Shilpa Medicare Limited's (NSE:SHILPAMED) investors are due to receive a payment of ₹1.10 per share on 28th of October. The dividend yield is 0.3% based on this payment, which is a little bit low compared to the other companies in the industry.

Check out our latest analysis for Shilpa Medicare

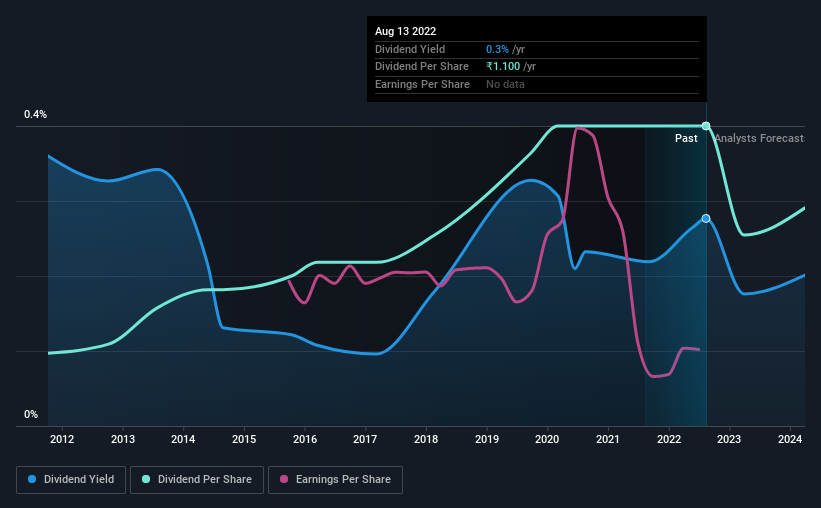

Shilpa Medicare's Dividend Is Well Covered By Earnings

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. Prior to this announcement, Shilpa Medicare's earnings easily covered the dividend, but free cash flows were negative. With the company not bringing in any cash, paying out to shareholders is bound to become difficult at some point.

The next year is set to see EPS grow by 39.3%. Assuming the dividend continues along recent trends, we think the payout ratio could be 12% by next year, which is in a pretty sustainable range.

Shilpa Medicare Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. The dividend has gone from an annual total of ₹0.267 in 2012 to the most recent total annual payment of ₹1.10. This implies that the company grew its distributions at a yearly rate of about 15% over that duration. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

Dividend Growth Potential Is Shaky

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Unfortunately things aren't as good as they seem. Shilpa Medicare's earnings per share has shrunk at 14% a year over the past five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

Our Thoughts On Shilpa Medicare's Dividend

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for Shilpa Medicare that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SHILPAMED

Shilpa Medicare

Manufactures and sells active pharmaceutical ingredients (APIs), finished dosage formulations, biosimilars, recombinant albumin in India, the United States, Europe, and internationally.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives