Advertisement

- India

- /

- Basic Materials

- /

- NSEI:ULTRACEMCO

Is UltraTech Cement Limited's (NSE:ULTRACEMCO) Recent Stock Performance Tethered To Its Strong Fundamentals?

Most readers would already be aware that UltraTech Cement's (NSE:ULTRACEMCO) stock increased significantly by 13% over the past three months. Given that the market rewards strong financials in the long-term, we wonder if that is the case in this instance. Particularly, we will be paying attention to UltraTech Cement's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for UltraTech Cement is:

9.2% = ₹68b ÷ ₹739b (Based on the trailing twelve months to June 2025).

The 'return' is the amount earned after tax over the last twelve months. Another way to think of that is that for every ₹1 worth of equity, the company was able to earn ₹0.09 in profit.

View our latest analysis for UltraTech Cement

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

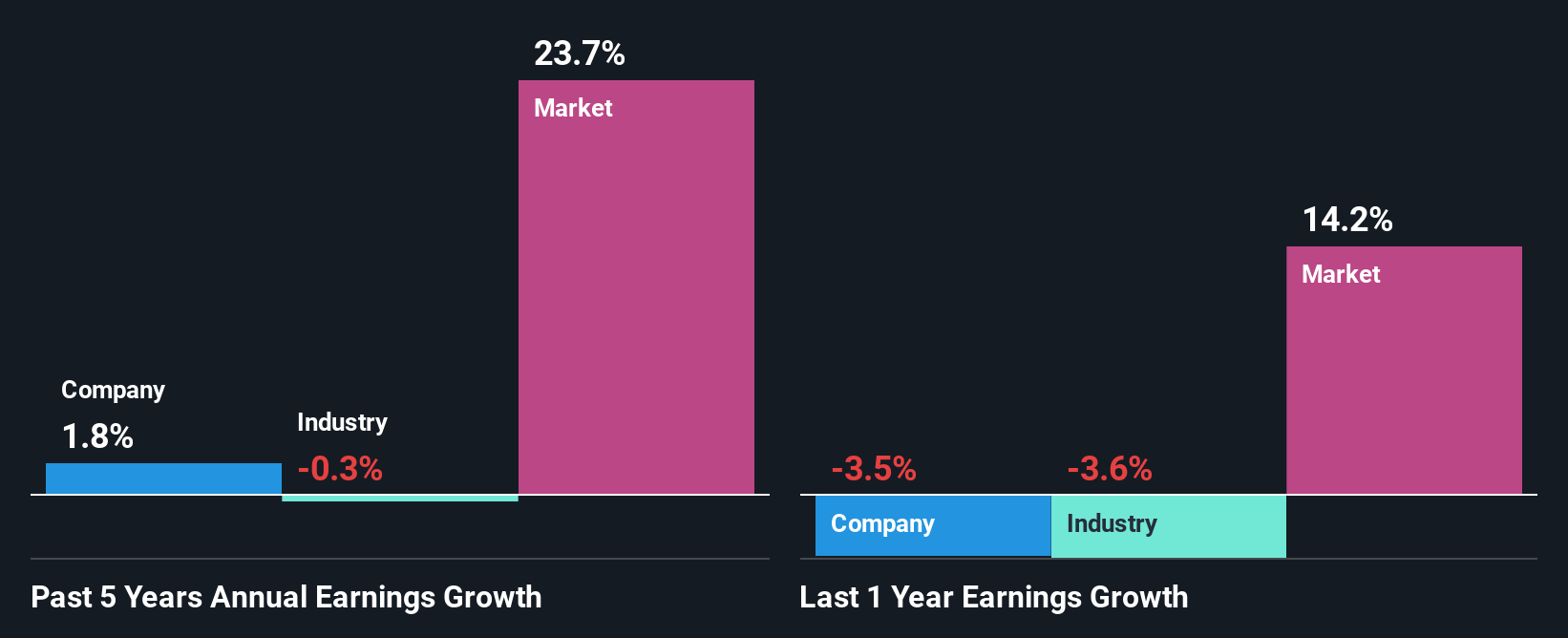

A Side By Side comparison of UltraTech Cement's Earnings Growth And 9.2% ROE

At first glance, UltraTech Cement's ROE doesn't look very promising. However, the fact that the company's ROE is higher than the average industry ROE of 5.4%, is definitely interesting. Still, UltraTech Cement has seen a flat net income growth over the past five years. Bear in mind, the company does have a slightly low ROE. It is just that the industry ROE is lower. Hence, this goes some way in explaining the flat earnings growth.

We then compared UltraTech Cement's net income growth with the industry and found that the industry which has shrunk at a rate of 0.3% in the same period, which makes the company's growth somewhat better.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about UltraTech Cement's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is UltraTech Cement Making Efficient Use Of Its Profits?

Despite having a normal three-year median payout ratio of 29% (implying that the company keeps 71% of its income) over the last three years, UltraTech Cement has seen a negligible amount of growth in earnings as we saw above. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

Additionally, UltraTech Cement has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 24% of its profits over the next three years. Regardless, the future ROE for UltraTech Cement is predicted to rise to 14% despite there being not much change expected in its payout ratio.

Summary

On the whole, we feel that UltraTech Cement's performance has been quite good. In particular, it's great to see that the company has seen significant growth in its earnings backed by a respectable ROE and a high reinvestment rate. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ULTRACEMCO

UltraTech Cement

Engages in the manufacture and sale of clinker, cement, ready mix concrete, and related products in India, the United Arab Emirates, Bahrain, and Sri Lanka.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor