Advertisement

- India

- /

- Life Sciences

- /

- NSEI:TARSONS

3 Indian Stocks That Could Be Trading Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

Over the last 7 days, the Indian market has experienced a decline of 3.6%, yet it has shown impressive growth of 40% over the past year, with earnings projected to increase by 17% annually in the coming years. In this environment, identifying stocks that are potentially trading below their estimated value can be crucial for investors seeking opportunities amidst fluctuating market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In India

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Everest Kanto Cylinder (NSEI:EKC) | ₹188.79 | ₹306.16 | 38.3% |

| RITES (NSEI:RITES) | ₹295.85 | ₹517.78 | 42.9% |

| Thomas Cook (India) (BSE:500413) | ₹186.30 | ₹301.15 | 38.1% |

| IOL Chemicals and Pharmaceuticals (BSE:524164) | ₹431.70 | ₹762.32 | 43.4% |

| Orchid Pharma (NSEI:ORCHPHARMA) | ₹1257.70 | ₹2142.32 | 41.3% |

| Vedanta (NSEI:VEDL) | ₹500.30 | ₹900.84 | 44.5% |

| Patel Engineering (BSE:531120) | ₹52.93 | ₹91.66 | 42.3% |

| Artemis Medicare Services (NSEI:ARTEMISMED) | ₹253.90 | ₹445.15 | 43% |

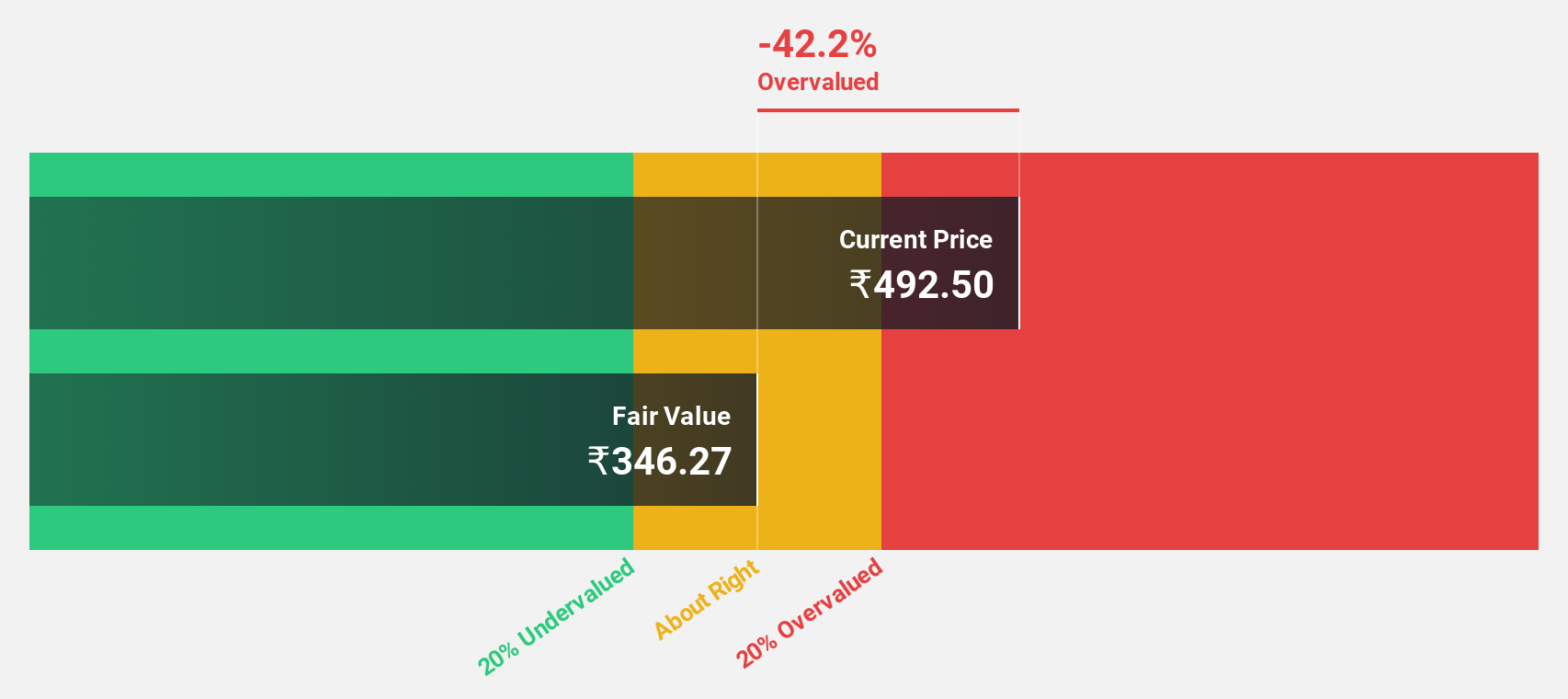

| Tarsons Products (NSEI:TARSONS) | ₹429.95 | ₹708.02 | 39.3% |

| Strides Pharma Science (NSEI:STAR) | ₹1410.20 | ₹2704.30 | 47.9% |

Let's explore several standout options from the results in the screener.

Awfis Space Solutions (NSEI:AWFIS)

Overview: Awfis Space Solutions Limited offers flexible workspace solutions in India and has a market cap of ₹44.50 billion.

Operations: The company's revenue primarily comes from Co-Working Space on Rent and Allied Services, generating ₹6.65 billion, followed by Construction and Fit-Out Projects at ₹2.29 billion.

Estimated Discount To Fair Value: 27.4%

Awfis Space Solutions is trading at ₹633.8, significantly below its estimated fair value of ₹873.58, suggesting undervaluation based on discounted cash flow analysis. The company anticipates above-market revenue growth of 28.8% annually and aims to become profitable within three years, despite recent share price volatility. Recent expansions in GIFT City and partnerships in Pune enhance its strategic presence in India's commercial hubs, potentially boosting future cash flows and supporting its undervalued status.

- Our comprehensive growth report raises the possibility that Awfis Space Solutions is poised for substantial financial growth.

- Dive into the specifics of Awfis Space Solutions here with our thorough financial health report.

Quess (NSEI:QUESS)

Overview: Quess Corp Limited is a business services provider operating in India, South East Asia, the Middle East, and North America with a market cap of ₹108.91 billion.

Operations: The company's revenue is derived from several segments: Product Led Business contributing ₹4.29 billion, Workforce Management at ₹138.44 billion, Operating Asset Management generating ₹28.43 billion, and Global Technology Solutions (excluding Product Led Business) adding ₹23.87 billion.

Estimated Discount To Fair Value: 31.4%

Quess Corp is notably undervalued, trading at ₹732.8 compared to its estimated fair value of ₹1067.53, based on discounted cash flow analysis. The company reported a robust 62.5% earnings growth over the past year and expects annual profit growth of 22.8%, outpacing the Indian market's average forecasted growth of 17.2%. However, despite strong earnings potential, Quess has an unstable dividend track record and low forecasted return on equity at 19.5%.

- In light of our recent growth report, it seems possible that Quess' financial performance will exceed current levels.

- Navigate through the intricacies of Quess with our comprehensive financial health report here.

Tarsons Products (NSEI:TARSONS)

Overview: Tarsons Products Limited manufactures and trades scientific plastic labware products in India and internationally, with a market cap of ₹22.88 billion.

Operations: The company's revenue segment comprises Plastic Laboratory Products and Certain Scientific Instruments, generating ₹3.19 billion.

Estimated Discount To Fair Value: 39.3%

Tarsons Products appears undervalued, trading at ₹429.95 against an estimated fair value of ₹708.02, reflecting a 39.3% discount based on discounted cash flow analysis. Despite high debt levels and declining profit margins from 25.3% to 11.6%, earnings are expected to grow significantly at 27.45% annually over the next three years, surpassing the Indian market's growth rate of 17.2%. However, its dividend yield remains unsustainable due to insufficient free cash flows.

- The growth report we've compiled suggests that Tarsons Products' future prospects could be on the up.

- Delve into the full analysis health report here for a deeper understanding of Tarsons Products.

Where To Now?

- Delve into our full catalog of 27 Undervalued Indian Stocks Based On Cash Flows here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tarsons Products might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:TARSONS

Tarsons Products

Manufactures and trades in scientific plastic labware products in India and internationally.

Reasonable growth potential with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets