Advertisement

- India

- /

- Life Sciences

- /

- NSEI:DCAL

These 4 Measures Indicate That Dishman Carbogen Amcis (NSE:DCAL) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Dishman Carbogen Amcis Limited (NSE:DCAL) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Dishman Carbogen Amcis

What Is Dishman Carbogen Amcis's Net Debt?

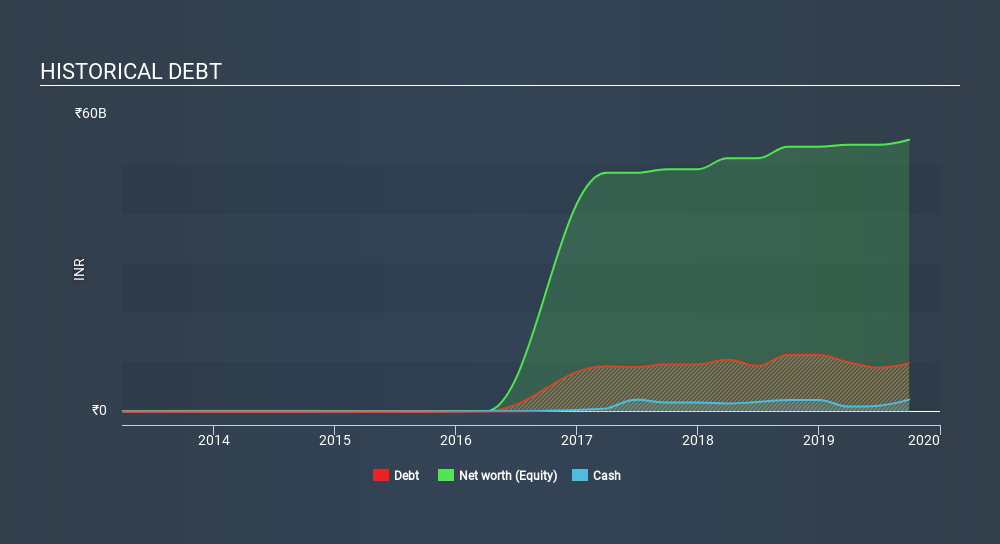

You can click the graphic below for the historical numbers, but it shows that Dishman Carbogen Amcis had ₹9.71b of debt in September 2019, down from ₹11.4b, one year before. However, it does have ₹2.37b in cash offsetting this, leading to net debt of about ₹7.33b.

How Strong Is Dishman Carbogen Amcis's Balance Sheet?

The latest balance sheet data shows that Dishman Carbogen Amcis had liabilities of ₹14.1b due within a year, and liabilities of ₹8.88b falling due after that. Offsetting this, it had ₹2.37b in cash and ₹4.44b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹16.1b.

This is a mountain of leverage relative to its market capitalization of ₹20.0b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Dishman Carbogen Amcis's net debt is only 1.1 times its EBITDA. And its EBIT covers its interest expense a whopping 13.0 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Also positive, Dishman Carbogen Amcis grew its EBIT by 27% in the last year, and that should make it easier to pay down debt, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Dishman Carbogen Amcis's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Dishman Carbogen Amcis reported free cash flow worth 4.9% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Dishman Carbogen Amcis's interest cover was a real positive on this analysis, as was its EBIT growth rate. But truth be told its conversion of EBIT to free cash flow had us nibbling our nails. Looking at all this data makes us feel a little cautious about Dishman Carbogen Amcis's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Dishman Carbogen Amcis's earnings per share history for free.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:DCAL

Dishman Carbogen Amcis

Provides contract research and manufacturing services for the pharmaceutical and healthcare industries worldwide.

Questionable track record with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|12.0% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor