Advertisement

Here's Why Shareholders May Want To Be Cautious With Increasing Worth Peripherals Limited's (NSE:WORTH) CEO Pay Packet

Key Insights

- Worth Peripherals' Annual General Meeting to take place on 16th of August

- CEO Raminder Chadha's total compensation includes salary of ₹5.10m

- The total compensation is 34% higher than the average for the industry

- Worth Peripherals' EPS grew by 2.2% over the past three years while total shareholder return over the past three years was 31%

Under the guidance of CEO Raminder Chadha, Worth Peripherals Limited (NSE:WORTH) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 16th of August. However, some shareholders may still want to keep CEO compensation within reason.

See our latest analysis for Worth Peripherals

How Does Total Compensation For Raminder Chadha Compare With Other Companies In The Industry?

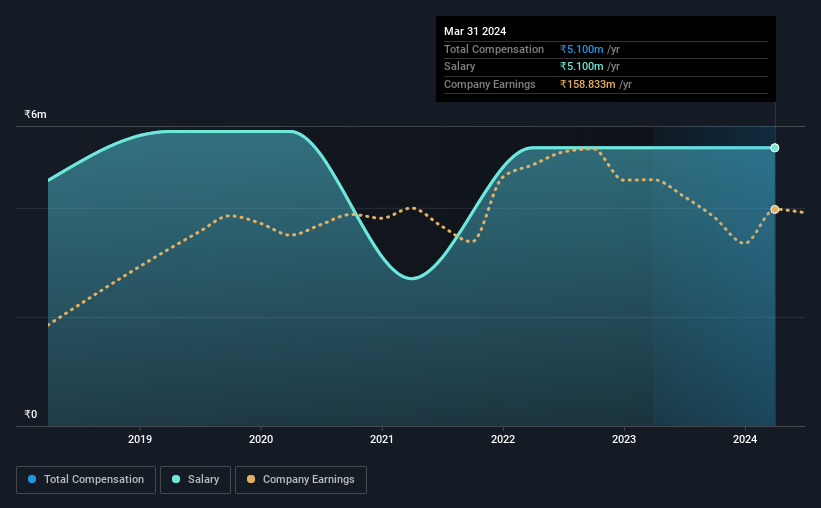

According to our data, Worth Peripherals Limited has a market capitalization of ₹2.0b, and paid its CEO total annual compensation worth ₹5.1m over the year to March 2024. This was the same amount the CEO received in the prior year. Notably, the salary of ₹5.1m is the entirety of the CEO compensation.

On comparing similar-sized companies in the Indian Packaging industry with market capitalizations below ₹17b, we found that the median total CEO compensation was ₹3.8m. Hence, we can conclude that Raminder Chadha is remunerated higher than the industry median. What's more, Raminder Chadha holds ₹879m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | ₹5.1m | ₹5.1m | 100% |

| Other | - | - | - |

| Total Compensation | ₹5.1m | ₹5.1m | 100% |

On an industry level, roughly 82% of total compensation represents salary and 18% is other remuneration. At the company level, Worth Peripherals pays Raminder Chadha solely through a salary, preferring to go down a conventional route. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Worth Peripherals Limited's Growth Numbers

Worth Peripherals Limited has seen its earnings per share (EPS) increase by 2.2% a year over the past three years. It saw its revenue drop 10% over the last year.

We would argue that the lack of revenue growth in the last year is less than ideal, but it is good to see a modest EPS growth at least. It's hard to reach a conclusion about business performance right now. This may be one to watch. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Worth Peripherals Limited Been A Good Investment?

Worth Peripherals Limited has generated a total shareholder return of 31% over three years, so most shareholders would be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

To Conclude...

Worth Peripherals pays CEO compensation exclusively through a salary, with non-salary compensation completely ignored. The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation can have a massive impact on performance, but it's just one element. We've identified 2 warning signs for Worth Peripherals that investors should be aware of in a dynamic business environment.

Switching gears from Worth Peripherals, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Worth Peripherals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:WORTHPERI

Worth Peripherals

Manufactures and sells corrugated boxes and sheets in India.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

60 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

60 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative