnings at a solid pace. It might be that many expect the respectable earnings performance to degrade substantially, which has repressed the P/E. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

View our latest analysis for IntraSoft Technologies

Does Growth Match The Low P/E?

In order to justify its P/E ratio, IntraSoft Technologies would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered an exceptional 17% gain to the company's bottom line. Pleasingly, EPS has also lifted 49% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 24% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we can see why IntraSoft Technologies is trading at a P/E lower than the market. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

What We Can Learn From IntraSoft Technologies' P/E?

IntraSoft Technologies' recently weak share price has pulled its P/E below most other companies. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of IntraSoft Technologies revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Plus, you should also learn about these 3 warning signs we've spotted with IntraSoft Technologies (including 1 which can't be ignored).

If these risks are making you reconsider your opinion on IntraSoft Technologies, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ISFT

IntraSoft Technologies

Through its subsidiaries, engages in the development and delivery of e-commerce and e-cards through internet platform in India and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor