- India

- /

- Real Estate

- /

- NSEI:PURVA

Further Upside For Puravankara Limited (NSE:PURVA) Shares Could Introduce Price Risks After 34% Bounce

Puravankara Limited (NSE:PURVA) shares have continued their recent momentum with a 34% gain in the last month alone. The last month tops off a massive increase of 137% in the last year.

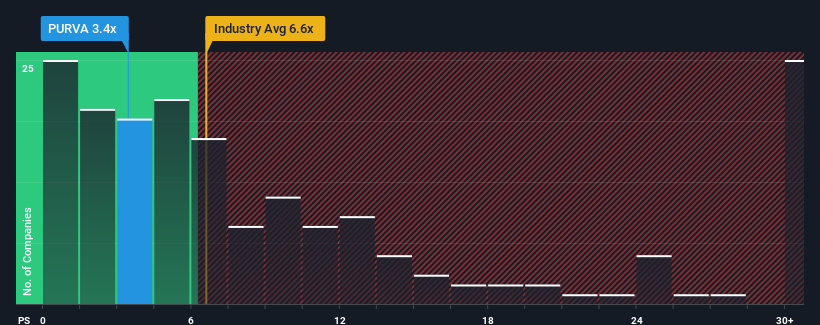

Although its price has surged higher, Puravankara may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 3.4x, considering almost half of all companies in the Real Estate industry in India have P/S ratios greater than 6.6x and even P/S higher than 15x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Puravankara

What Does Puravankara's Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Puravankara has been relatively sluggish. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Puravankara will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The Low P/S?

Puravankara's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 45%. The latest three year period has also seen a 17% overall rise in revenue, aided extensively by its short-term performance. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 37% over the next year. With the industry predicted to deliver 36% growth , the company is positioned for a comparable revenue result.

With this information, we find it odd that Puravankara is trading at a P/S lower than the industry. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

What We Can Learn From Puravankara's P/S?

Despite Puravankara's share price climbing recently, its P/S still lags most other companies. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've seen that Puravankara currently trades on a lower than expected P/S since its forecast growth is in line with the wider industry. When we see middle-of-the-road revenue growth like this, we assume it must be the potential risks that are what is placing pressure on the P/S ratio. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Having said that, be aware Puravankara is showing 4 warning signs in our investment analysis, and 2 of those are potentially serious.

If these risks are making you reconsider your opinion on Puravankara, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PURVA

Puravankara

Designs, develops, constructs, and markets residential and commercial properties in India.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Community Narratives